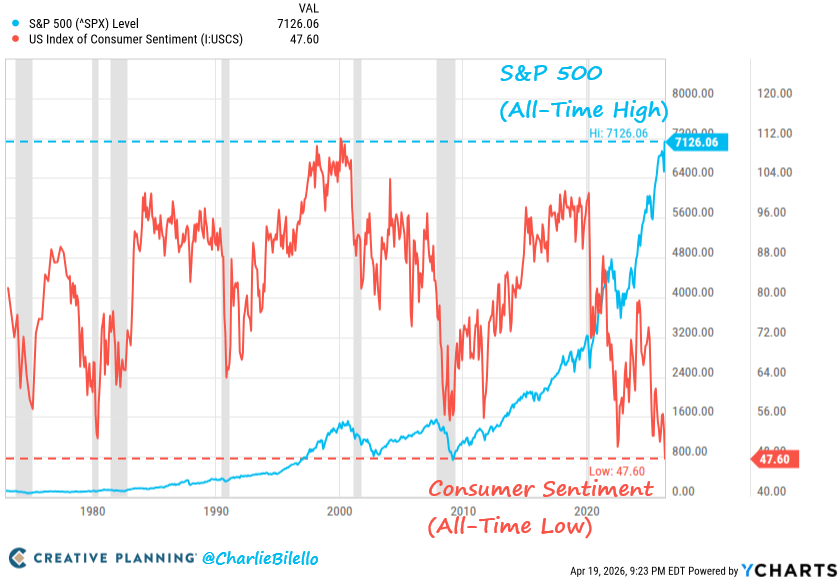

On April 17, the S&P 500 index closed at 7,126, also a new record, while the University of Michigan Consumer Sentiment Index for April fell to 47.6, the lowest reading in the history of the survey.

The split screen is surreal.

Charlie Bilello shared the graph below to highlight the gap.

Wall Street trades at high altitude. Household signals something darker.

Bitcoin sits in the middle of that gap, caught between the myth of hard assets and the reality of movement in a market regime still dominated by equity risk, ETF flows, and macro positioning.

That tension gives shape to the current setup. This dot-com comparison also focuses on the structure of late-cycle rallies, so it can bring a fresh reader.

A recent look inside the S&P 500 shows that a significant portion of the earnings revision support has come from a limited number of companies, with Micron alone accounting for 51% of positive earnings revisions since the start of the Iran war.

This is alongside intensive data showing that the top 10 stocks represent 35.5% of SPY and Mag 7 represents 30.4%.

In such a structure, the index is likely to continue rising. And in the moments when we seem our strongest, we can also become more vulnerable.

In the case of Bitcoin, the core question is straightforward.

If stock price appreciation turns out to be thinner than the composite index suggests, will BTC absorb the shock like an extension of high-beta risk appetite, or will BTC hold out amid widespread distrust in the broader system?

Recent market trends lean toward the first answer.

In March, Bloomberg reported that the 30-day correlation between Bitcoin and the S&P 500 rose to 0.74, the highest level this year.

That doesn’t resolve the long-running identity debate surrounding Bitcoin. That would narrow the short-term map.

At this stage, BTC is moving in sync with stocks, and many holders are looking to trade Bitcoin as an alternative.

Wall Street is celebrating, but households are retreating.

The clearest way to understand the current moment is to start with the household side of the economy. Because that’s where the emotional reality becomes most vivid.

Michigan’s poll is down 10.7% from March, with the current score at 50.1 and the expected score at 46.1.

Research director Joan Hsu said the decline widened the decline that began with the outbreak of the Iran conflict, with respondents pointing to higher prices, falling asset values and worsening conditions for purchasing durable goods and cars.

One-year inflation expectations rose to 4.8% from 3.8%, the largest monthly increase since April 2025.

This is what a squeezed consumer looks like.

Uncertainties about gasoline, groceries, financing costs and household balance sheets all figure into this number.

Energy is part of the bridge between Main Street and the market.

U.S. crude oil has risen to $87 and Brent to $95 as tensions flare up in the Strait of Hormuz, bringing the national average gasoline price to about $4.05 per gallon.

The survey itself points to the Iranian conflict as a factor in worsening sentiment.

Consumers don’t need to model revenue corrections or passive inflows to feel this.

They experience it at the pump, in their shopping carts, and in how they think about buying a new car or getting new credit.

At the same time, stock markets are behaving as if they can handle these pressures.

The S&P 500 continues to set new all-time highs, and the Nasdaq just posted its strongest rally on record.

There is a rational basis for many of the moves.

Earnings in key regions of the market were performing better than feared, and hopes of calm in the Middle East gave investors reason to take risks again.

Still, the gap has widened to the point that it cannot be ignored.

Family psychology shows tension. Asset prices continue to show resilience.

This gap creates a natural tension around Bitcoin.

Cryptocurrency holders need no more abstract discussion about whether consumer sentiment can predict a recession.

The practical question is, what happens to BTC if the market decides that households are sending a truer signal?

Bitcoin is trading at around $75,500 on igcurrencynews, down 0.40% in 24 hours, up 6.3% in 7 days, and up 6.5% in 30 days.

While the coin has stabilized and ETF demand is helping, the price structure remains 41.3% below its October 2025 all-time high of $126,198.

This leaves room for two very different interpretations.

Some see it consolidating before another leg moves higher. The other sees the market as still bound by the same macro forces that drive and threaten stock prices.

The dot com analogy is useful, focus becomes a sharper lens.

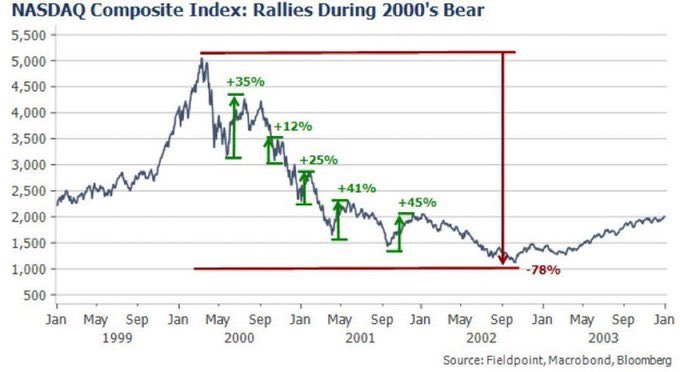

The 2000 Nasdaq chart has a mechanism that resurfaces every time the market expands.

It resurfaces for some reason.

Bear markets often feature violent countertrend upswings that feel convincing in real time.

The 2000-2002 sequence included rebounds of 35%, 12%, 25%, 41%, and 45% before ending with a full drawdown of 78%. Thierry Borger shared the graph below.

This pattern reminds investors that strong upward bursts can occur within a period of broader repricing.

It also reminds us that routes and destinations can be oriented in different directions for a long time.

Today’s setup still has a different structure.

The market in the late 1990s was full of companies built on weak business models, speculative capital, and the promise of distant returns.

Today’s leaders are bigger, wealthier, and can generate far more cash.

That changes the comparison. It also creates other risks.

As leadership narrows and the index’s performance becomes dependent on an increasingly smaller set of engines, the benchmark can grow stronger even as the participants beneath it fade.

That’s why the recent internal circumstances of the market need to receive more attention than the label “pure bubble.”

Micron accounted for 51% of the S&P 500’s revised earnings per share since the start of the Iran war, with Exxon Mobil, Chevron and ConocoPhillips together contributing another 29% and Broadcom 10%, according to Goldman Sachs data.

The median S&P 500 companies saw no change in earnings expectations.

As a result, rallies will rely on a narrow support base.

That doesn’t guarantee a rupture, but it leaves the structure open to disappointment in a small number of names and sectors.

The concentration data points in the same direction.

The top 10 stocks in SPY (35.59%) and Mag 7 (30.44%) tell the same story in plain English.

Much of the market’s apparent health lies on small platforms.

Valuations also remain high.

YCharts’ periodically adjusted P/E data and other long-term valuation metrics reflect market confidence.

Narrower leadership means fewer weak spots to change the overall tone of the market.

If the positioning is crowded, the unwind can move faster than the build-up.

Bitcoin’s role in that setting has changed over the past year.

Spot ETFs have made BTC a more direct channel for institutional capital, bringing both sponsorship and sensitivity.

SoSoValue’s Bitcoin ETF dashboard shows the sector is once again attracting meaningful capital, with net inflows of $664 million on April 17 after recovering in March after months of outflows.

These flows can soothe weak sessions.

You can also communicate your broader risk appetite directly to cryptocurrencies.

Bitcoin is gaining a larger buyer base through ETFs and is also inheriting more of Wall Street’s mood swings through the same door.

Bitcoin is nearing an identity test

That leaves Bitcoin in something of an unresolved situation, which is the central tension currently circulating in the market.

It is caught between two roles.

One role is that of liquidity risk assets, which tend to flow out when stock prices rise, especially when the ETF’s inflows are healthy and macro stress has eased.

The other role is for harder assets that can attract capital when confidence in the broader financial order weakens.

In previous cycles, these stories often alternated. This time it’s a match in the same frame.

Short-term markets still support the risk asset interpretation.

Bitcoin’s high correlation with the S&P 500 indicates that the market has been treating BTC as part of a similar broader risk appetite.

Current price data is crypto slate Although the Bitcoin page shows a recovery, the market has not yet regained its previous peak.

A benign macro environment, continued ETF buying, and broad participation in equities could allow this stabilization to continue.

Along that path, Bitcoin is likely to continue to rise further, with the same forces driving technology and large-cap growth.

A more significant path will open up if the disconnect between Wall Street and household finances is resolved not by improved consumer confidence but by falling asset prices.

This is where the Bitcoin identity test becomes concrete.

If the current correlation holds, any cracks in the stock due to narrow leadership, weakening institutional support, or new energy stresses would immediately put pressure on BTC.

This move does not require any cryptocurrency-specific triggers.

Stocks can do the job on their own, and Bitcoin can absorb secondary effects through sentiment, positioning, and ETF flows.

There is another route, and one that Bitcoin bulls still have in mind.

If household budget stress continues, inflation concerns persist, and confidence in traditional assets weakens without a full liquidation, Bitcoin could begin to trade as a parallel store of value rather than a leveraged technological proxy.

That path is even harder to determine from today’s evidence.

That will likely require steady ETF inflows and new demand for assets deemed outside direct sovereign control, as well as strength relative to the Nasdaq amid volatile stock prices.

Setup is possible. The market hasn’t confirmed it yet.

For now, live details will be displayed on the split screen itself.

Stock markets are thriving, but consumers are retreating, oil can still reprice inflation expectations overnight, and Bitcoin remains at a halfway point that may not be sustainable forever.

This is why comparisons with 2000 keep coming up.

It captures the emotional risk of a powerful rally on shaky foundations.

It also leaves room for more accurate conclusions.

For Bitcoin holders, the current market doesn’t have to be a repeat of the dot-com bubble, and they do have exposure issues.

Concentrated stock price increases and highly pessimistic consumers may coexist for some time.

They rarely coexist without consequences.

(Tag translation) Bitcoin