CoreWeave, an AI cloud infrastructure provider, has secured more than $20 billion in debt and equity financing this year. This includes a recently completed $3.1 billion financing backed by graphics processing units.

The oversubscription situation indicates the scale of institutional demand for companies and infrastructure related to building AI. Investors will be actively pouring money into the space throughout 2026, with CryptoRank data ranking AI as the most popular funding category this year.

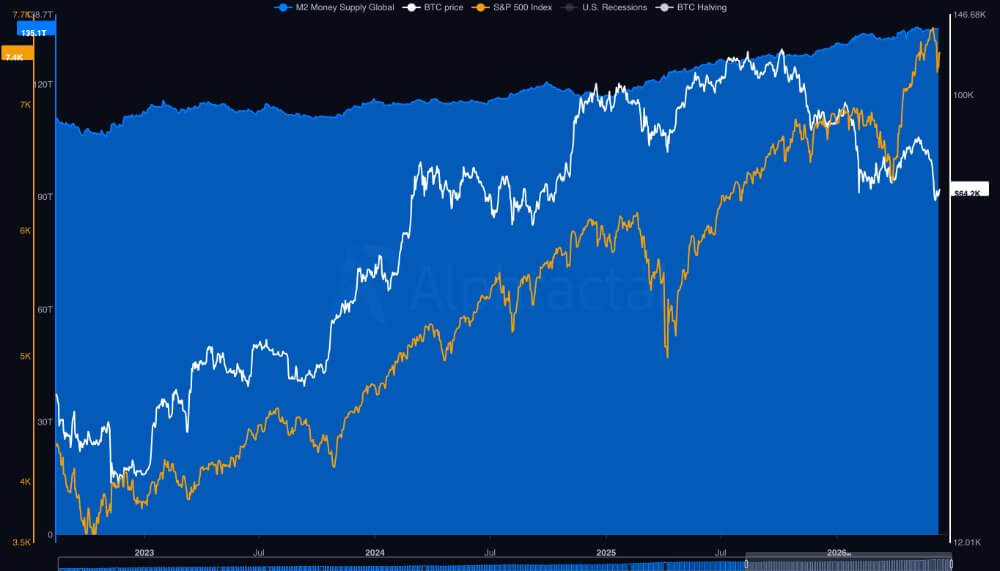

In stark contrast, Bitcoin moved in the opposite direction. Despite the global money supply expanding to record levels, the largest digital asset has fallen more than 50% from its previous peak around $126,000.

Historically, increased global liquidity has supported risk assets, with Bitcoin often benefiting as capital moves further along the risk curve. For most of the last cycle, this relationship seemed reliable enough that traders treated it almost as a rule.

But that relationship broke down this year as liquidity continued to expand. One possible explanation is that AI captured a larger share of the risk capital that might have otherwise supported Bitcoin’s recovery.

Why are investors funding AI infrastructure instead of Bitcoin?

Investors are directing tens of billions of dollars to artificial intelligence infrastructure instead of Bitcoin because the AI sector can provide predictable returns, income, and physical collateral that Bitcoin lacks.

While Bitcoin remains a volatile, non-yielding financial asset, AI infrastructure can offer multi-year dollar-denominated contracts backed by top technology companies.

For context, CoreWeave’s recent $3.1 billion delayed withdrawal term loan facility exemplifies the structural advantages that help AI compete with the crypto market for capital.

The financing provides investors with interest income, identifiable collateral, and a fixed maturity date, while the underlying customer agreement provides visibility into CoreWeave’s projected cash flows.

Moody’s and Fitch rated the facility Ba2 and BB+, respectively, giving institutional investors traditional credit tools tied to AI computing demand.

This structure allows institutional investors to assess GPU value, customer contract strength, projected cash flow, and refinance risk, while accessing secondary market instruments that provide yield.

Bitcoin, on the other hand, has no comparable revenue streams, interest payments, or claims on operating assets. Its earnings mainly depend on scarcity and future price increases.

Additionally, the scale of spending on AI has widened the opportunity for investors. The Bank for International Settlements (BIS) predicts that the five largest hyperscalers will spend more than $1 trillion in AI-related capital spending from 2025 to 2026.

Considering this, Pierre Rochard, CEO of Bitcoin Bond Company, stated that capital rotation is essentially a race to secure key supply bottlenecks. He said the AI boom will require unprecedented physical enhancements across power generation, specialized chips and cooling systems.

Investors are therefore funding tangible assets tied to companies’ immediate, large-scale demand for computing power. And unlike the “software eats the world” era, which spawned a proliferation of low-marginal-cost companies, the AI era will see excess savings absorbed directly into physical bottlenecks like expensive GPUs, data centers, and power grids.

“This is why the AI boom has crowded out Bitcoin,” Rochard argued, adding that capital is flooding into companies that manage these physical constraints. He said the market is paying up front for an industrial build-up that will significantly unlock global liquidity.

Ultimately, Roshard noted, this supercycle of AI capital spending is absorbing excess fiat liquidity that could otherwise flow into scarce bearer assets, making AI infrastructure a formidable competitor for institutional investors’ risk budgets.

How an AI funding reversal could benefit Bitcoin over time

But the more difficult question facing the market is what happens when the artificial intelligence investment cycle begins to bend. While the AI downturn could cause short-term market turmoil, the eventual capital turnover could benefit Bitcoin in the long term.

Rochard argues that the current concentration of capital in AI infrastructure will eventually create the conditions for liquidity to return to digital assets. he said:

“As the AI capital investment cycle turns from boom to overcapacity, capital currently trapped in crowded AI tickers and infrastructure financing will look for an exit.”

A reversal could begin if earnings estimates decline, depreciation costs exceed margins, power prices rise or debt-financed data centers face refinancing problems, he said.

In such an environment, investors may begin to decouple the long-term utility of AI from the aggressive price paid for exposure to AI, recognizing that productive technologies may still generate weak investment returns.

In particular, the BIS has already warned that $1 trillion in AI commitments is outpacing free cash flow, forcing companies to increasingly rely on debt.

The BIS warned that disappointing returns could set back AI financing and turn a capital investment boom into an investment slump, with wide-ranging implications for credit and financial markets.

For Bitcoin, such an AI exit could pose short-term risks while creating potential long-term structural benefits. If a downturn in AI hurts highly leveraged data center vehicles or private credit funds, the market’s initial reaction could be a significant retreat from risk. Investors could simultaneously sell stocks, credit, and cryptocurrencies to raise cash, causing Bitcoin to fall immediately following a credit freeze.

However, a long-term solution could favor Bitcoin. Once the initial deleveraging is complete, capital will aggressively seek assets with clear return drivers, such as government bonds, gold and defensive stocks.

Rochard argues that Bitcoin could attract some of that capital because:

“[It’s]the opposite kind of asset. There’s no board of directors committed to monetizing AI. There’s no capital expenditure budget. There’s no debt maturity wall. Just because Nvidia ships a better chip or a hyperscaler signs a power contract doesn’t accelerate its issuance schedule. This is not a claim on future corporate cash flow. This is a scarce financial asset that competes with savings technology.”

Ultimately, Bitcoin cannot be counted on to be an automatic catalyst for the AI collapse, but the eventual unwinding of infrastructure deals could create an opportunity for capital to rethink corporate bonds, depreciation, and scarce monetary assets without income risk.

(Tag translation) Bitcoin