The latest Canaan financial results also reveal new divisions among Bitcoin mining’s most prominent hardware suppliers. The company, which sells mining machines, reported a significantly weaker quarter just as its crypto holdings became impossible to ignore.

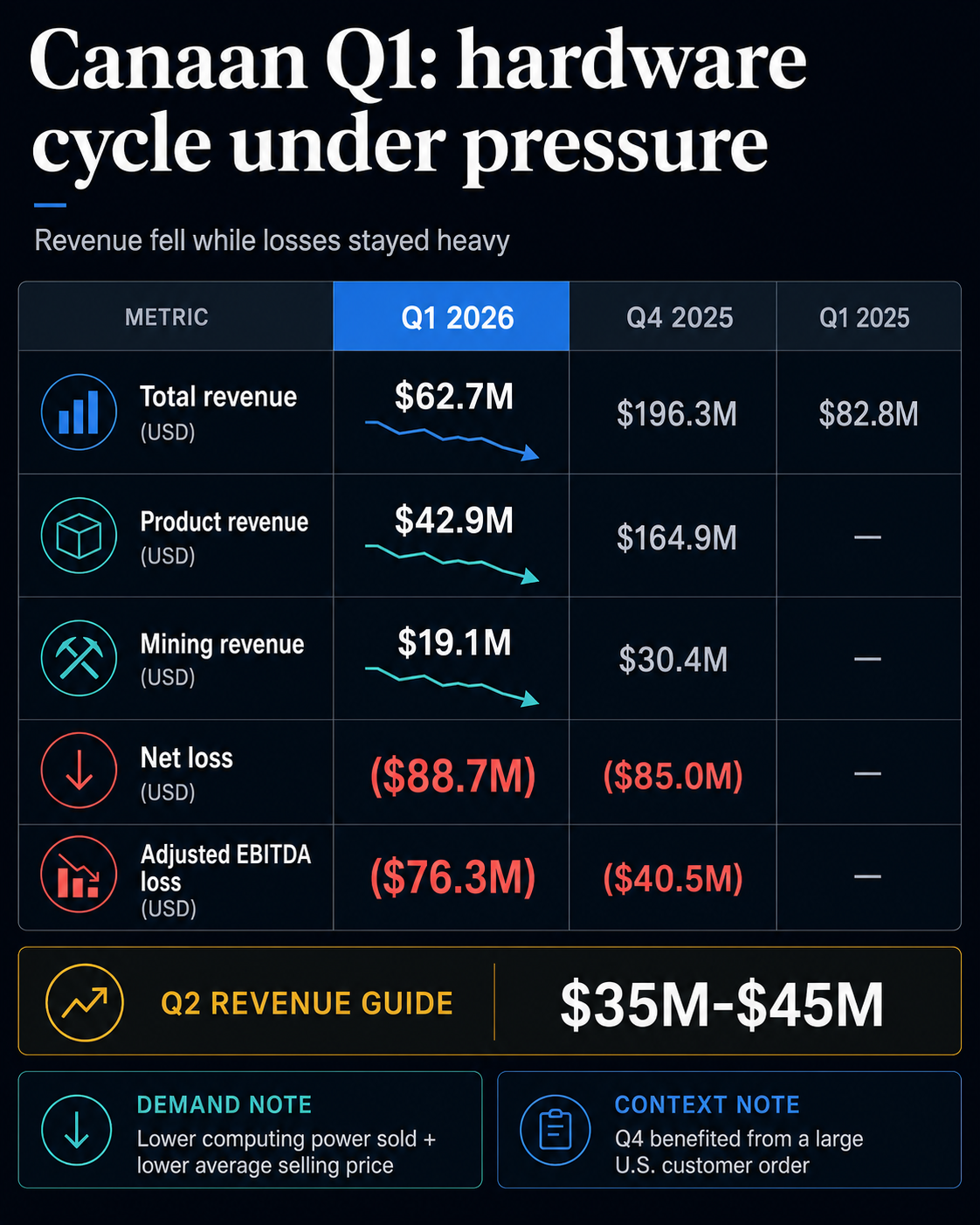

The ASIC maker announced revenue for the first quarter of 2026 fell to $62.7 million, down from $196.3 million in the previous quarter and $82.8 million in the year-ago period.

Net loss widened to $88.7 million from $85 million in the fourth quarter, and non-GAAP adjusted EBITDA loss nearly doubled from $40.5 million to $76.3 million.

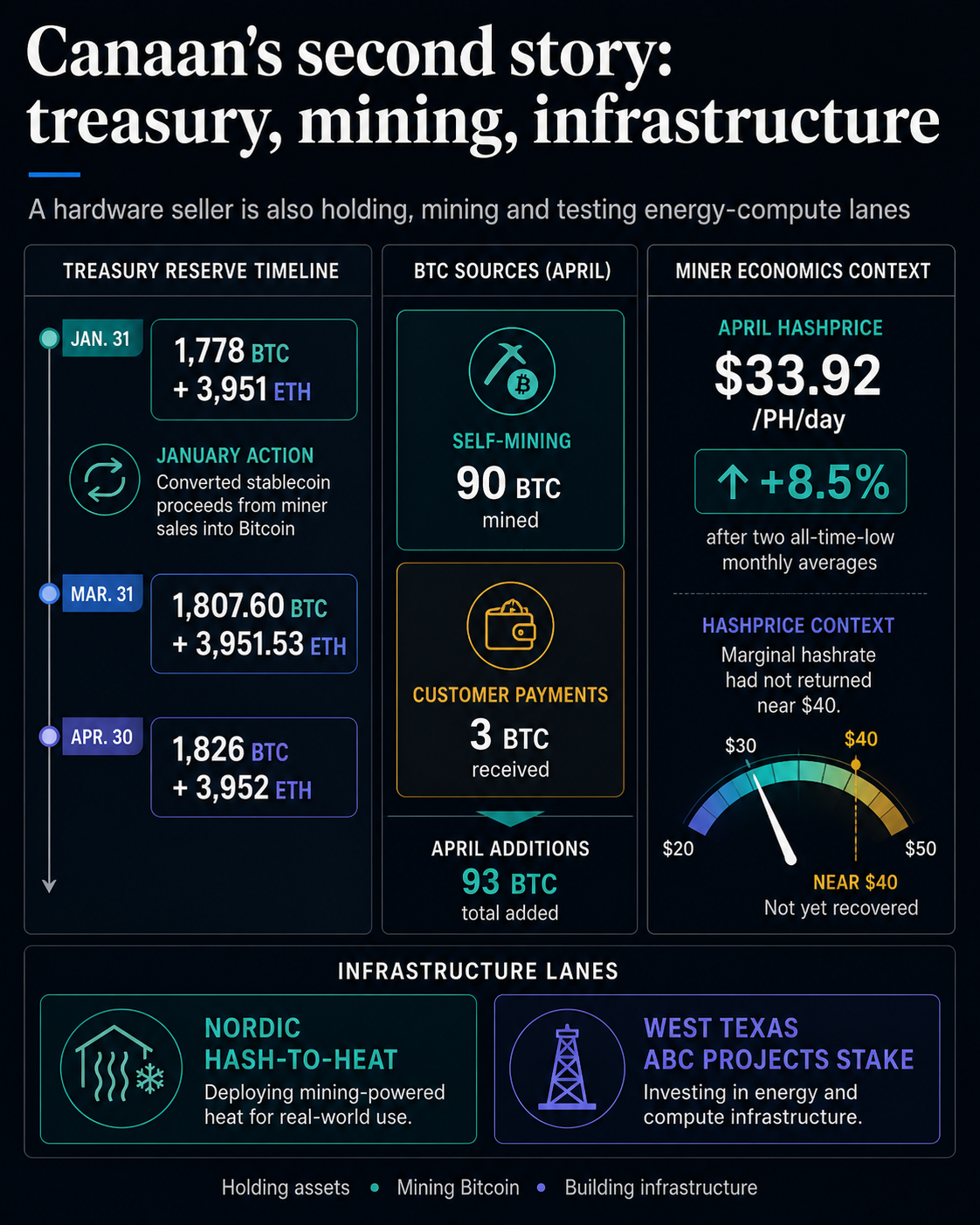

At the same time, Canaan ended March at 1,807.60. $BTC and 3,951.53 $ETHa record crypto asset for the company.

in crypto slate May 22nd price level is approximately $77,200 $BTC $2,100 per case $ETHwhose stack was valued at approximately $148 million on a spot market basis before accounting, receivables, or liquidity constraints.

That’s the tension within the quarter. Canaan still sells machines that power Bitcoin mining, but the reported numbers make it seem like the company is a growing company despite a weak hardware cycle. $BTCThe other – linked balance sheet. This decline also reflects sluggish demand for Bitcoin mining due to the tight miner economy.

The important point is the hardware cycle.

Canaan’s product segments demonstrate why hardware revenue, minor economics, and financial exposure should all be read together. ASIC miner revenue decreased to $42.9 million from $164.9 million in the fourth quarter of 2025.

The company said this decline reflects lower computing power sold and lower average selling prices, which is related to tighter market demand following the Bitcoin price drop.

This representation is important because ASIC manufacturers are located at the upper reaches of the minor economy. If miners are confident that they can recoup their costs on new machines, hardware orders can bring forward revenue.

Demand for new hardware can quickly weaken as profit margins are compressed by power costs, difficulties, financing, or hash price pressures.

There was also some company-specific noise in Canaan’s Q1 comparison. The fourth quarter benefited from large orders from U.S. customers, after which the decline was even steeper.

However, the demand language in the first quarter release still points to broader issues. The hardware line reflects both weaker unit demand and lower average prices.

Outside Canaan, the miners’ economic situation was still recovering from difficult conditions. According to the April 2026 lookback of the Hash Rate Index, the average hash price in USD rose 8.5% to $33.92 per PH per day after the monthly average hit new all-time lows twice.

Despite hash prices returning to near $40 in early May, marginal hashrate has not returned to the network, the company said.

CryptoSlate’s own mining coverage tracks the same pressures from a different angle. Earlier this year, miners’ failure to rush to bring machines back online even after prices recovered underscored that point. $BTC It’s not just about whether the rig is profitable or not.

Power prices, difficulty, machine efficiency, and balance sheet liquidity are all important.

For Canaan, it turns the product’s revenue line into a key signal. The company has two related exposures: Bitcoin price fluctuations and miners’ willingness to justify new capital investment in machines.

The first quarter suggested that demand was not yet strong enough to absorb the operating base of hardware sellers.

Treasury is a counterweight

The other side of the story is Canaan’s Bitcoin vault and $ETH Holdings continued to increase.

In its January mining update, the company announced that it had converted stablecoin revenue from miner sales into Bitcoin, reaching 1,778 in reserves. $BTC and 3,951 $ETH At the end of the month.

Results for the first quarter ended March 31 were 1,807.60. $BTC and 3,951.53 $ETH. At the end of the quarter, Canaan announced that operating profit for April increased by $90. $BTC From self-mining and 3 $BTC From the customer’s payment, the balance is 1,826 $BTC and 3,952 $ETH By April 30th.

This mechanism changes the way you look at the quarter. Canaan’s crypto asset balances currently reflect ongoing operational decisions in parallel with its traditional holdings.

A portion of miner sales proceeds are transferred to Bitcoin, and self-mining continues to add $BTC Although mining revenue decreased from the fourth quarter,

The distinction is important. Pure ASIC suppliers depend on customer demand for their machines. Miners depend on operational efficiency, power costs, hash prices, and Bitcoin production.

Treasury holders are dependent on the market value of the assets they hold. Kanan now has all three elements, making it difficult to interpret reported weaknesses through a single lens.

Operating losses remain a counterpoint. The company reported a net loss of $88.7 million in the first quarter, and sales in the second quarter were only $35 million to $45 million, lower than the already weak first quarter results.

This guidance means the balance sheet could be a big part of the story, since the income statement has yet to show any signs of recovery.

Canaan’s spot estimate is approximately $148 million. $BTC and $ETH Restraint is also necessary. This helps with scale, but the market value is different from Canaan’s accounting value, and investor motivations are still unproven.

Without evidence of market capitalization and stock prices, a more accurate argument is that Treasury is now of enough substance to belong near the top of the story.

Infrastructure gives Canaan a third lane.

Canaan’s Q1 release also promoted a broader infrastructure message. The company highlighted its hash-to-heat expansion in Northern Europe and its investment in the West Texas ABC project, which is located closer to energy and computing infrastructure than traditional machinery sales.

These details lie behind the core numbers, but they help explain why Canaan is looking beyond the next ASIC order cycle.

As mining margins tighten, public miners are already gravitating toward energy, hosting, AI or high-performance computing strategies. CryptoSlate has covered how public miners are leveraging Treasury and infrastructure pivots to navigate the post-halving market.

Canaan versions are different because they are upstream. The company sells to miners, operates its own mining exposure, owns a growing crypto stack, and tests energy-related infrastructure projects.

The combination could help the company if hardware demand remains weak, but it also makes the investment story more complicated. Buyers of Canaan stock are reading on ASIC sales, Bitcoin price exposure, self-mining production, and management’s ability to turn infrastructure projects into lasting returns.

This complexity is what keeps this quarter from being a story of basic deviations and expectations. Canaan’s customers are under stress, product revenue has significantly decreased, and at the same time its own crypto balances have become more noticeable.

Sellers of mining machines are now exposed to the assets that their machines are built to produce.

The next test is easy. The question is whether Q2 earnings and product prices stabilize enough that Q1 looks like a weak transition quarter, or whether Canaan-induced decline pushes the story further into treasury, self-mining, and infrastructure exposures.

Even if customer demand improves, Canaan will continue to grow primarily as a circular ASIC supplier. $BTC and $ETH balance. If revenues decline in line with guidance and the crypto stack continues to rise, the market will have more reason to treat the company as a hybrid of hardware seller, miner, Bitcoin treasury, and energy calculation operator.

So far, the source records bear out tensions rather than clean verdicts. The first quarter showed a slowdown in the hardware business, widening losses, a decline in mining revenue, and an increase in crypto assets.

This combination makes Canaan one of the clearest examples of how Bitcoin mining transactions are changing. Even companies that sell picks and shovels are increasingly taking on asset risks that their customers face every day.

The company is still heavily exposed to demand for Bitcoin mining hardware despite its increased financial exposure. The broader question after these Canaan gains is whether Treasury growth can offset weak hardware demand.