BlackRock has updated its regulatory filing for its new Bitcoin Premium Income ETF, signaling an impending launch that will intensify Wall Street’s competition for Goldman Sachs Group Inc. to win over yield-seeking digital asset investors.

On June 10, the world’s largest asset manager filed with the Securities and Exchange Commission (SEC) an updated prospectus for the iShares Bitcoin Premium Income ETF, which trades under the ticker BITA.

The proposed amendments introduce important operational and pricing parameters, including a sponsorship fee of 0.65% per annum, payable at least quarterly.

This fee positions BITA as a high-cost alternative to plain vanilla spot Bitcoin funds, such as BlackRock’s own iShares Bitcoin Trust (IBIT).

Still, this fee is well below the expense structure typical of large equity-based covered call ETFs currently operating in traditional financial markets.

Meanwhile, Bloomberg Intelligence ETF analyst Eric Balchunas said the filing likely marks a final structural adjustment before the fund receives regulatory approval to begin trading publicly.

Inside the workings of seed capital and trust

The updated registration statement provides an operational picture of the fund’s original financial position, filling in several key metrics that were omitted in the original January filing.

Documents state that initial seed investors acquired 198,000 shares on June 1 at $50 per share, generating $9.9 million in proceeds to establish the trust.

BlackRock put the money toward establishing the fund’s underlying portfolio on June 9, according to filings. The trust acquired exactly 109.9630217 Bitcoins along with 90,901 shares of IBIT.

At the same time, the fund manager wrote 856 option contracts to initiate the income-generating component of the strategy. Following these transactions, the trust reported a net asset value of approximately $9.99 million. This corresponds to an initial net asset value of $49.97 per share.

The prospectus states that in order to maintain day-to-day operations, the trust plans to periodically liquidate a portion of its IBIT holdings to meet the ongoing 0.65% sponsor fee.

This mechanical design reflects the mixed composition of the fund, which concurrently holds physical Bitcoin, liquid spot ETF stocks, and cash instruments while writing option contracts primarily against the IBIT stock allocation.

Covered call strategy and volatility dynamics

This investment mandate positions BITA as a covered call Bitcoin ETF designed to track Bitcoin’s baseline performance while generating premium distributions.

Management intends to accomplish this by selling call options on IBIT stock and possibly a specialized index that monitors a wide range of physical Bitcoin exchange-traded products.

By selling these options, the Fund collects an upfront premium from counterparties seeking leveraged exposure to potential upward movements in IBIT’s stock price. In exchange for this immediate source of income, the Fund waives the right to appreciation above a predetermined strike price.

BlackRock’s strategy includes maintaining a target override level between 25% and 35% of the trust’s total net assets.

This partial override strategy ensures that a large portion of the portfolio remains unhedged, allowing shareholders to participate in a portion of the Bitcoin market bull run while utilizing a smaller segment of the asset base to maintain distribution yield.

For asset allocators, this structure reflects equity-linked income instruments that have gained significant market share during periods of ranged or moderately positive equity performance.

Cryptocurrencies are a unique underlying asset for this strategy due to their structurally higher implied volatility compared to traditional asset classes such as equities and sovereign debt. High volatility drives up the market price of option contracts, theoretically allowing BITA to command a larger premium than comparable stock index funds.

However, this income generation model comes with inherent trade-offs. In a sharp bull market for cryptocurrencies, written call options limit the fund’s total return and cause BITA to underperform its underlying spot assets.

Conversely, this strategy provides modest downside protection in flat or moderately declining market conditions, as the premiums collected offset small capital losses.

Goldman Sachs intensifies competition

The timing of BlackRock’s amendments intensifies its conflict with Goldman Sachs, which has been pushing for its own regulatory framework for competing automakers.

The Goldman Sachs Bitcoin Premium Income ETF has completed its regulatory review process and is expected to become effective near the beginning of July.

Although both Wall Street institutions target the same customer base, there are clear differences in their operating frameworks.

Goldman Sachs products do not directly hold physical cryptocurrencies. Instead, the investment strategy provides that at least 80% of net assets will be directed to vehicles that provide Bitcoin exposure, such as external spot Bitcoin ETPs, exchange-traded options contracts, and wholly-owned subsidiaries based in the Cayman Islands.

Additionally, Goldman Sachs plans to implement a more aggressive option override framework. Under standard market conditions, option override levels are expected to range from 40% to 100% of total Bitcoin exposure, according to the company’s regulatory filings.

| Features | iShares Bitcoin Premium Income ETF (BITA) | Goldman Sachs Bitcoin Premium Income ETF |

|---|---|---|

| Direct BTC holdings | Yes (blended with IBIT) | No (using ETP and Cayman subsidiary) |

| Overwrite target range | 25% to 35% of NAV | 40% to 100% of exposure |

| Sponsorship and operating expenses | 0.65% per annum | Final decision scheduled |

| Key option targets | IBIT Stock and Spot Bitcoin Index | Extensive Bitcoin ETP and options market |

Once both funds become active, this operational difference could influence market preferences. Goldman’s wide override parameters allow for higher theoretical distribution yields during market downturns, but expose investors to larger caps during sudden rises in the Bitcoin market.

BlackRock’s conservative 25% to 35% range, on the other hand, preserves greater capital appreciation potential at the expense of a lower baseline distribution target.

Maturation of the Bitcoin ecosystem

The move to actively managed, high-yield crypto products marks the second major evolution of the digital asset ETF ecosystem.

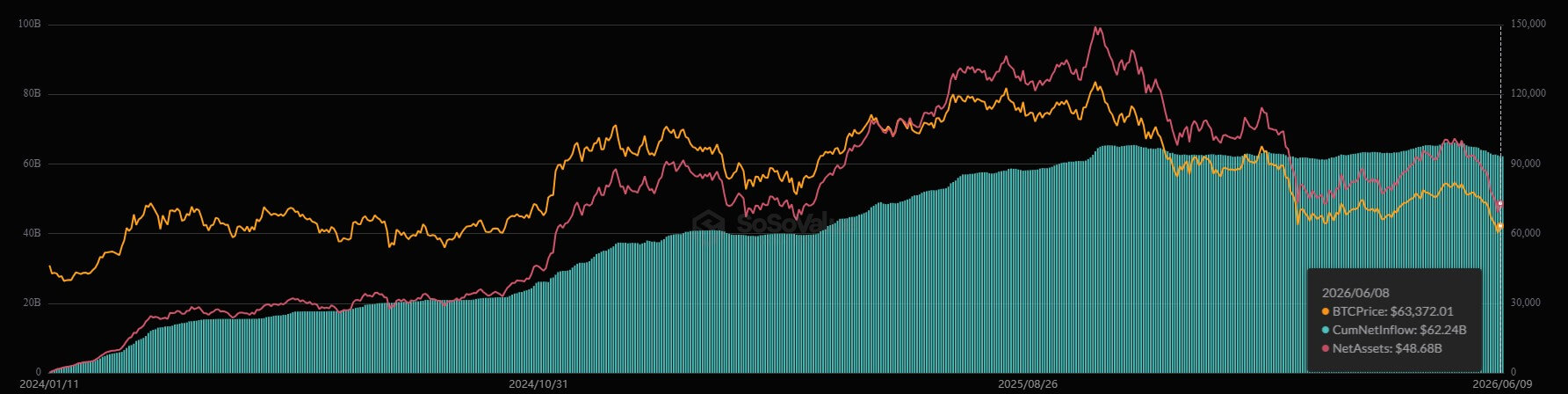

The first phase focused entirely on establishing direct infrastructure, represented by BlackRock’s flagship spot business, IBIT, which has generated total net inflows of $62 billion since its launch in 2024, according to data compiled by SoSoValue.

The introduction of rival products from BITA and Goldman shows that Bitcoin ETF returns are becoming a distinct product category beyond basic spot exposure.

Wall Street asset managers are now focusing on differentiating their products to attract risk-averse institutional portfolios and asset advisory networks that prioritize recurring cash flow over pure speculation.

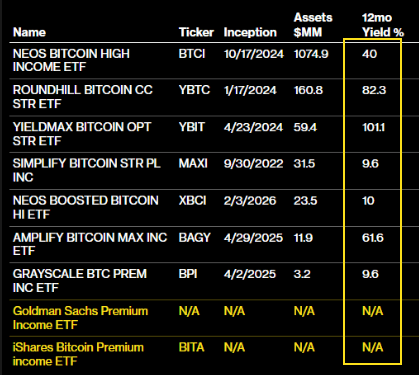

This emerging segment is not without existing competition. Future institutional products will enter a market where specialist issuers have already established an early foothold. For example, the NEOS Bitcoin High Income ETF (BTCI) has amassed over $1 billion in assets under management by utilizing a comparable options-driven yield framework.

Meanwhile, the long-term viability of these premium incomes depends on educating investors on the distinction between structured yields and traditional bonds.

The payments that BITA and its peers generate derive entirely from option pricing dynamics and market volatility, rather than interest payments or underlying corporate cash flows.

As a result, the distribution rate will fluctuate based on macroeconomic changes, trading volumes, and changes in the option’s volatility index.

(Tag Translation) Bitcoin