Bitcoin is about to experience its biggest option expiration of the year at the worst possible time.

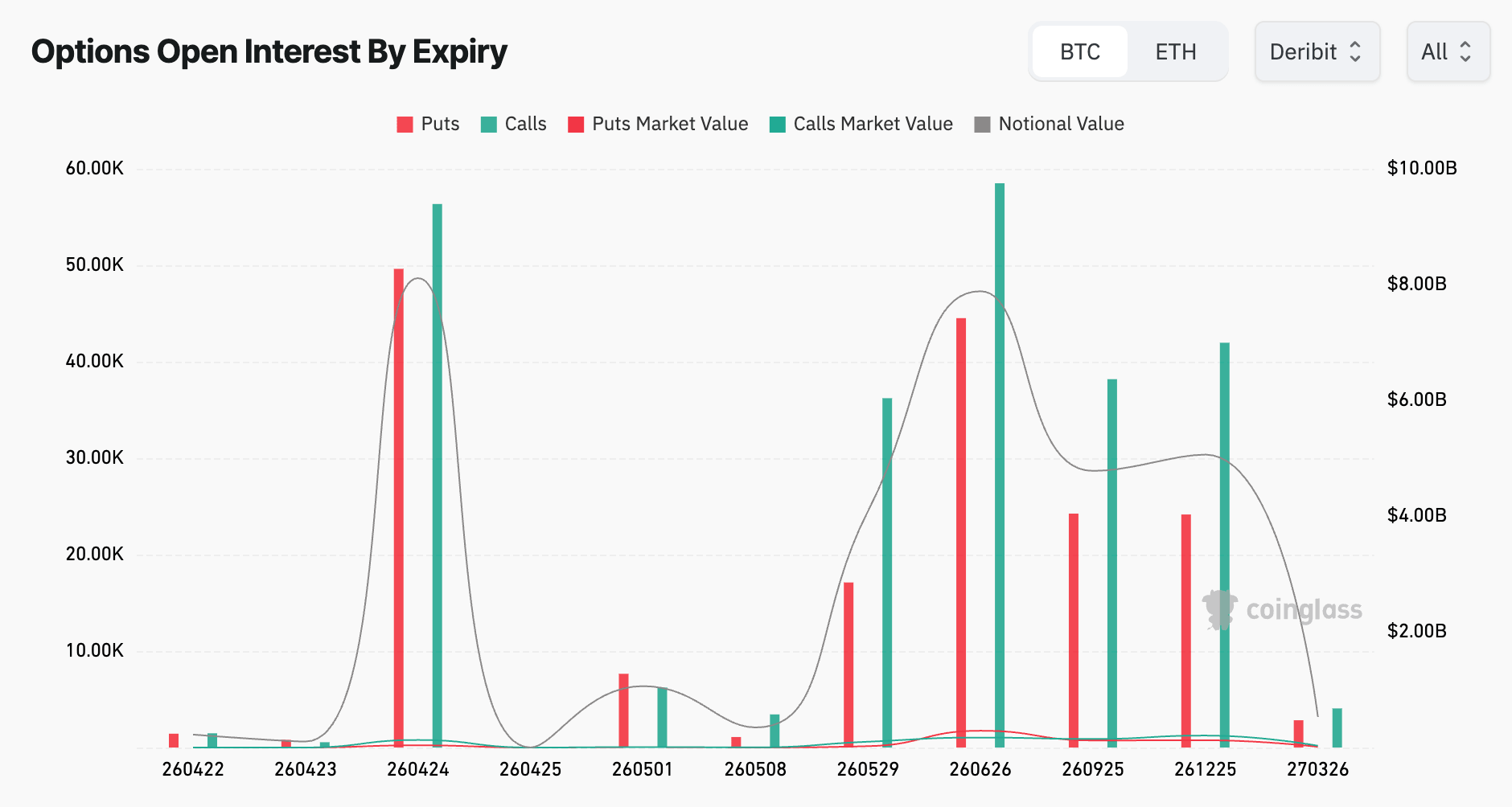

The nominal open interest in Deribit options expiring on April 24 is approximately $8.07 billion, split into 56,300 calls and 49,540 puts, according to CoinGlass data. While the ratio itself is bullish, it comes against the backdrop of one of the most uncertain macro environments in recent months.

The expiration comes three days before the Federal Reserve convenes for its April 28-29 meeting and four days before the Bureau of Economic Analysis releases first-quarter GDP and March PCE inflation data on April 30.

This is the densest macro calendar in a while, opening in an environment where Fed officials have spent the past week warning on record that oil-driven inflation could keep borrowing costs rising for much longer than markets assumed.

There is considerable tension in the structure of derivatives itself.

Currently, Deribit has approximately $31 billion in total options open interest, which exceeds even BlackRock’s IBIT, and the April 24 contract has a large amount of call positioning, with approximately $395 million concentrated at a strike price of $75,000. The biggest pain in this contract is around $71,500 to $72,000, roughly $3,000 to $4,000 below the current Bitcoin price.

In options markets, maximum pain is the price level at which the most contracts expire worthless, benefiting sellers (in this case large institutions and market makers) more than buyers. This gap can create a downward gravitational force as subsidence approaches.

The Fed has a new problem, and it’s coming from the Strait

In the war that began in late February, a coordinated U.S.-Israel attack on Iran caused the closure of the Strait of Hormuz, a narrow waterway through which about 20% of the world’s oil supplies flow, and pushed Brent crude oil prices above $100 a barrel for the first time in years.

Iran’s April 17 economic reopening announcement temporarily reversed some of that pressure, with Brent dropping about $10 per barrel to nearly $89 and Bitcoin surging toward the $77,000 to $78,000 range.

But it turns out that relief didn’t last long. Bitcoin opened around 2.5% lower on Monday as the US seized a Strait-bound Iranian cargo ship on Sunday, seemingly confirming diplomatic progress from last weekend. Shipping traffic on the corridor remains more than 95% below pre-war levels, and because insurance companies do not cover the corridor, major shipping companies still sail ships to various parts of Africa, while warships remain active.

All of this makes everything the Fed does or says in the coming weeks extremely consequential, especially for Bitcoin.

St. Louis Fed President Alberto Moussallem said last week that the oil shock would likely keep underlying inflation at around 3% for the rest of the year, almost a full percentage point above the Fed’s 2% target.

This is said to support the rationale for keeping interest rates in the current 3.50% to 3.75% range “for some time.”

New York Fed President John Williams essentially reiterated this, saying that rising energy prices are already spilling over into airfares, groceries, fertilizer and other consumer products, and that the process has “already begun.” The CME FedWatch tool was pricing in a 99.5% chance of a hold on the stock heading into the weekend.

The best summary of what’s at stake came in Fed Director Christopher Waller’s April 17 speech, which was almost certainly the Fed’s last substantive communication before a pre-meeting blackout cut off new guidance.

Waller described the situation as a watershed, saying that an early resolution to the dispute would keep inflation moving toward 2%, leaving room for interest rate cuts later this year. On the other hand, a prolonged conflict would likely lead to more supply chain disruptions and higher inflation across a wide range of goods and services. The ceasefire is so fragile that both paths really persist.

Why does Bitcoin option expiration matter?

Large option expirations rarely move prices cleanly in one direction, and the macro sensitivities that have defined crypto markets since late February have made most crypto-native positioning signals less reliable than usual.

The more specific risks from Friday’s settlement are structural. The large expirations concentrated near the top of the recent range may create hedging dynamics among dealers, amplifying the initial arrival of macro signals.

If the Holmes situation stabilizes and a rate cut becomes more likely, the call-heavy position could put pressure on $75,000. When a new escalation arrives, the same structure runs in reverse, with maximum pain nearing $72,000 for level dealers to try to defend.

Financial institutions spent much of this quarter selling upside exposure to Bitcoin to generate yield, transferring risk to market makers. This creates a structural cushion that disappears as soon as the contract expires, leaving Bitcoin even more exposed to macro and geopolitical forces.

Waller’s April 17 speech was the last given by Fed policymakers before officials entered a pre-meeting blackout ahead of the April 28-29 meeting.

The FOMC’s decision will be announced without any guidance since mid-April, and markets will read it in conjunction with first-quarter GDP and PCE data, which will provide the first understanding of how much the Hormuz shutdown will actually cost the US economy.

Bitcoin’s performance over the next 10 days will be subject to Friday’s expiration, the Fed’s decision, and a series of numbers that could change the price of the entire interest rate outlook. The derivatives market already has a position in the first event. Now we need to see if it’s also true for the other two.

(Tag translation) Bitcoin