CME Group’s crypto futures and options have been trading continuously since 4pm CT on May 29th, marking the first full-year trading week without the typical weekend CME gap.

More than 7,200 contracts were traded in the first 48 hours, representing approximately $50 million in notional value, enough to confirm that institutional demand for weekend hedges is genuine.

However, the announcement coincided with the S&P 500, Dow, and Nasdaq all closing at record highs on June 1, while Brent crude oil rose 4.2% to settle at $94.98 following a flare-up in U.S.-Iranian tensions, and Bitcoin nearly lost its $70,000 floor.

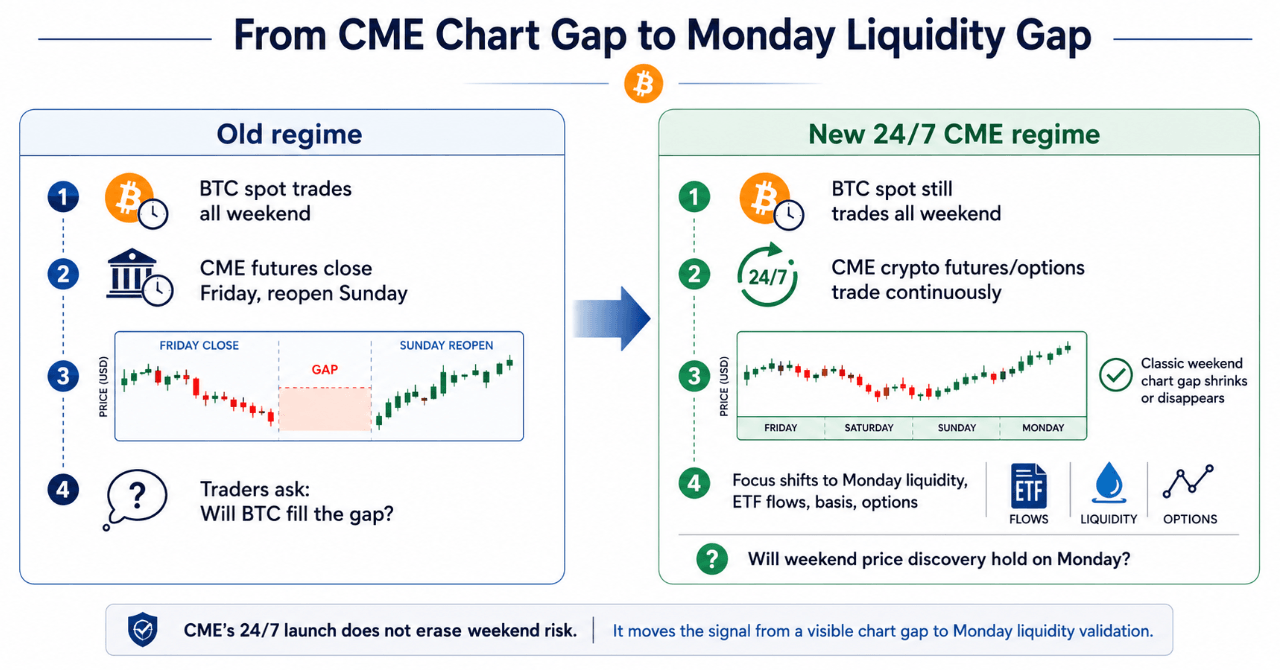

From chart gap to liquidity gap

Prior to May 29, the Bitcoin spot market traded continuously, but CME futures closed every Friday afternoon and resumed trading on Sunday evening.

As spot moved sharply over the weekend, the CME futures chart reopened with a visible gap between Friday’s closing price and Sunday’s opening price. Traders treated these gaps as magnets, as prices often tend to revert within a few weeks and close the gap.

Continued trading in CME closes a gap in the chart and opens another gap. The US ETF market follows stock market time, with some financial institutions’ desks lightened over the weekend and Monday morning still meaning a return to full participation in the cash market. The new question is whether weekend price discovery will hold when Monday’s liquidity arrives.

CME’s crypto derivatives have averaged 407,200 contracts per day since the start of 2026, an increase of 46% year-over-year, on the back of a $3 trillion notional trading volume across all crypto products in 2025.

This volume base confirms that financial institutions are already using CME as a hedging instrument, and the 24/7 extension removes periods where hedges were unavailable without fundamentally changing where prices are formed.

Bitcoin as a weakness

The sharper take this week is that Bitcoin is below its record share price increase, and the narrowness of its share price gains makes underperformance difficult to ignore.

The index record was led by Nvidia’s 6.2% session gain, while a small majority of stocks fell, with the Russell 2000 down 0.5 percentage points due to rotation into large-cap tech stocks.

Bitcoin has historically tracked a wide range of risk sentiments, putting it on the wrong side of being bullish on the surface but defensive on the surface.

According to data from Pharcyde Investors, the U.S. Spot Bitcoin ETF lost about $3 billion in 10 trading sessions from May 15 to May 29, including $733.4 million on May 27 alone and $527.8 million from BlackRock’s IBIT in the same session.

ETF flows are now Bitcoin’s most direct institutional demand signal, and that signal runs counter to the market structure improvements that CME has just delivered, as continued regulated futures access amplifies price discovery as institutional allocators add exposure.

| market signals | recent movements | BTC read through |

|---|---|---|

| S&P500 / Dow / Nasdaq | record close | headline risk on tape |

| Nvidia | +6.2% | Rally focused on megacap technology |

| russell 2000 | -0.5% | Weak width/weak bottom defense |

| Slight majority of US stocks | fell | The strength of the index is not wide-ranging. |

| brent crude oil | $94.98, +4.2% | Inflation/interest rate pressures remain strong |

| Bitcoin | lost almost $70,000 | Unable to keep up with stock price rises |

| Spot BTC ETF | Approximately $3 billion leaked in 10 sessions | Institutional demand signal is negative |

Monday’s liquidity validates the weekend

If Monday’s full return of ETFs and physical market participation brings Bitcoin back to stock performance, CME’s new structure will directly contribute.

Financial institutions that had hedged their weekend crypto exposures with regulated futures through Saturday and Sunday will arrive at Monday’s open with positions already adjusted, mitigating the chaotic pricing that previous Sunday night reopenings sometimes produced.

VanEck identified the $80,000 to $85,000 zone as the key resistance to a change in momentum, and the three traditional CME gaps in the $70,000 to $80,000 range remain unresolved targets prior to the new regime.

Bitcoin’s 30-day annualized perpetual basis was -0.45% as of mid-May, down from 3.16% a year earlier, resulting in a spot-led structure with minimal leverage overlay.

A recovery from this configuration tends to be a durable spot-driven move, with the bullish case hinged on a reversal in ETF trends and broader equity risk appetite beyond mega-cap tech, giving Bitcoin a tracking tape.

Macro becomes a magnet

When there are no more gaps in the chart to fill, oil-driven inflation concerns become a cleaner short-term magnet.

Brent at $94.98 maintained interest rate hike expectations, with CME FedWatch showing traders pricing in about a 56% chance of at least one U.S. rate hike by year-end, with U.S. Treasury yields falling to 4.46% after briefly hitting 4.52%.

If oil prices remain near $95-$100 and the ETF’s outflow streak extends into a second week, Bitcoin will trade as a high-beta risk asset in a tightening environment, just as it has been doing for the past two weeks.

The traditional CME gap of just below $70,000 sits within the current price range, and a full break below this would remove the last nearby technical reference point. Citi’s recession Bitcoin scenario targets $58,000 and is relevant if interest rate hike expectations persist and the dollar continues to strengthen.

| scenario | trigger | New market signals to watch | Impact on BTC |

|---|---|---|---|

| Bullish catch-up | Crude oil has cooled, stock prices remain strong, and ETF flows are in the opposite direction. | Monday’s liquidity supports weekend prices | BTC regains resistance at $80,000-85,000 |

| neutral digestion | Oil prices remain high but stable; ETF flows are mixed | Basis and option skew stabilized | BTC carves out $70,000-$80,000 legacy gap zone |

| bearish breakdown | Oil prices are between $95 and $100, interest rate concerns persist, and ETF outflows continue | Monday’s liquidity touts weekend strength | BTC loses traditional gap area below $70,000 |

| stress case | Defensive hedging accelerates as USD/yields rise | Use CME 24/7 for downside exposure | Citi-style $58,000 recession target in sight |

CME’s 24/7 launch gives financial institutions a better hedging tool that can be used to build downside exposure as the macro environment moves toward defensive positioning.

More efficient access to CME at 2am on Saturday is an improvement in the market’s plumbing environment and has nothing to do with price direction at a time when yield expectations are rising.

The classic CME gap trade gave Bitcoin a visible chart-based signal that drew institutional attention back to a specific price level regardless of macro conditions.

The direction of ETF flows, the depth of Monday’s liquidity, futures basis movements, and options skew are now in play.

This week’s price action will show whether the new regime produces cleaner price discovery or removes one of the few signals pulling BTC back from the macro-driven turmoil.

(Tag translation) Bitcoin