The SEC on May 22 approved Nasdaq PHLX’s proposed rule changes to list Nasdaq Bitcoin Index options, clearing an important regulatory step toward implementing cash-settled Bitcoin volatility trading within the U.S. listed options infrastructure.

The contract (ticker QBTC) is cash-settled in USD against the Bitcoin benchmark and fits into the same account and margin framework used for stock index options.

This will allow QBTC to enter the cash-settled Bitcoin options market, eliminating the need for investors to hold BTC or use crypto-native derivatives exchanges.

Trading will only begin if the CFTC grants the necessary exemptions and the OCC receives approval to update its options disclosure document, which would reshape what Bitcoin can be in the machines Wall Street uses every day.

Spot Bitcoin ETFs offer traditional investors regulated price exposure to BTC, and these ETF options have added hedging and speculative tools tied to specific fund stocks. This difference is important because Bitcoin ETF options track the fund’s shares, whereas Nasdaq Bitcoin Index options directly reference the Bitcoin benchmark.

QBTC creates an options market centered around the Bitcoin exposure itself, priced based on real-time Bitcoin benchmarks and cleared through OCC’s standard infrastructure, within a publicly traded index option stack.

The SEC order describes the contract as European-style, PM-settled, cash-settled, and that the final settlement value is based on the Bitcoin benchmark BRRNY at the New York closing price synchronized at 4:00 p.m. ET.

The underlying index is the CME CF Bitcoin Real-Time Index (BRTI) divided by 100, and the CF Benchmark calculates the index value every 200 milliseconds during the trading day.

Nasdaq argued in its filing that the index option will allow Spot Bitcoin ETF investors to hold QBTC contracts in the same brokerage account and under the same margin regime as the ETF exposure, integrating Bitcoin risk management into existing brokerage account workflows.

| product tier | What it gives investors | market infrastructure | limit |

|---|---|---|---|

| Spot Bitcoin ETF | Regulated BTC price exposure | Securities account/ETF wrapper | Mainly directional exposure |

| Bitcoin ETF options | Hedging and speculating on ETF stocks | Listed options for specific funds | Fund-specific exposure |

| CME Bitcoin Futures/Options | Institutional derivatives exposure | futures market infrastructure | Dynamics of futures accounts, margin and basis |

| Cboe Bitcoin ETF Index Options | Spot Bitcoin ETF Basket Cash Settlement Options | Listed index option frameworks | Indirect BTC exposure through ETF basket |

| Nasdaq QBTC | Cash settlement options for Bitcoin index exposure | Stock index option stack/OCC clearing | Will not be released until CFTC and OCC conditions are cleared |

Infrastructure that Bitcoin is entering

Bitwise CIO Matt Hogan said when Nasdaq first sought approval that Bitcoin options were essential for the asset class to fully normalize.

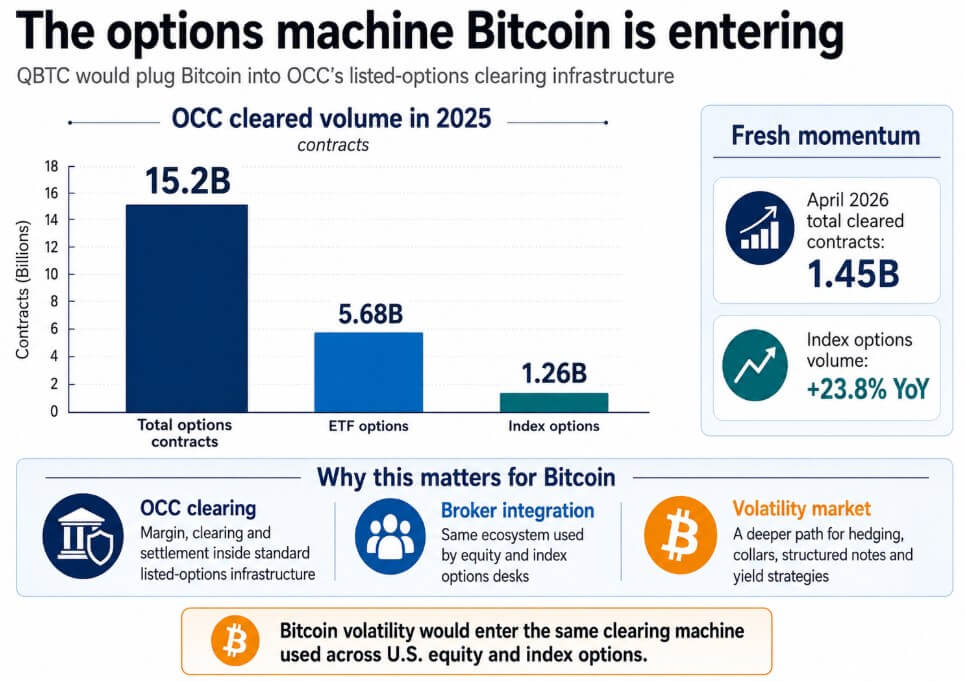

The infrastructure that will enable that normalization is the OCC, a clearinghouse that processed 15.2 billion options contracts in 2025, including 5.68 billion ETF options and 1.26 billion index options.

In April 2026 alone, the OCC settled a total of 1.45 billion contracts, with index option trading volume increasing 23.8% year-over-year.

OCC Clearing is an operational bridge between Bitcoin volatility products and the same risk system used by stock index desks.

Bitcoin index options will enter the OCC clearing machine, which will handle all margin processing, intermediary integration, and market maker relationships associated with the infrastructure, placing Bitcoin volatility within the same portfolio margin system and volatility desk that equity indexes use.

Cboe already offers cash-settled Bitcoin index products, including the Bitcoin US ETF Index Option and the Mini Bitcoin US ETF Index Option, which are European-style contracts based on the US-listed spot Bitcoin ETF index.

Nasdaq’s QBTC uses BRTI as its underlying asset, tying the value of the contract directly to the spot price of Bitcoin.

The SEC noted that as of April 29, Bitcoin’s spot market capitalization was approximately $1.52 trillion, and noted that the proposed position and exercise limits would represent 0.12% of Bitcoin outstanding.

These are limits set by the SEC to constrain the product’s footprint relative to the underlying Bitcoin market while allowing for meaningful institutional size.

Nasdaq PHLX will be able to list and trade QBTC only if it receives a CFTC exemption, meets all relevant conditions, and receives OCC approval to update its options disclosure document.

The approval itself leaves open whether these limits will remain in place under stress and whether the CFTC will process the exemption on a schedule that would allow trading in 2026.

QBTC Options Market Maker Test

If CFTC exemption relief and OCC approval are obtained, and market makers deploy capital at tight spreads, Bitcoin will gain a deep liquid volatility surface within the equity options infrastructure, giving banks and asset managers a toolkit to build collars, buffer notes, downside protection strategies, and volatility selling yield structures based on BTC.

One QBTC contract is equivalent to approximately 1 Bitcoin notional value at a multiplier of $100, and at approximately $76,593 Bitcoin, 10,000 contracts is equivalent to approximately $766 million notional value.

Covered Call Bitcoin ETFs have already demonstrated that yield-generating structures built on top of BTC carry real retail and advisor demand. Exchange-listed index options provide these strategies with a more reliable clearing platform and cleaner underlying assets.

If the CFTC were to delay exemptions or add conditions that complicate Nasdaq’s product design, it would reduce participation by market makers.

IBIT options and Cboe’s ETF index options continue to capture the regulated Bitcoin options market, while the approval remains symbolic as wide spreads prevent institutional investors from using them and spreads continue to widen.

QBTC enters that market and builds a dealer and intermediary network from scratch without the market maker savvy IBIT options that accumulated with the introduction of ETFs.

| scenario | what happens | Signals to monitor | Impact on the Bitcoin market |

|---|---|---|---|

| bull case | CFTC/OCC approval is clear, market makers are quoting tight spreads | Strong opening volumes, narrow bid-bid spreads, institutional flows | BTC gains deeper listed volatility surface |

| basic case | QBTC launches but gradually grows alongside IBIT options and Cboe ETF index options | Moderate trading volume, ETF hedging use case, gradual broker introduction | Gradual improvements to BTC risk management tools |

| bear case | CFTC relief is delayed or product design is complicated | No release schedule and weak dealer commitment | Recognition remains symbolic |

| liquidity trap | Product launches, but spreads remain wide | Low open interest, thin depth and limited market maker capital | Financial institutions continue to use IBIT options or futures instead |

The SEC’s approval reflects that Bitcoin is a $1.52 trillion asset class that includes spot ETFs, CME futures, ETF options, and pending exchange-traded index option products aligned to the closing mechanism of the U.S. market.

Options on the Nasdaq Bitcoin Index indicate that Bitcoin’s next institutional step will be through options clearinghouses, margin systems, and structured products desks, and the SEC has now confirmed that it is open to moving forward with that integration.

(Tag translation) Bitcoin