Was Donald Trump substantively positive about Bitcoin? This is an uncomfortable question for many Bitcoin supporters, including myself.

My political criticism of Trump is considerable and has been for many years. They extend far beyond policy disagreements to questions about rhetoric, institutional behavior, and the broader political culture surrounding the presidency.

None of that will go away just because Bitcoin performed well during parts of his administration, or because parts of the industry now consider him an ally. Still, the issue is important as Bitcoin is increasingly integrated into national policy, capital markets, and geopolitical competition.

Once that happened, it became more difficult to distinguish between political preferences and analytical judgments. The reason this question deserves a serious answer is simple. No modern U.S. president has come as close as Trump to formal government approval of Bitcoin.

That doesn’t make him a “good guy for Bitcoin” in the full sense of the word. Price increases alone are not enough. Poor campaign rhetoric. Political branding is insufficient.

The real test will be whether Bitcoin becomes institutionally more durable, legally defensible, and less likely to be alienated by future governments.

There is stronger evidence on this narrow issue than many critics like me would like to admit.

President Trump’s Bitcoin legacy will depend on whether political approval translates into durable institutional protection.

So, digging into it, Donald Trump was positive on Bitcoin in a significant and provable way. That is, he has brought Bitcoin closer to the center of US government policy than any previous president.

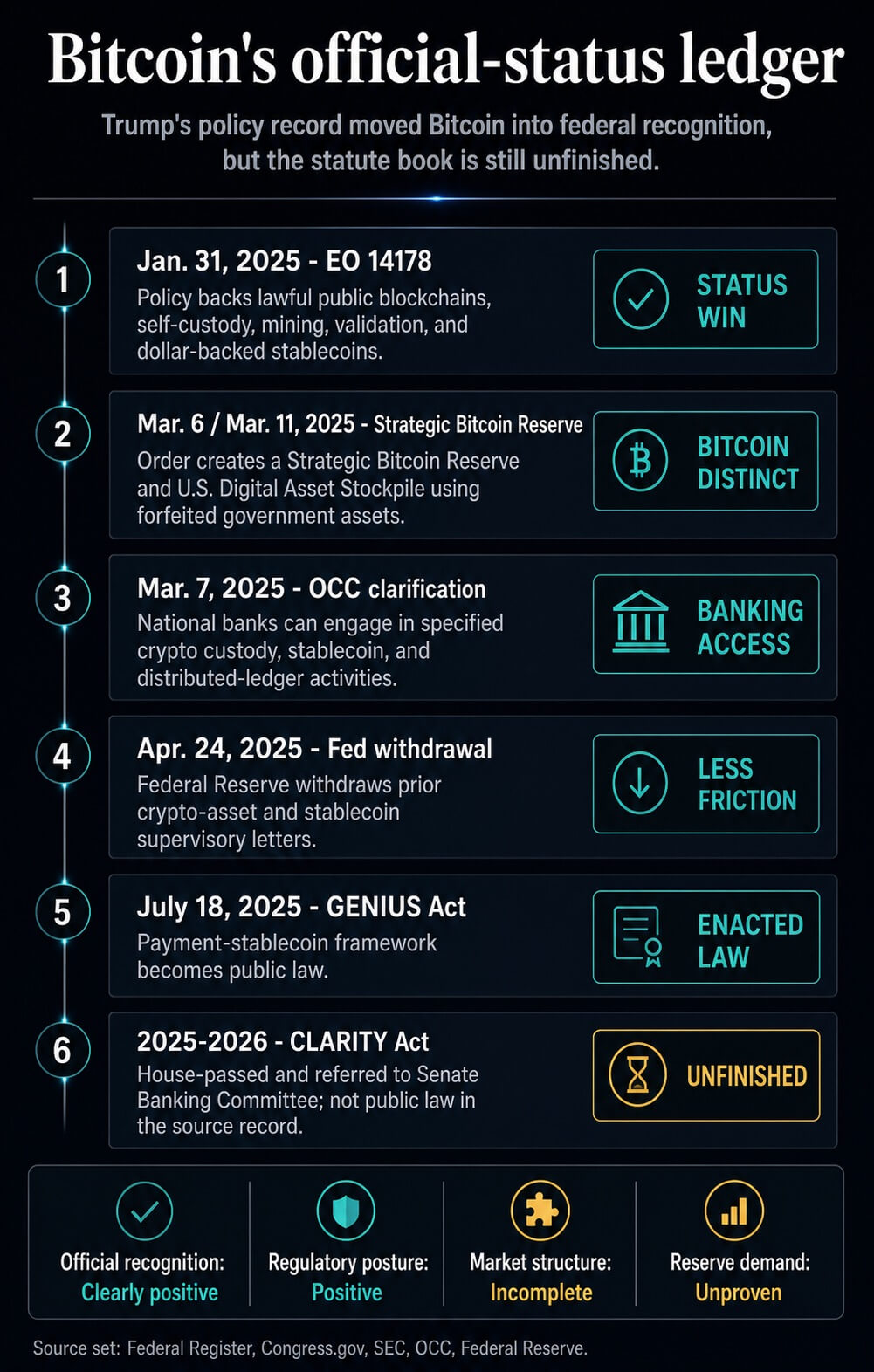

The clearest evidence comes from federal records. So, an executive order supporting the legal use, self-custody, mining, and verification of public blockchains is followed by another order creating the Strategic Bitcoin Reserve and the U.S. Digital Asset Reserve.

This change changed Bitcoin’s political ceiling. The U.S. government stopped treating it only as an asset to be policed, taxed, and liquidated, and began describing it as something the nation could hold as a reserve asset.

For investors and institutions, this reduces the risk of a perceived federal ban or hostile banking policy returning unchanged.

The broader record is less extensive. Price trends vary. Although regulations have improved, the law surrounding Bitcoin itself is still incomplete.

However, public trust remains weak. Blockchain has not yet shown a simple adoption boom. Cryptocurrency businesses linked to Trump pose other reputational issues that Bitcoin supporters cannot ignore by saying the protocol is apolitical.

So the answer varies from ledger to ledger. President Trump’s Bitcoin record is strongest when government approval, institutional access, and political permission are tested.

It is weaker when tested for price durability, public confidence, durable legislation, or the use of organic base layers.

| ledger | what the evidence shows | verdict |

|---|---|---|

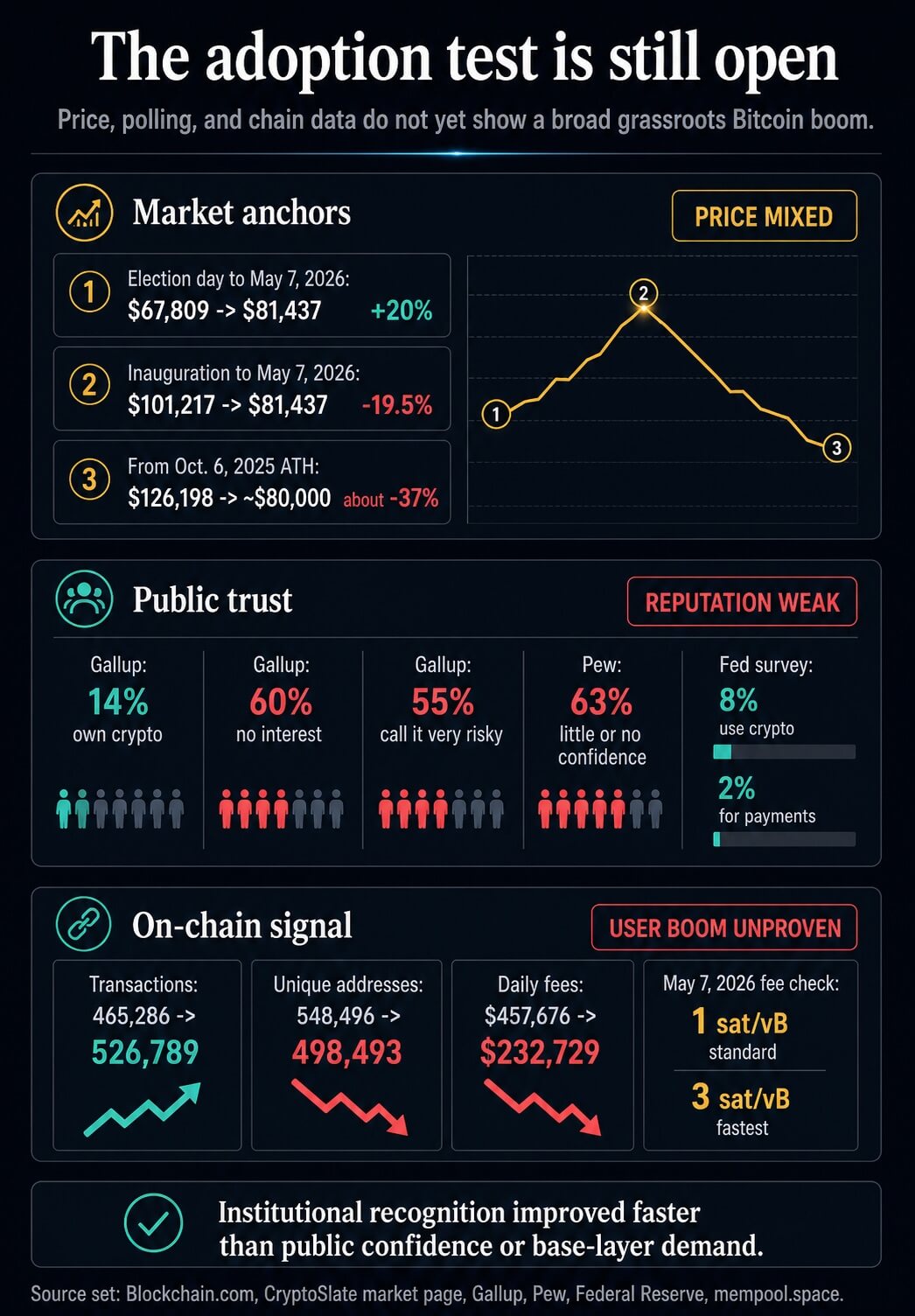

| price | It rose from Election Day and fell from Inauguration Day and preliminary orders, leaving it about 37% below its October 2025 high. | mixture |

| ideological position | Public blockchains, mining, self-custody, and Bitcoin reserves are now clear U.S. policy positions. | obviously positive |

| regulation | Although the stablecoin law and the attitude of government agencies have improved, the market structure law is incomplete. | positive but incomplete |

| public reputation | Polls continue to show low ownership, high risk perception, and weak trust. | weak |

| On-chain use | Selected endpoints saw an increase in transactions, but addresses and rates did not show widespread base layer demand. | not proven |

Prices and policies tell different stories

The case for pricing depends on where you start your measurements. Bitcoin was hovering around $67,800 on November 5, 2024, and around $80,700 on May 10, 2026.

From its election day anchor, Bitcoin has risen about 20%. This supports the view that Trump’s victory, policy signals, and broader post-halving cycle coincided with meaningful market repricing.

Other politically relevant anchors provide weaker readings. On January 20, 2025, the day President Trump was inaugurated, Bitcoin was worth about $101,200.

It was around $90,600 on March 6, 2025, when the Strategic Bitcoin Reserve order was signed. Measured in terms of those points, the market is lower.

crypto slate Also on the Bitcoin page, BTC is at a level of just over $80,000 this weekend, which is about 37% below the all-time high of $126,198 on October 6, 2025.

Honest price judgments vary. Trump-era policies helped create a more friendly backdrop, and Bitcoin hit new highs during that period.

Current price action still falls short of proving that the Trump premium is permanent. This shows that subsequent gains have given back most of that gain, with the market turning positive from Election Day but negative from Inauguration Day.

Policies strengthen Trump’s case. Executive Order 14178 made it explicit U.S. policy to support the use of legitimate digital assets, including public blockchain networks, self-custody, mining, validation, and dollar-backed stablecoins.

Executive Order 14233 went a step further and established the Strategic Bitcoin Reserve, giving Bitcoin different treatment than other digital assets in the federal stockpile.

That’s a real status change. This changes Bitcoin from something that was primarily seized, sold, or discussed by the U.S. government to something that the government says it will hold as a reserve asset.

It also creates a political fact that if future regimes want to return to a more adversarial posture, they will have to openly reverse course.

Restrictions are equally important. This reserve mandate only allows for budget-neutral acquisition strategies that utilize confiscated government BTC to leverage reserves and impose no additional cost to taxpayers.

The immediate effects of reserves are recognition, storage, and potential restraint from selling pressure. New sovereign demand will require acquisition experience, which is currently lacking.

Regulations follow the same pattern. The GENIUS Act was enacted as federal law, creating a framework for payment stablecoins.

The SEC’s SAB 122, the OCC’s March 2025 clarification, and the Federal Reserve’s reversal of previous virtual currency guidance have all made the banking and custody environment less hostile.

These are physical changes. The battle over the core Bitcoin market structure is far from over.

The CLARITY Act passed the House and was referred to the Senate Banking Committee, but has not yet become public law.

From a practical standpoint, Trump could make a case for real change in the attitude of the administration and agencies, as well as enacting one major piece of legislation regarding stablecoins. He cannot yet claim that the issue of Bitcoin’s federal market structure has been fully resolved by statute.

Public reputation did not follow official approval

The weakest link in the pro-Trump case is public opinion. Gallup revealed in June 2025 that 14% of U.S. adults own cryptocurrencies, 60% are not interested in purchasing cryptocurrencies, and 55% consider cryptocurrencies to be very dangerous.

Pew’s October 2024 baseline was similarly hostile. 63% of Americans have little or no confidence that cryptocurrencies are reliable and safe, and 17% have ever invested in, traded, or used cryptocurrencies.

These surveys are incomplete in measuring the effectiveness of President Trump’s second term. Pew predates the term, and Gallup predates the subsequent Trump-related crypto controversy.

Even if the timing was tricky, they are showing a starting point and public reaction in the first year. Bitcoin and cryptocurrencies have not yet become trusted mass market institutions because the president has embraced them.

The US Federal Reserve Board (FRB) has added new check items to its household budget survey. In 2024, 8% of adults used cryptocurrency for some purpose, but only 2% used it to buy or pay for something.

This shows that the asset is still primarily understood as a speculative or investment product rather than an everyday financial tool.

This is where reputation ledgers and official status ledgers come into conflict. Reserve orders could change the way fund managers, bank compliance teams and public market investors assess political risk.

Governments have far less influence over households formed by currency failures, fraud, meme coin cycles, and partisan suspicions. Public recognition can reduce institutional fear while leaving public distrust largely intact.

Trump’s personal and family ties to cryptocurrencies further complicate the reputation ledger. Associated Press reporting on President Trump-related crypto business connections and igcurrencynews reporting on surveillance surrounding World Liberty Financial support credible conflict of interest concerns.

The source records support the reputational and ethical risks as well as the context of the allegations. It falls short of proving criminal activity or showing that the Bitcoin protocol was compromised.

For Bitcoin, that distinction is uncomfortable.

Yet public reputation is built through connections, not just technical design. The president could strip Bitcoin of its official status while simultaneously making the cryptocurrency seem more self-serving to people who already distrust it.

Chain data leaves case studies unproven

On-chain evidence is another major constraint to net-positive claims. According to data from Blockchain.com, the number of daily confirmed transactions increased from 465,286 on November 5, 2024 to 526,789 at the end of last week.

This is a positive endpoint comparison. Unique addresses per day on the same endpoint decreased from 548,496 to 498,493, and transaction fees per day decreased from approximately $457,676 to approximately $232,729.

These numbers should be treated with caution. Unique addresses are a poor proxy for people, and daily endpoints can be distorted by batch processing, exchange flows, transaction configurations, and non-monetary activities.

Still, they fail to support the clear argument that President Trump’s policy shift has brought a wave of base-layer users to Bitcoin.

Independent on-chain analysis points in the same direction. Glassnode explained the disconnect between BTC price growth and quiet network activity such as low fee pressure and dominance by large companies in 2025.

Separately, Galaxy claimed that the fee pressure eased after Rune and Ordinal activity subsided in the second half of 2024.

A check of mempool.space also shows the price market at a quiet point in time, with 1 sat/vB recommended for 30 minute, 1 hour, economy, and lowest price targets, and 3 sat/vB recommended for fastest confirmation.

The situation is more mixed than bearish in any sense of the word. Lower fees make Bitcoin cheaper to use, and higher prices likely reflect demand from institutional investors moving through ETFs, custodians, treasuries, and off-chain venues rather than an increase in base-layer transactions.

It limits adoption claims. President Trump’s Bitcoin effect appears to be stronger in official approvals and institutional channels than in day-to-day demand for block space.

Source records support conditional answers. Trump is positive about Bitcoin’s ideological status and institutional access.

He turned support for public blockchains into administrative policy, created a version of the Strategic Bitcoin Reserve, endorsed a more friendly government stance, and signed major stablecoin legislation to support crypto market infrastructure.

The rest of the ledger is weak. Bitcoin price has been positive since election day, but negative since the inauguration and the pre-order anchor.

Although the reserves are real, there is no hard evidence of an active savings program by the government. The market structure law remains incomplete. Public trust remains low.

There is no simple grassroots boom in on-chain activity. Even without proving criminality, Trump-related crypto disputes undermine trustworthy reputations by association.

The most defensible answer is yes, in a limited sense. President Trump was a net positive in that the main tests were government approval, institutional access, and political permission.

Although he is not yet clearly net positive, Bitcoin’s broader legitimacy ultimately needs to be demonstrated: public trust, durable laws, and the use of organic networks.

The next developments that could change the decision are specific reserve accounting, new records in BTC acquisitions, eventual market structure legislation, changes in public opinion data, and sustained on-chain demand that cannot be explained primarily by speculation or institutional custody flows.

(Tag translation) Bitcoin