Bitcoin’s macro settings are increasingly tied to the same forces driving the S&P 500 to new highs: liquidity, concentration, interest rate expectations, and investor tolerance for overvaluation.

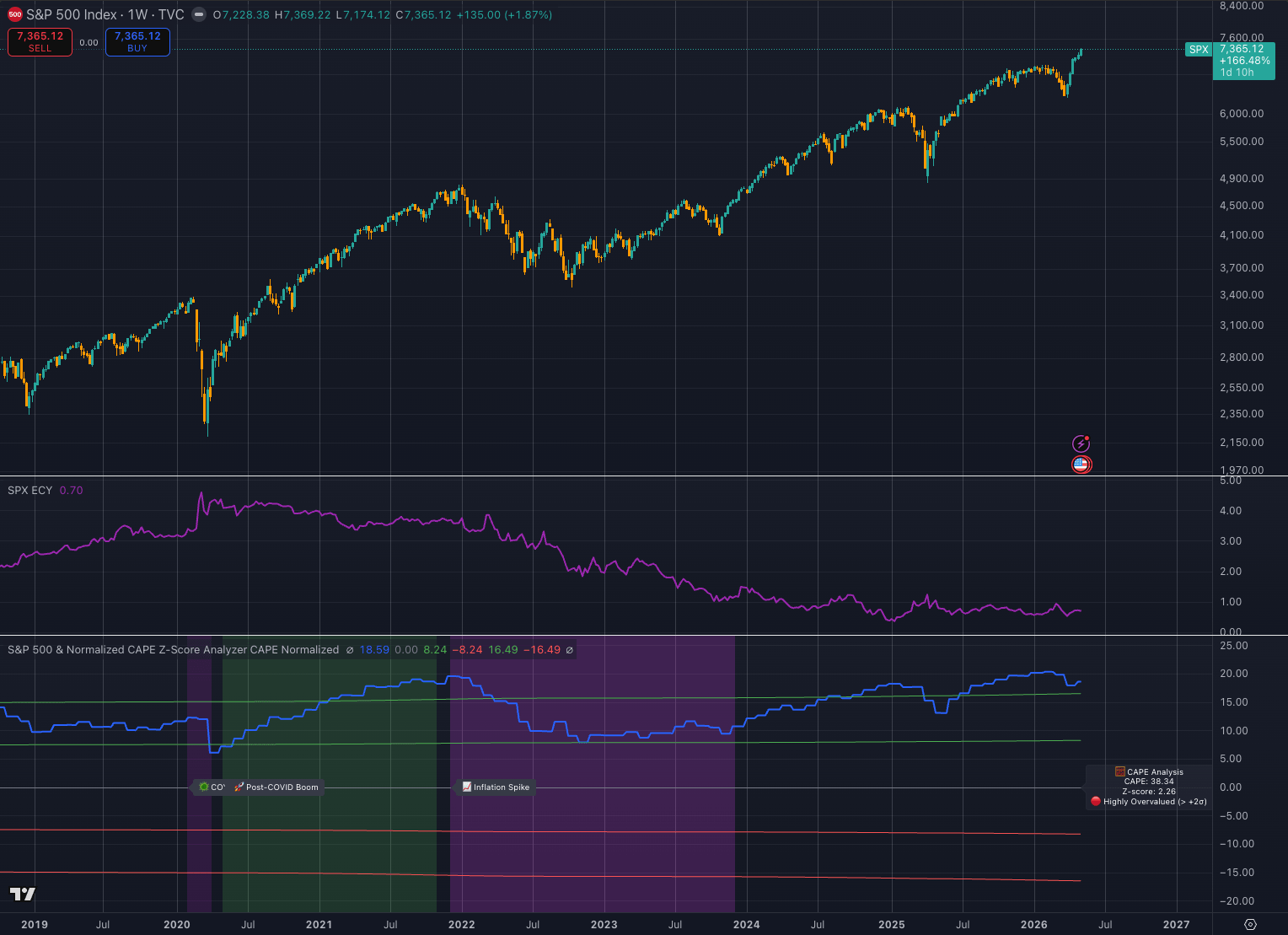

The current composition of the S&P 500 indicates that the index remains in a strong long-term uptrend, with the price hovering around 7,365 on the weekly chart, while the valuation metric is in historically high territory.

This combination adds clear conditions and creates a constructive backdrop for Bitcoin in the short term.

BTC can profit while the stock price trend holds.

Vulnerability increases when expensive stocks begin to roll under the weight of interest rates, earnings pressures, or volatility.

The current market regime is best understood through the three tiers of the S&P 500 chart below.

The first layer is price.

The index continues its long-term progress, with higher highs and lower lows through the dot-com crash, the global financial crisis, the coronavirus shock, the 2022 monetary tightening cycle, and the latest phase of AI-driven stock concentration.

The second layer is the equity risk premium style signal, indicated by the SPX ECY reading around 0.70.

This level suggests that investors are accepting that the rewards for owning shares are low relative to the interest rate environment.

The third layer is evaluation.

The normalized CAPE Z-score analyzer shows that the CAPE reading is around 38.34 and the Z-score is around 2.26, putting the market in the chart’s highly overvalued zone.

The independent CAPE dataset, which includes Shiller PE ratios, shows a similar broad picture. In other words, U.S. stocks are expensive relative to their long-term history.

In the case of Bitcoin, the conclusion is straightforward.

The current equity structure will continue to support high-beta assets as long as investors continue to treat expensive valuations as a hallmark of a sustainable growth regime.

BTC sits further out of the risk curve than the S&P 500 and Nasdaq.

When macro confidence expands, Bitcoin typically receives an amplified version of its capital flows.

When macro confidence declines, Bitcoin typically absorbs amplified drawdowns.

Stock valuations are trending upward, but Bitcoin’s risk appetite remains supported

The S&P 500 chart shows how the market is overvalued while maintaining trend control.

This distinction is central to Bitcoin.

If earnings, liquidity, and story strength are aligned, overvalued markets can continue to rise over time.

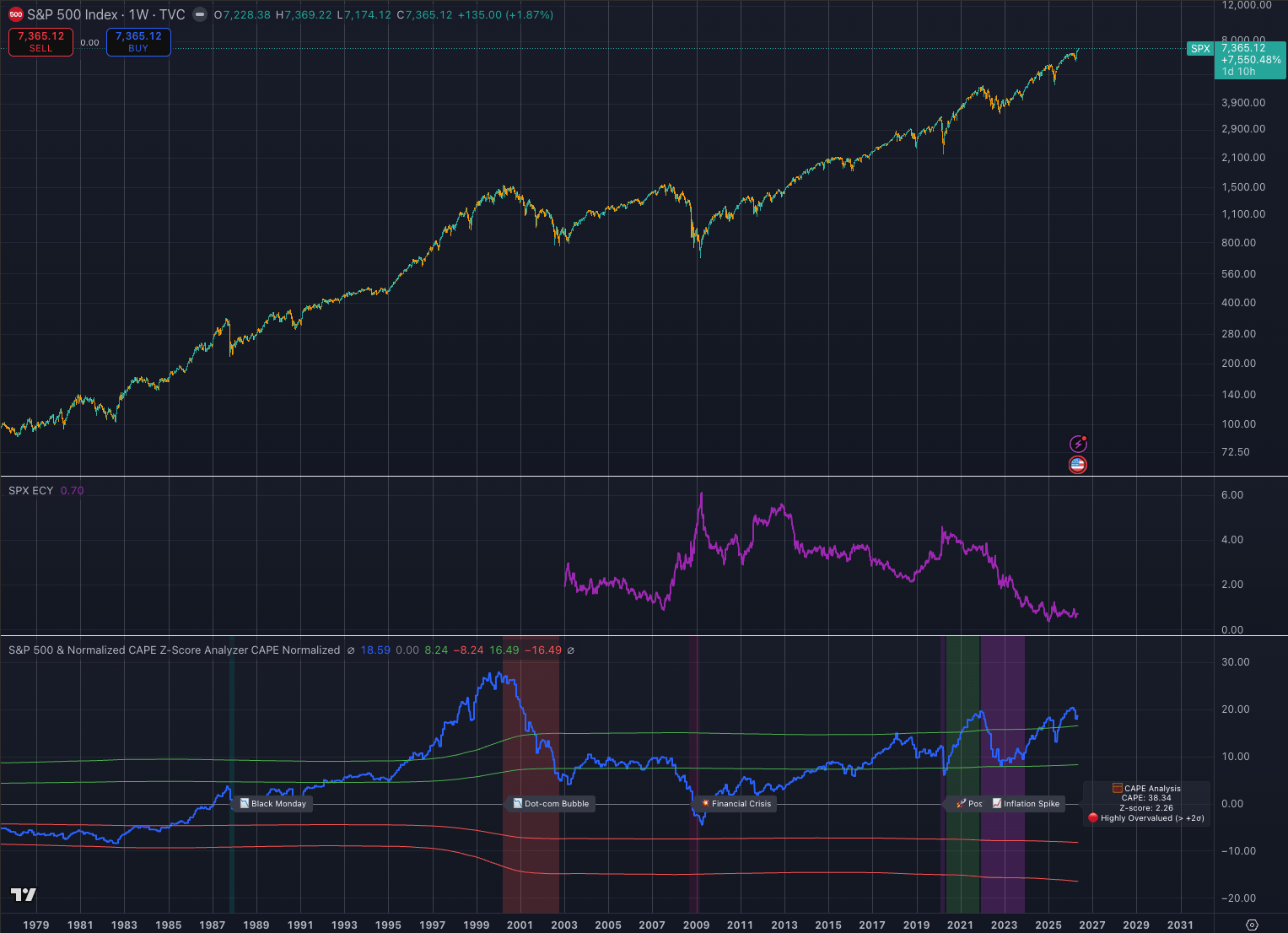

The late 1990s showed how far technology-driven cycles can go before evaluation discipline returns.

The 2020 and 2021 cycles showed how volatile risk assets can be when combined with expanding liquidity, falling real yields, and speculative capital.

The 2022 cycle showed the other side of the equation, with rising interest rates compressing duration assets and exposing positioning congestion.

The current setup borrows from all three periods.

As in the dot-com era, leadership is focused on innovative technology themes. In a recent article, we also highlighted this comparison and potential red flags.

In the late 1990s, the Internet provided a powerful rationale to justify higher multipliers.

Now, AI is filling that role.

The index has become increasingly reliant on a small number of large-cap technology companies, the so-called Magnificent Seven, which account for much of the S&P 500’s performance and index weight.

When leadership works, its focus provides significant upside potential for the index.

And when leadership weakens, the margin for error also narrows.

However, today’s leading companies have large revenue bases, high profit margins, and significant free cash flow, making the current stock cycle a stronger revenue base than the speculative Internet bubble.

Still, operational market signals remain late-cycle in nature.

Although the S&P 500 index is rising, valuation support is thin, risk premium compensation is compressed, and the index relies heavily on market confidence in future productivity gains.

Bitcoin tends to perform well in exactly such environments.

When equity investors accept valuation growth in exchange for future growth, crypto investors often move further along the same curve.

That is why the current S&P 500 setup is constructive rather than immediately bearish for BTC.

The chart shows a market with an execution price.

Bitcoin will grow when execution risk is undervalued, liquidity is available, and investors believe the next phase of growth will justify today’s valuation premium.

In this regime, BTC acts as a high beta expression of macro confidence rather than as a defensive hedge.

Therefore, the short-term impact is positive.

If the S&P 500 maintains its weekly trend, volatility remains subdued, and AI-driven profit expectations continue to attract institutional investors, Bitcoin should remain in favor.

Even with rising stock market valuations, BTC could rise further as allocators are more willing to pursue convexity.

Because Bitcoin has a smaller capital base, is more reflexive, and has a more direct relationship to liquidity expectations, Bitcoin’s gains in this setting could outpace stock market movements.

Bitcoin now trades through the same liquidity channels as high-beta technologies

Bitcoin’s sensitivity to stocks has changed over time.

Previous cycles were more isolated, driven by narrative halving, offshore leverage, crypto-native liquidity, currency flows, and retail speculation.

Those forces still exist, but the institutional market structure is now larger.

The SEC’s approval of spot Bitcoin exchange-traded products in January 2024 resulted in a change in access tiers.

BTC is now easier to hold within traditional portfolios, easier to model as a macro allocation, and easier to trade as part of a broader risk basket.

This change has two effects.

First, Bitcoin has a stronger structural demand channel than in previous cycles, as access to ETFs attracts more potential buyers.

Second, Bitcoin is more exposed to the same macro variables that drive institutional investor portfolios.

Investors who use the S&P 500, Nasdaq, gold, Treasury futures, and volatility products to express a macro view can now use Spot Bitcoin ETFs in the same allocation stack.

This makes BTC more liquid, more legal, and more tied to conditions between assets.

Therefore, the S&P 500’s valuation signal is relevant to Bitcoin because it indicates where risk appetite stands within the broader portfolio system.

If the CAPE value is near 38 and the Z-score is greater than 2, the stock is in rare valuation territory.

This will not trigger an automatic sell signal.

It reduces the market’s tolerance for disappointment.

At these levels, investors need returns to validate prices, interest rates to avoid new pressures, and liquidity to remain available.

If these conditions apply, Bitcoin can be profitable.

If any of these supports weaken, vulnerability increases.

The rate channel is particularly important.

Bitcoin performs best when real yields fall, liquidity expands, and the opportunity cost of holding non-yielding assets falls.

The Fed’s target rate framework, visible through data series such as the Federal Funds Target Range, remains a central input for all duration-sensitive assets.

When the market expects policy easing, Bitcoin often rebounds before the easing materializes.

When policies are restrictive for long periods of time, speculative assets lose some of their valuation support.

The current stock price chart shows that risk assets were able to rise despite the higher interest rate regime.

That’s an important signal.

This suggests investors view earnings strength, AI-related capital spending, and future productivity as strong enough to offset the drag from interest rates.

Bitcoin interprets its environment as permissive.

If capital continues to flow into high-conviction growth themes and institutional investors continue to look for assets with asymmetric upside potential, BTC does not need to raise its zero rate.

While ETF access strengthens Bitcoin’s upside, it becomes more closely tied to macro stress

BTC can remain constructive even with stock prices stretched because in 2020 and 2021, the market is no longer in a pure liquidity regime when stimulus and ultra-low interest rates overwhelmed almost all other inputs.

The current settings are more selective.

Capital rewards assets at the intersection of scarcity, technology, liquidity, and institutional adoption.

Bitcoin qualifies for that framework.

The risk is that the inclusion of institutional investors gives portfolio managers greater credibility as they collectively reduce risk, while at the same time making it easier to sell.

Historical markers on charts provide a useful framework for Bitcoin.

The dot-com era shows how technology stories can push valuations far beyond traditional comfort levels before the cycle dries up.

The 2008 financial crisis shows how dangerous valuations and leverage can be when the underlying financial system fails.

The period of 2020 and 2021 shows how liquidity can dramatically drive Bitcoin up when risk appetite expands.

The 2022 inflation shock shows how quickly BTC can reprice when interest rates rise, liquidity tightens, and investors stop paying premium multiples for long-term assets.

The current environment is the closest to a convergence of dot-com concentration, post-COVID risk appetite, and post-2022 interest rate discipline.

That blend is rare.

Stocks are expensive, but the index is still rising.

Interest rates are still higher than they were in the zero-rate era, but investors are still willing to buy growth.

AI has replaced emergency liquidity as the main reason justifying higher valuations.

Bitcoin has replaced purely retail-driven speculation with a more organized demand channel.

This indicates that the S&P 500 trend holds, while the outlook for Bitcoin is positive.

If the stock price continues to rise, money could flock to BTC for three reasons.

- Investors become more comfortable moving outward on the risk curve.

- Bitcoin has a more convex representation of liquidity reliability than large-cap stocks.

- Structural ETF channels allow institutional flows to reach BTC without the operational friction that defined previous cycles.

The most important market signal is whether the S&P 500 is still expensive and trending, or expensive and failing.

The first condition supports Bitcoin.

The second condition threatens it.

The weekly SPX trend continues to make new highs, indicating that investors are still willing to absorb valuation risk.

A failed breakout, narrowing, increased volatility, or weak AI leadership will change the signal.

Bitcoin would then be less likely to be traded as digital gold and more likely to be traded as highly liquid beta.

Although stock price momentum is maintained, Bitcoin continues to perform well

There is precedent for that action.

In March 2020, BTC was sold off during the liquidity shock and subsequently became one of the biggest beneficiaries of the policy response.

Bitcoin plummeted in 2022 as an inflation shock and the Fed’s tightening cycle compressed speculative assets.

BTC outperformed stocks in late 2020 and early 2021 as increased liquidity concentrated capital into the most reflective assets.

These episodes show that Bitcoin’s long-term scarcity narrative can coexist with short-term macro liquidations.

Under stress, liquidity is paramount.

For now, the charts favor continuation over immediate defensive positioning.

The price structure of the S&P 500 remains bullish.

The valuation is extended, but the extension is rarely the end of the cycle.

The market needs a catalyst to turn overvaluation into aggressive repricing.

This could be triggered by earnings disappointments, a resurgence of inflationary pressures, the Fed’s path to higher long-term interest rates, credit stress, or a loosening of mega-cap AI leadership.

Until that catalyst emerges, Bitcoin has room to continue benefiting from the same macro confidence-boosting stocks.

The practical signal is that BTC remains in a favorable but vulnerable situation.

The bullish case is strongest while SPX maintains its trend, volatility is subdued, and liquidity expectations stabilize or improve.

In that environment, Bitcoin is likely to outperform as it is on the high beta end of the same risk spectrum.

The risk case begins when the S&P 500 stops treating high valuations as sustainable and starts reassessing them as vulnerabilities.

Until then, stock charts show that risk appetite continues, and Bitcoin is one of the most obvious beneficiaries of that appetite.

(Tag Translation) Bitcoin