Strategy (formerly MicroStrategy)’s flagship dividend preferred stock is trading at its lowest levels this year, putting pressure on purchases of Bitcoin, one of the company’s most important fundraising tools.

The $10.5 billion floating-rate perpetual preferred stock, which trades under the ticker STRC, closed Tuesday at $91.79.

The settlement marks the third-lowest closing price since trading began in July 2025 and is well below the $100 level that Michael Saylor’s company has been trying to approach.

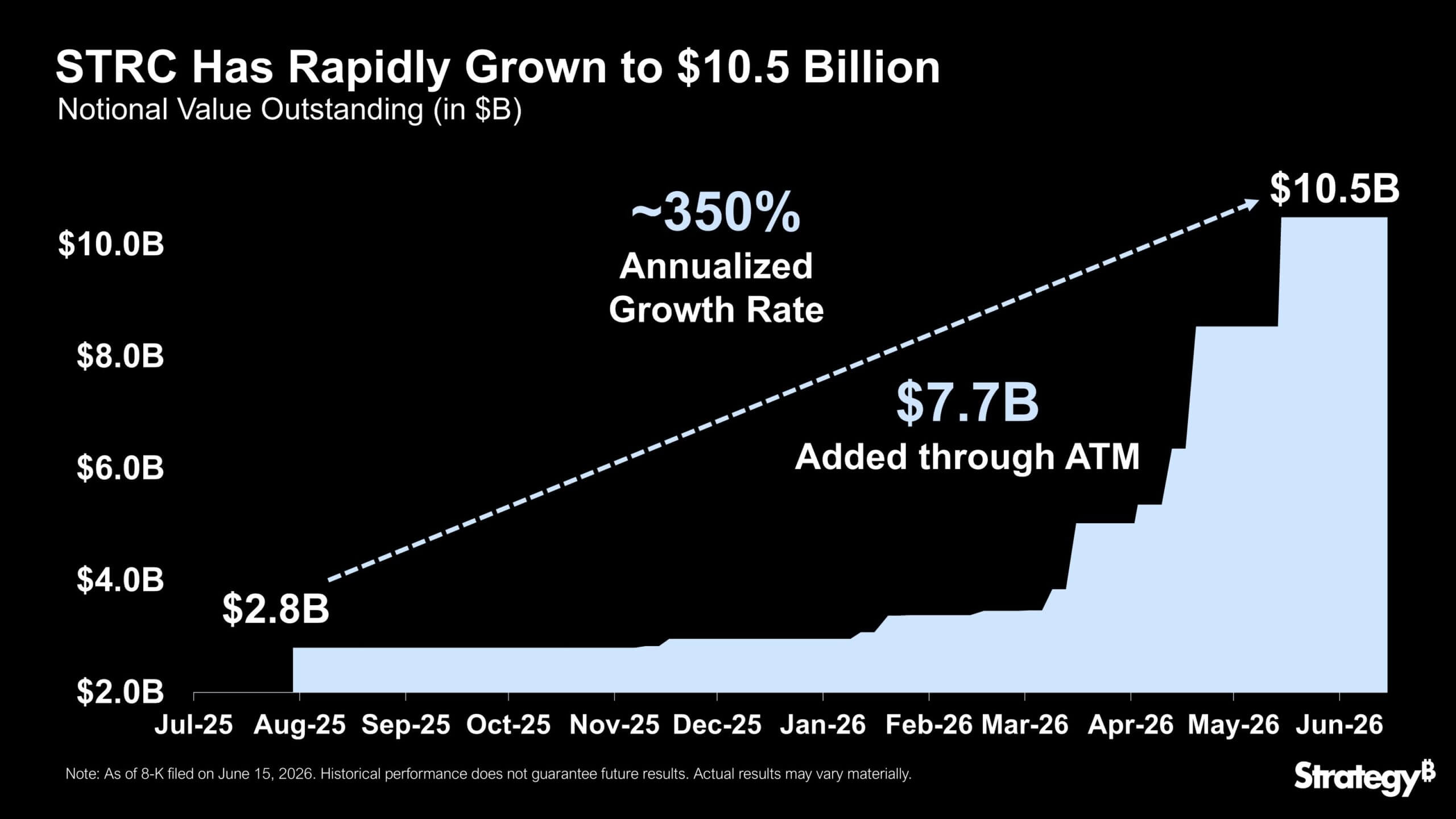

Over the past year, STRC has grown from $2.8 billion to $10.5 billion, with market issuances adding $7.7 billion. This makes it one of the fastest growing financial products in history.

This decline therefore made STRC a live test of investor appetite for Bitcoin-related income products. Strategy has built a vehicle that provides high dividends while giving companies another way to raise capital.

But the market is now implicitly demanding higher yields as Bitcoin falls, competing preferred stocks offer more attractive terms, and investors reassess the risks associated with expanding the strategy’s capital structure.

Bitcoin rebound reaches priority stack

STRC’s weakness shows how quickly Strategy’s income products can start trading under the same pressures as the underlying assets on the company’s balance sheet.

During the spring, strong demand and rising Bitcoin prices allowed Strategy to keep the STRC dividend rate unchanged at 11.5%. With the stock trading near par, there was little reason for management to raise the dividend.

However, that changed as Bitcoin rolled over and investors began seeking additional rewards for holding preferred stocks associated with companies whose value was heavily exposed to the cryptocurrency.

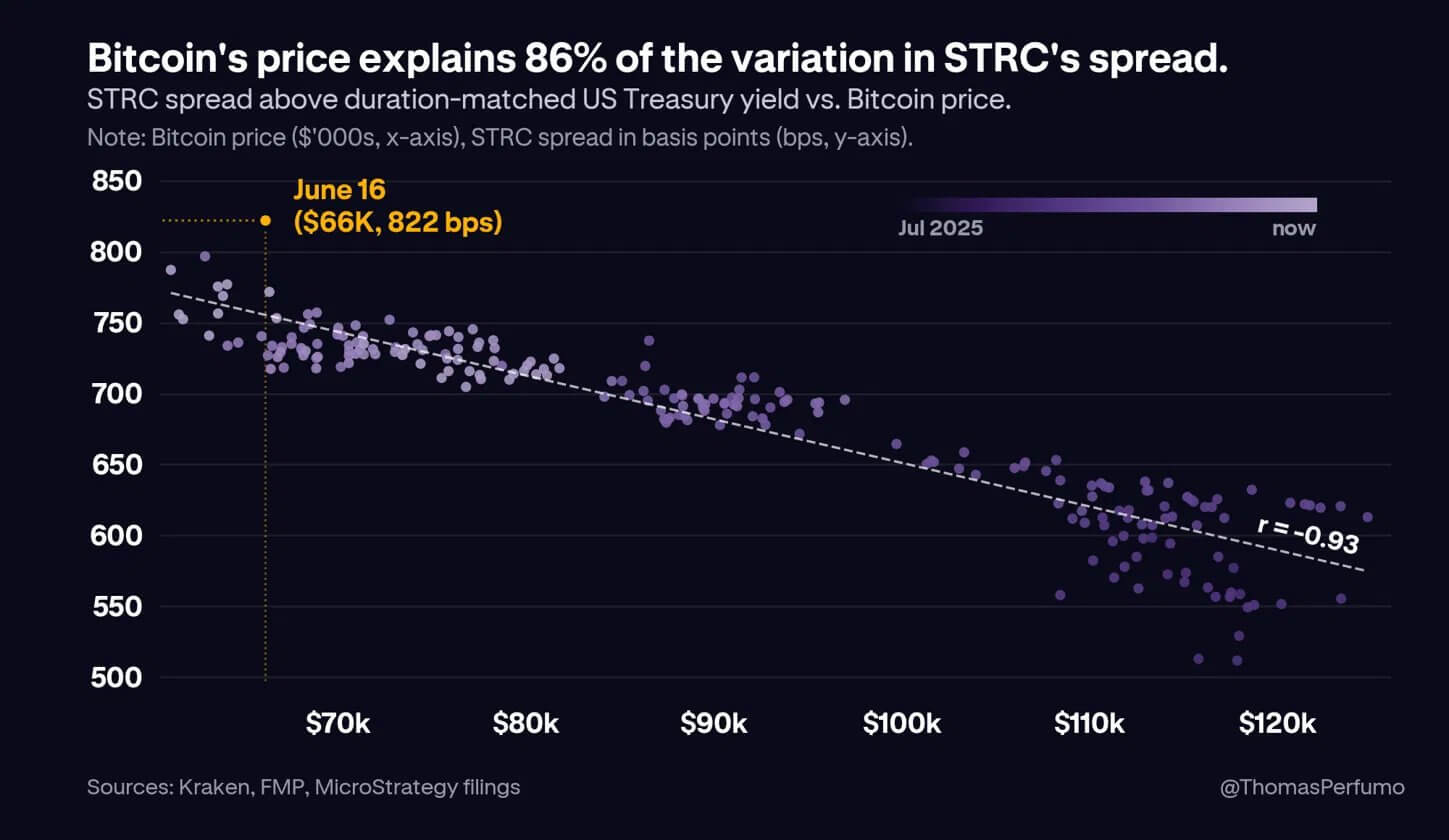

Thomas Perfumo, chief economist at Kraken, said that around 86% of the variation in STRC’s yield spread can be explained by movements in the price of Bitcoin. His analysis suggests that investors are treating STRC less like a stable preferred stock and more like a credit product whose risk premium moves with Bitcoin.

This relationship is not unique to STRC. Other Strategy Preferred Securities such as STRK, STRD, and STRF are also showing pressure.

The difference is that investors expect those products to fluctuate. STRC is being sold with a stronger price stability objective, making it harder for holders to reject its extended discount.

Market calculations are easy. STRC pays an annual dividend of $11.50. At a price close to $92, investors would have earned about 12.6%.

To get the stock back around $100, the strategy will need to move the dividend closer to the yield investors are already demanding. Andre Dragosh, Head of Research at Bitwise Europe, said:

“To bring STRC up to parity levels, Saylor essentially needs to raise its dividend by just over $1.00. Currently, the equilibrium dividend is about $12.60.”

Soft peg problem

STRC’s design gives flexibility to the strategy, but does not force the market to value stocks at $100.

The value of this product is set at $100, and Strategy can adjust the payout rate to encourage trading around that level. However, there is no automatic mechanism to require buyers to intervene at par. This difference is at the heart of the current decline.

Parker White, chief operating officer and chief investment officer at DeFi Development Corp., said the product’s soft anchor of $100 could make it vulnerable to short sellers.

He argued that STRC’s retail investor base expects the stock to remain near parity, and a drop of even a few dollars below that level could cause major concerns.

He said STRC’s borrowing costs are relatively low, so short sellers could take advantage of that reaction.

White continued that the full cost of borrowing is approximately 60 basis points, making the deal cheap to maintain compared to similar products. The strategy’s market issuance program may also limit price increases beyond $100, reducing the risk short sellers face if they take a position in the stock.

This theory gives traders a clear pressure point. If investors treat $100 as a promise rather than a goal, their confidence is likely to weaken each time they move away from that level.

That risk becomes more pronounced as some crypto protocols are built around STRC or use securities linked to the strategy as part of a broader yield strategy. If the decline continues, some holders may be forced to reassess collateral values, liquidity assumptions, and expected returns.

Strive’s SATA raises the bar

White also noted that STRC’s discounts have become more noticeable because rival products have held up better.

Strive’s Bitcoin-backed preferred stock SATA continues to trade near its $100 par value while offering a higher annualized dividend of approximately 13%. Dividends are also paid daily, rather than monthly or semi-monthly, providing investors with quick cash distributions and increasing the short sale price of the product.

This structure strengthens SATA’s appeal among income-oriented investors. Daily dividends reduce the pressure that builds up around the ex-dividend date when holders decide whether to collect their dividends or rotate them elsewhere.

It also increases carrying costs for short sellers and requires them to pay their dividend obligations more frequently.

White estimated SATA’s baseline borrowing cost to be approximately 460 basis points. He said that including the impact of daily dividend obligations, the annualized cost of shorting SATA has risen towards 17.6%, compared to about 60 basis points for STRC.

This comparison puts Strategy in a difficult position. STRC still offers a high stated dividend, but the market tends to favor both higher yields and faster payouts.

STRC restoration is expensive

STRC’s decline leaves Strategy with a narrow path to regaining confidence in one of its most important funding channels.

White argued that the company could stabilize its product by raising the dividend to 12%, calling for a shareholder vote to move to daily payments, increasing the call price from $101 to at least $110, and rebuilding its cash buffer to $2.5 billion.

According to him, the cost of shorting STRC will increase as dividends and daily payments increase. A higher call price gives the stock more room to trade above $100, increasing the risk for traders who bet on it.

Furthermore, the increased cash on hand will alleviate concerns about dividends, which will provide peace of mind for investors who value income.

However, each step has significant trade-offs that can impact your strategy.

For context, increasing the dividend could help bring STRC closer to parity, but it would also increase the strategy’s recurring cash burden. Daily dividends could boost market confidence, but would require other structural changes. Increasing reserves could strengthen creditworthiness, but could slow the pace of new Bitcoin purchases.

The bigger challenge is the investor base. STRC still appears to be heavily owned by Bitcoin native buyers, who are comparing the preferred stock to Bitcoin itself.

If Bitcoin falls, these investors can collect income from STRC or convert it back to Spot Bitcoin at a lower price. This competition is forcing Strategy to offer higher returns than traditional bond buyers would demand.

A broader investor base could ease that pressure. For money market, preferred stock, and bond investors, an 11.5% cash dividend remains significant.

But to attract that capital, STRC will likely need stronger evidence that it can maintain its range even during Bitcoin’s decline.

(Tag translation) Bitcoin