Iran conflict is already disrupting the hidden plumbing of global trade

Markets were monitoring crude oil during the first phase of the Iran conflict. That was the visible layer. Today, the price has fallen below $90 per barrel for the first time in a while, and Bitcoin is rising along with it.

But profound changes are still occurring deep within systems such as shipping, gas, fertilizer, aviation, petrochemicals and trade finance. These channels pose a real economic burden.

These determine delivery times, input costs, working capital, factory schedules, food production, and freight transportation capacity. As pressure shifts to these layers, the economic effects extend far beyond the oil chart.

Its widespread disruption is already visible. Merchant ships in and around the Strait of Hormuz have come under repeated attacks since late February, killing civilian seafarers and leaving thousands of crew members still operating in the waters, the International Maritime Organization said.

UNCTAD said ship traffic passing through Hormuz plummeted to single digits from pre-crisis levels in early March, a sign that physical trade flows were already at a standstill. Commodity shocks change expectations. Shocks during transportation change what can actually be moved.

The economic impact is beginning to expand accordingly. China’s trade data for March showed imports surging while export growth slowed sharply, a combination that points to increased input pressure and weak external demand.

The IMF has signaled slower growth and firmer inflation as the war impacts through global prices and transport routes. What started as an energy shock in the Middle East is turning into a broader supply-side impairment that directly impacts industrial output and financial conditions.

For the cryptocurrency market, that change changes the analytical frame. If liquidity continues to loosen and growth expectations are maintained, the narrow oil rally could be absorbed.

Prolonged disruptions across transportation, fuel, industrial inputs, and cross-border financing will create a different environment. Tight financial conditions, weakening risk appetite, increased volatility in emerging market currencies, and a shift towards more selective capital allocation across digital assets.

Bitcoin could still benefit from an explosion of sovereign distrust and geopolitical stress. As the macro environment deteriorates over time, the broader cryptocurrency complex tends to trade closer to growth-sensitive risks.

This also paves the way for Bitcoin to reassert its role as an inflation hedge. It has already outperformed gold since the start of the year, showing that capital is shifting to higher beta stores of value rather than traditional defensive assets. Despite the noise surrounding ceasefire talks, the price structure remains solid, suggesting resilience rather than reflexive risk-off behavior.

If macro stress continues to transmit through inflation channels rather than outright demand destruction, Bitcoin’s position will shift from a peripheral risk asset to a more central hedge within the digital asset complex.

Therefore, the hidden pipeline of trade will be more related to cryptocurrencies than the initial movement of crude oil alone.

Shipping and gas are moving from commodity stress to physical disruption

The first serious cracks in commercial transportation appeared. While tanker traffic has received a lot of attention, the bigger issue is operational reliability.

Shipowners, charterers, insurers and crews are all reassessing whether this corridor is worth the risk. The IMO’s call for a safe navigation framework speaks to the scale of the problem.

Even if navigation is technically possible, commercial travel could still be curtailed if war risk insurance premiums rise, crews deny passage, or insurers tighten conditions. This creates a drag to survive the initial diplomatic hiatus, as underwriting decisions and routing actions tend to lag behind the front lines.

The next transmission route is natural gas. UNCTAD’s assessment of the Hormuz disruption notes that the strait is responsible for a large share of the world’s LNG, putting Asian importers at risk through power generation, chemicals and industrial raw materials.

The pressure is already showing up in trade data and industry warnings. A Reuters report on China’s March imports noted a decline in gas arrivals, while ICIS warned that India’s ammonia production faces risks as LNG supply concerns are already impacting the economics of imported feedstock.

That would bring the conflict straight to fertilizer, chemical, and electricity prices. It also impacts manufacturing margins, especially in economies where industrial demand is already softening.

Aviation adds another layer as it is exposed to both route and fuel. The International Air Transport Association cited increased airspace restrictions, airport restrictions and operational uncertainties related to military activities in the region.

Airlines can also reroute routes around conflict zones, but that option burns more fuel, lengthens rotations, tightens aircraft usage and increases overall costs for passenger and cargo networks. At the same time, fuel itself is becoming a constraint.

Europe’s airport sector has warned it could run out of jet fuel within weeks if traffic remains backed up, and Qantas has already cut flights and raised fares as route economics deteriorate.

The latest US producer price data added an important near-term offset to the inflation picture. March PPI rose 0.5% month-on-month, below consensus of 1.1%, while core PPI rose 0.1%, below expectations of 0.5%.

Annual producer inflation was also lower than expected, with headline PPI at 4.0% and core PPI at 3.8%. This alleviates the immediate case of linearly accelerating inflation.

It will do little to remove the structural risks that are building beneath the surface, with transport disruptions, LNG strains, fertilizer exposure and aviation fuel stress that could later put cost pressure on the global economy.

This combination has a wide range of meanings. Air cargo is critical for high-value goods, pharmaceuticals, precision parts, and time-sensitive electronics.

Rising costs and tight schedules are creating friction across supply chains that have only recently regained balance. In the case of the cryptocurrency market, the key points are at the macro level.

A system that spends more on transportation, insurance, and fuel has less room for growth, less room for margins, and less room for policy flexibility. That is the route through which regional conflicts become dependent on global liquidity and risk assets.

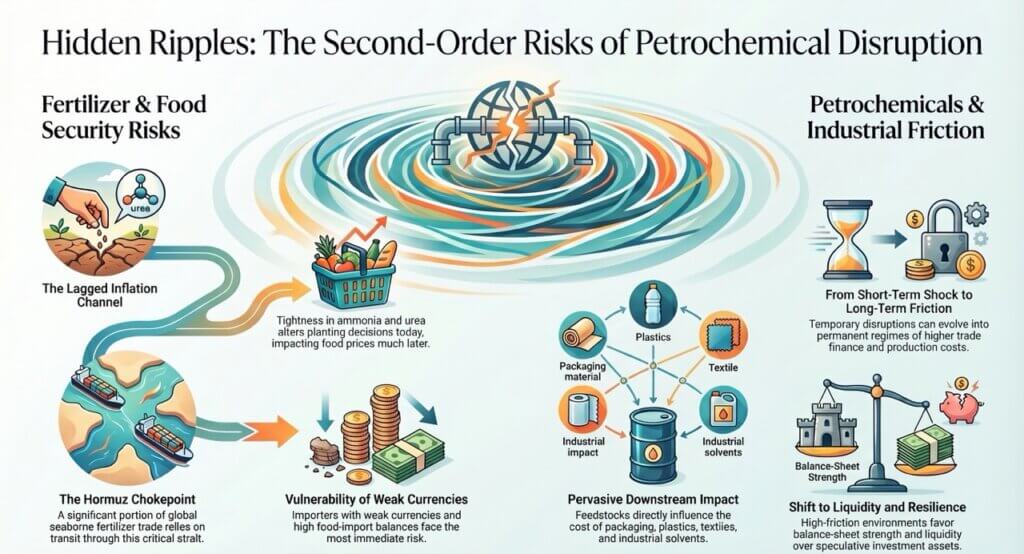

Fertilizers and petrochemicals are emerging as hidden pressure points

Fertilizers and petrochemicals are the most hidden items in the current mess. Although these markets rarely drive the public narrative, they shape food prices, industrial production, and the cost base of a wide range of industrial products.

According to a UNCTAD trade memo, about one-third of the world’s seaborne fertilizer trade transits through Hormuz. This is a large enough share to cause a secondary disruption even if the volume does not collapse completely.

Tightness in ammonia, urea, and related raw materials has a direct impact on agriculture, and cost shocks tend to surface later through planting decisions, input use, and ultimately crop yields.

FAO’s warnings about food security risks have an even sharper impact on this channel. Rising energy costs and disruptions to the fertilizer trade are increasing pressure on food systems far beyond the Gulf.

Countries with weaker currencies and weaker fiscal buffers, especially those where food imports already absorb the bulk of external financing, may be the first to feel the burden. The damage then spills over from commodity markets to household finances, trade balances, and political risks.

Food inflation is long in the memory, and policy responses are often clumsy because the shock starts upstream in gas and fertilizer before it reaches supermarkets.

A similar logic exists for petrochemicals. They exist inside packaging, plastics, solvents, textiles, industrial materials, consumer products, and countless intermediate products.

S&P Global reported that the war is already forcing companies and governments to rethink their supply chain strategies across chemical raw materials. South Korea’s move to ban the storage of petrochemicals is a clear sign of stress.

Governments will not pre-emptively ration actions without recognizing the real risks in physical provision. As naphtha, methanol, ethylene, and related supplies tighten, downstream manufacturers face widespread cost and supply pressures.

It’s both a question of price and quantity.

This conflict is starting to resemble a system shock rather than a single market shock. Oil may suffer a setback on ceasefire news, but fertilizers, chemicals and food will continue to function due to supply delays.

While insurance companies and operators continue to deem the route dangerous, the route may be officially reopened. This delay helps explain why the next stage of disruption feels more diffuse and more persistent than the first.

For cryptocurrencies, these channels are reflected in the macrobalances they create. Prolonged input stress causes inflation to stagnate, growth to slow, and policy space to narrow.

In such circumstances, capital tends to concentrate in search of quality, liquidity and balance sheet resilience. Bitcoin often holds its buzz better than the speculative edges of digital asset markets.

If Holmes remains in custody, chaos moves from shock to regime

The next question is whether the current disruption will stabilize as a significant but temporary shock, or whether it will harden into a regime in which the costs of moving energy, goods, and capital remain structurally high. If Holmes remains in custody, the answer is likely to be on the regime’s side.

The first reason is simple. Shipping and insurance actions may remain defensive long after official access returns.

IMO’s recent statements make clear that piecemeal responses are failing to restore trust. In commercial terms, trust is a commodity that keeps lines functioning.

Without it, the hallway will remain open on paper but half-closed in reality.

The second risk lies in fuel and transportation. Warnings from Europe’s airport sector suggest that aviation fuel could become a more immediate operational constraint if logistics disruptions persist.

That will have ripple effects on travel, tourism and cargo. High-cost supply chains that rely on reliable air cargo will also be hit.

The third risk is agriculture. FAO’s long-term assessment indicates that if fertilizer shortages persist into the planting cycle, there will be a delayed but severe impact on crop economics.

This is the kind of late-onset shock that could cause a reassessment of inflation expectations several months after the initial conflict premium disappears from oil.

The fourth risk lies in emerging markets and trade finance. UNCTAD has warned of tightening financial conditions, weak currencies and rising borrowing costs across the developing world as turmoil spreads.

These dynamics are highly relevant to cryptocurrencies, as they tighten global dollar conditions while increasing domestic fiscal stress in countries where stablecoins, dollar proxies, and cross-border digital payments already play a practical role. There is room for two speeds of cryptographic responses here.

Bitcoin could benefit from a burst of geopolitical mistrust and sovereignty stress. The broader altcoin complex typically struggles when global liquidity is scarce and growth prospects worsen.

That leaves a clear conclusion. The Iran conflict has already gone beyond oil and the initial inflationary impulse.

It is disrupting the operational layers of the global economy: where ships sail, cargo is removed, raw materials are moved, fuel arrives at airports, and industrial inputs are transformed into finished products. If the Strait of Hormuz remains restricted, these disruptions will continue to spread outward through food, cargo, industrial margins, and external funding.

The next critical pressure point for the market could come from lower trading volumes and tighter liquidity, with crude oil being just one of several transmission channels. For cryptocurrencies, this setup favors a more selective environment, where performance is driven more by macro sensitivity, funding conditions, and balance sheet quality than by a reflexive risk-on narrative.

(Tag translation) Bitcoin