HyperLiquid prices surged above $50 as the first Spot HYPE exchange-traded fund drew stronger initial demand than Bitcoin products on a market capitalization-adjusted basis, offering investors a regulated way to express exposure to one of the fastest-growing exchange venues for cryptocurrencies.

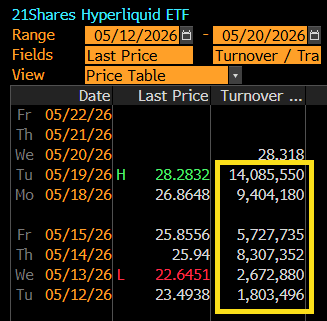

The two HYPE funds attracted nearly $50 million in inflows in their first week of trading and had about $60 million in assets, according to SoSoValue data.

Market capitalization $14.98 billion

24 hour volume $1.35 billion

Best ever $59.39

Although the absolute numbers are still small compared to the largest Bitcoin funds, this launch stands out because the product is expanding from a much smaller token economy.

The move also linked demand for ETFs with a much smaller token economy than Bitcoin, adding momentum to hyperliquid prices.

Bloomberg ETF analyst Eric Balchunas said the HyperLiquid ETF’s trading volume has increased each day since its launch and remains at about eight times its opening day level. He said this pattern suggests natural interest rather than a short-term opening burst.

The demand comes as investors reassess HyperLiquid’s position in the broader digital asset market.

The platform started as a perpetual futures exchange for cryptocurrencies, but has expanded into non-cryptocurrency markets such as commodities, equity-linked products, S&P 500 futures, pre-IPO contracts, and prediction markets.

For ETF buyers, HYPE has become an agent of that expansion. Tokens are being treated not as simple exchange assets, but as exposure to trading platforms that seek to move the rails of cryptocurrencies into markets that have historically existed within traditional finance.

Hyperliquidity price outperforms broader crypto market

Early flows already place HYPE in unusual territory among new crypto fund launches.

The launch of the HyperLiquid ETF is therefore an early test of whether institutional demand can expand beyond Bitcoin, Ethereum and Solana products.

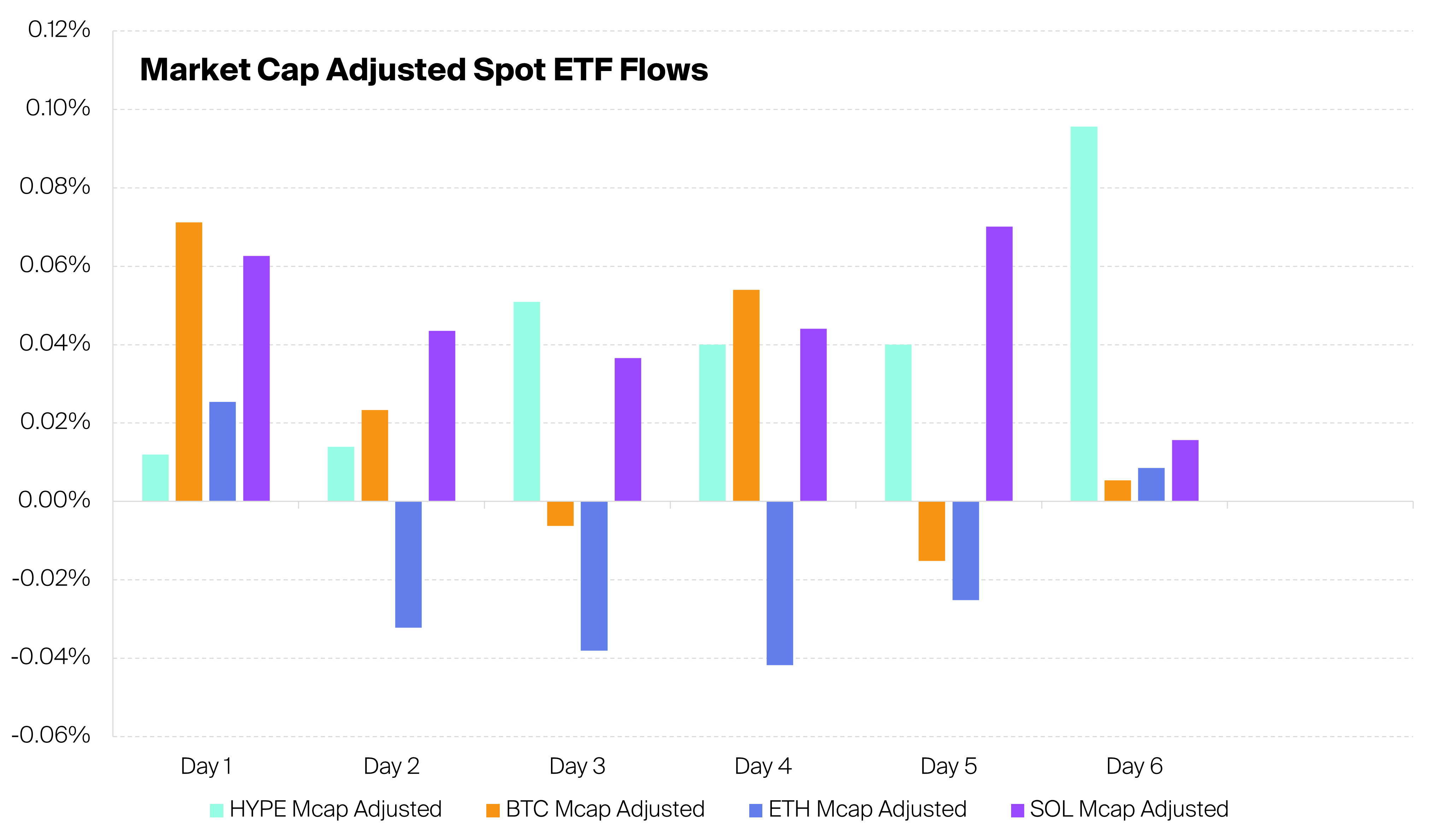

Crypto analyst Aleseia said that after adjusting for market cap inflows, the first two HYPE Spot ETFs outperformed the Bitcoin Spot ETF in three of the first six business days.

This comparison comes amid a downturn for Bitcoin-focused products, which recorded net outflows of over $1 billion during the same reporting period.

Meanwhile, HYPE products outperformed Ethereum funds on five out of six days. Solana’s fund has performed well through four out of six sessions, indicating that early demand for HYPE has been significant, although it hasn’t consistently outperformed all competing crypto ETF categories.

Adjusted flow comparisons narrow the focus from headline dollars to demand for asset size. Bitcoin ETFs still dominate the market on an absolute basis due to their deeper liquidity, access to a wider range of advisors, and longer trading history.

However, compared to Hyperliquid’s token economy, the first week of HYPE ETF activity showed unusually strong demand for the new crypto fund category.

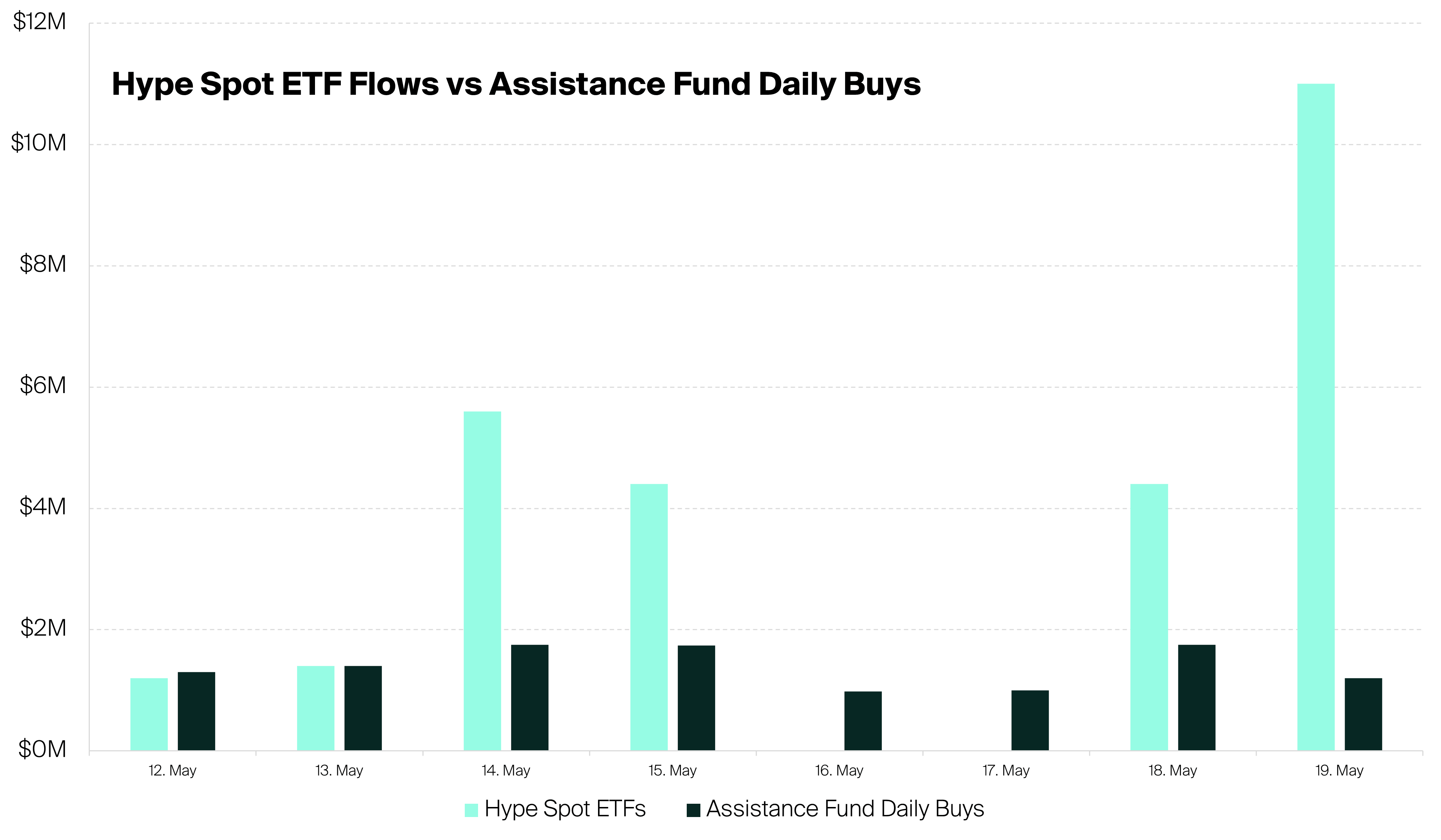

The fund’s activities will also bring about changes in the HYPE market structure. In the first six business days, the ETF purchased 2.5 times the amount of HYPE that HyperLiquid’s support fund purchased and erased, Aleteia said.

This means that the ETF issuer is already creating more open market buying pressure than one of the token’s existing internal support mechanisms.

Support funds buy HYPE and burn it, reducing the supply over time. ETF issuers need to acquire HYPE to support their fund’s exposure, thus creating another demand channel.

The result is a convergence of native protocol demands and traditional market demands, a structure that can only be achieved by a small group of crypto assets through regulated products.

Flows are still in the early stages and may fluctuate as funds move beyond the opening week. Still, the first six sessions moved HYPE to a different part of the market conversation.

Its performance is currently judged not only by crypto-native trading activity on Hyperliquid, but also by ETF inflows, secondary market volume, and institutional investor allocation behavior.

Why did institutional investors follow HyperLiquid?

The demand for the HYPE ETF reflects a broader shift in investors’ valuation of Hyperliquid.

The platform is increasingly seen as a financial infrastructure trade rather than a venue for narrow crypto derivatives trading.

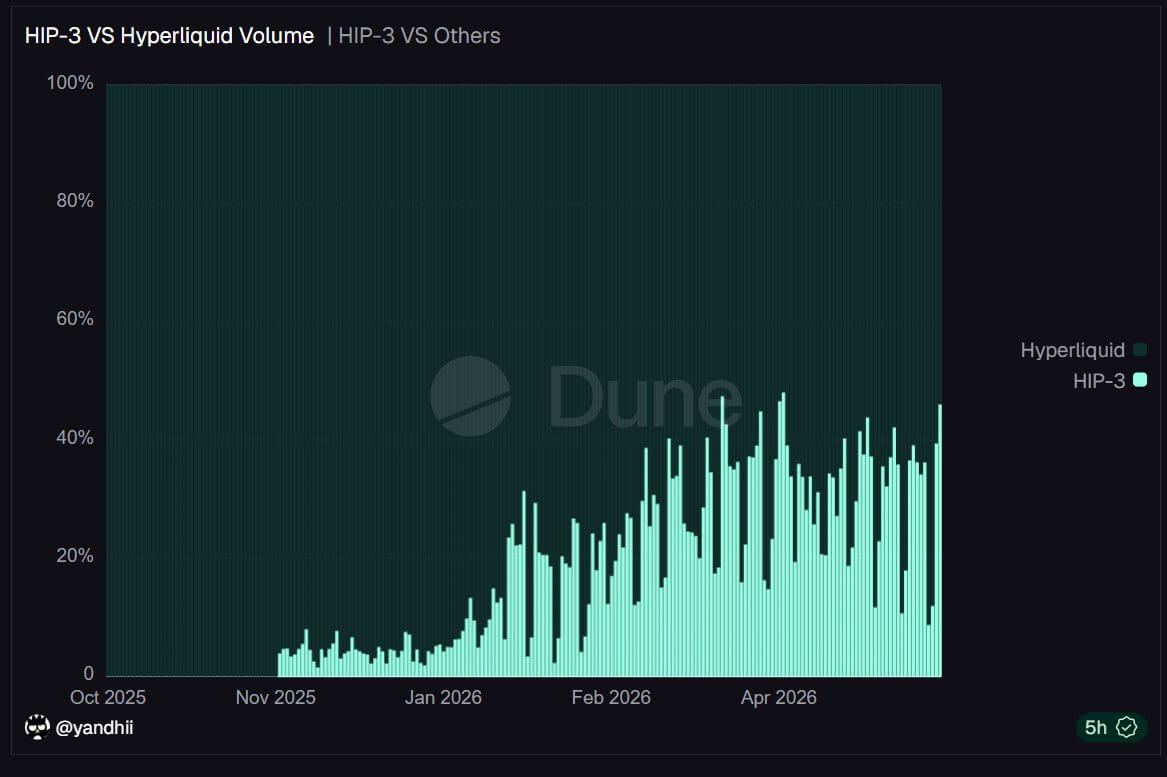

Currently, about half of Hyperliquid’s trading volume comes from non-crypto assets such as stocks, oil, S&P 500 futures, pre-IPO markets, and artificial intelligence companies, according to data from Dune Analytics.

HyperLiquid data also shows that real-world asset trading on the platform reached a record high of $2.6 billion in open interest, roughly double the level from two months ago.

This growth suggests that users are using the platform for broader macro- and equity-related exposure beyond permanent storage of cryptocurrencies.

Hyperliquid also gained attention during the U.S.-Iranian conflict, as its 24/7 market allows traders to avoid geopolitical risks in the Middle East on weekends when standard financial exchanges are closed.

Market participants could trade synthetic versions of traditional assets such as U.S. stocks and commodities, even if traditional venues were offline.

This use case strengthened the institutional argument for the platform.

With this in mind, Bitwise Chief Investment Officer Matt Hogan described HyperLiquid as a new “super app” for cryptocurrencies, claiming that the platform is targeting the $600 trillion global asset market as well as the roughly $3 trillion crypto economy.

He pointed to exposures across cryptocurrencies, equities, commodities, foreign exchange, prediction markets, and structured products as evidence of broader market design.

According to him:

“Hyperliquid has become the ‘super app’ that Mr. Atkins envisioned, a ‘non-SEC-regulated platform’ that provides investors with exposure to ‘a variety of asset classes.’

This framework helps explain why ETF demand has emerged so quickly.

Traditional investors already understand the exchange’s business model, as they can compare trading volume, fee generation, market share, and user growth to publicly traded companies such as CME Group, Robinhood, and other financial platforms.

Hyperliquid offers a crypto-native version of that model with the additional feature that demand for tokens is tied directly to platform activity.

HYPE’s evaluation story becomes clearer due to increase in fees

Meanwhile, market participants point out that HyperLiquid’s fee profile also supports institutional investor interest.

Market observers note that the platform accounts for about a third of the overall revenue of the top 10 protocols and about 43% of all on-chain fees, or about $11 million per week.

Most of its revenue comes from persistent transaction fees. Notably, almost all of it will be used to buy back HYPE on the open market, linking the token directly to platform activity.

This fee stream gives Hyperliquid tokens a more direct economic link to platform activity than many previous governance assets.

Hougan said this structure separates HYPE from many previous DeFi tokens. First generation governance tokens often struggled as the growth of the protocol was not always reflected in the value of the token. Holders were able to vote on governance issues, but often lacked a clear economic link to fees, cash flow, and share buybacks.

According to him, HYPE was launched with a different design. As trading activity increases, so do buybacks. As buybacks increase, investors will have a clearer basis for linking platform growth to token demand.

This allows ETF investors to buy into the story more directly. They are buying exposure to trading platforms, increasing trading volumes, increasing penetration of non-cryptocurrency markets, and powering buyback mechanisms that tie profits back to tokens.

Hougan estimates Hyperliquid’s annual revenue is about $800 million to $1 billion. At a market cap of about $10 billion to $11 billion, HYPE has roughly 10 to 14 times the share repurchase flow.

This comparison is incomplete because token holders do not have the same legal rights as stock holders. Still, it provides investors with a framework to evaluate HYPE against trading platform businesses rather than older DeFi governance assets.

This valuation framework helps explain why ETFs have gained so much demand so quickly. HYPE offers a high-growth exchange theory, a token-linked buyback model, and exposure to a platform that taps into a much larger market than just crypto perpetual trading.

HYPE outperforms broader crypto market

Against this backdrop, HYPE’s market performance has diverged significantly from the broader crypto market.

HYPE has rallied more than 120% this year, hitting an almost eight-month high above $50, according to Tradingview data.

This move puts it ahead of major crypto assets and crypto-related stocks such as Bitcoin, ETH, XRP, Solana, BNB, Dogecoin, and Coinbase, all of which are down double digits since the beginning of the year.

In fact, HYPE’s fully diluted valuation of $54.6 billion overturned Solana’s $54.3 billion.

Blockchain analysis firm Santiment said:

“HYPE’s open interest (which measures the total amount of active futures contracts still open) remains extremely high, currently exceeding $1.92 billion.”

The company further explained that the improved price performance reflects several overlapping catalysts. This includes the recently enacted CLARITY Act, which improves sentiment regarding the US regulatory outlook for digital assets.

At the same time, Coinbase and Circle named Hyperliquid as the official USDC deployer, strengthening the platform’s stablecoin rails. Additionally, the launch of synthetic pre-IPO products has added a new growth story, and the influx of ETFs has given traditional investors new access points.

As a result, HYPE began to trade more like a growth-linked market infrastructure token than a broad crypto beta asset.

Still, the risks to the platform remain high.

Hyperliquid is not available to users in the United States. The company’s new non-crypto products are still in their early stages, and their overall exposure to private companies and real-world markets could lead to greater regulatory scrutiny.

Platforms must also demonstrate that demand is likely to persist beyond launch week ETF activity and volatile trading windows.

(Tag translation) Bitcoin