Welcome to our newsletter “Crypto Long & Short”. this week:

- Ravi Tanuk tells us the story $genius Law to reprice Bitcoin’s monetary premium

- Looped Jesper Johansen $ETH Staking without exposure to the lending market

- “Top Headlines for Educational Institutions to Watch” by Francisco Rodriguez

- “$NEAR Intent fee run rate holds as price recovers from $1 low (This week’s chart)

Thank you for joining us!

-Alexandra Levis

Expert insights

of $genius Bill to reprice Bitcoin’s monetary premium

– Ravi Tanuku, Managing Member and General Partner of Natural Capital and Director of Krakacquisition Corp.

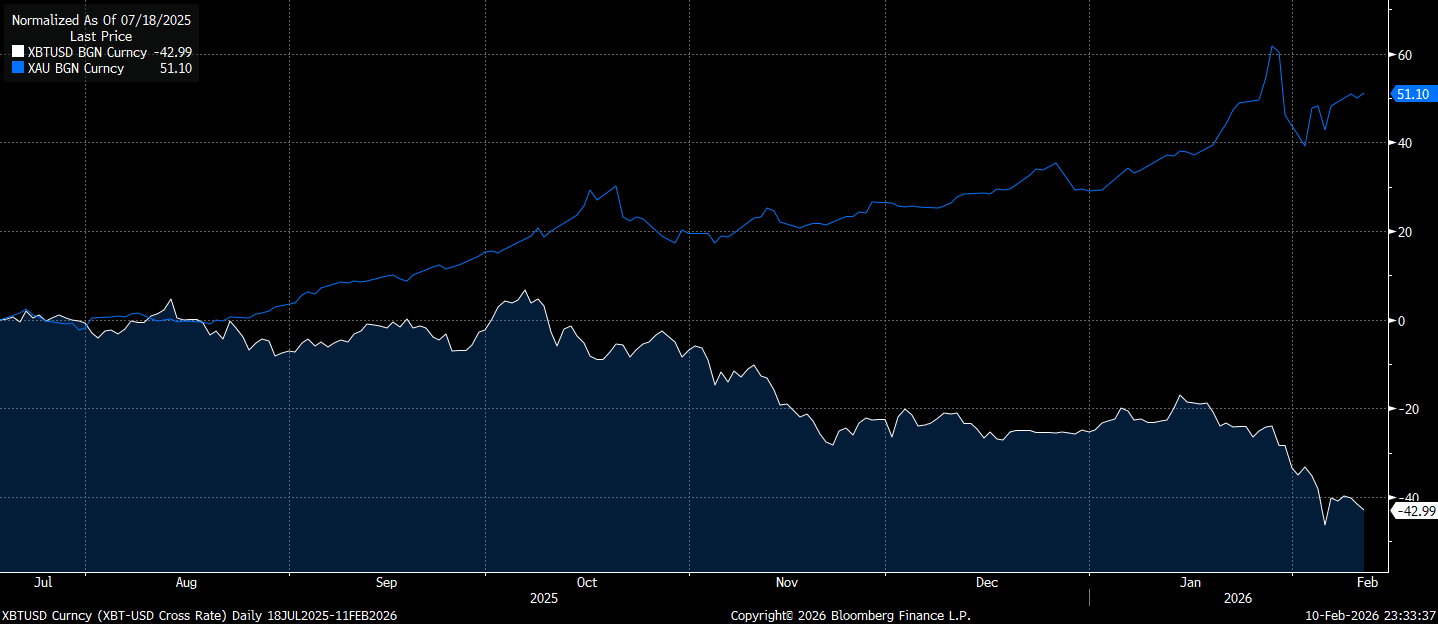

Since July 18, 2025, gold has outperformed Bitcoin by almost 100%. Same macro environment. Quite the opposite result.

The usual explanation doesn’t hold up to the simplest question of why gold still works if this is just a cycle top.

Bitcoin didn’t break due to cycles, sentiment, or quantum risk. This Bitcoin broke because the US government built a better version of what Bitcoin was offering to millions of people around the world and signed it into law that same day. of $genius Regulated stablecoins are 100% backed by US dollars or US Treasuries. In doing so, it created a government-sanctioned alternative currency to Bitcoin, effectively shifting the demand for a “digital dollar” from Bitcoin to stablecoins.

Chart: Bitcoin (XBTUSD) vs. Gold (XAU) normalized performance (BGN). Source: Bloomberg.

What is Bitcoin actually used for?

The standard framework is that Bitcoin has three use cases: access to dollars, digital gold, and speculation. Most discussions focus on the latter two. Recruitment data points elsewhere.

According to Chainalysis, the countries with the highest adoption of cryptocurrencies are Nigeria, Vietnam, Turkey, Argentina, and Ethiopia. The common denominator is not speculation or sound money ideology. These are capital controls and a weak currency against the dollar.

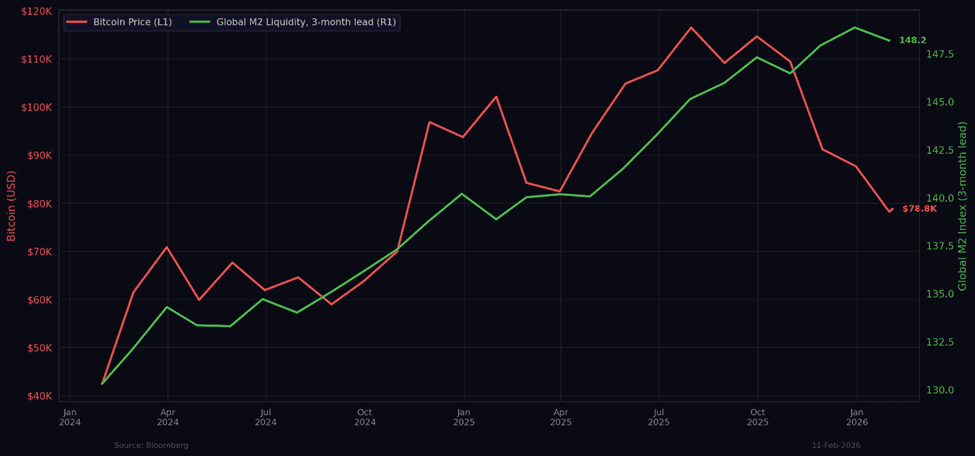

This pattern suggests that Bitcoin’s dominant real-world function has been as an alternative dollar access point for consumers and businesses whose governments have restricted Bitcoin. Speculative flows and institutional investors such as ETFs can be large in dollar terms at any time. But access to dollars was the most stable long-term demand. It was the structured bidding that gave Bitcoin its bottom price and its long-term relationship with the world’s M2 money supply.

Chart: Bitcoin and global M2 money supply. Source: Bloomberg.

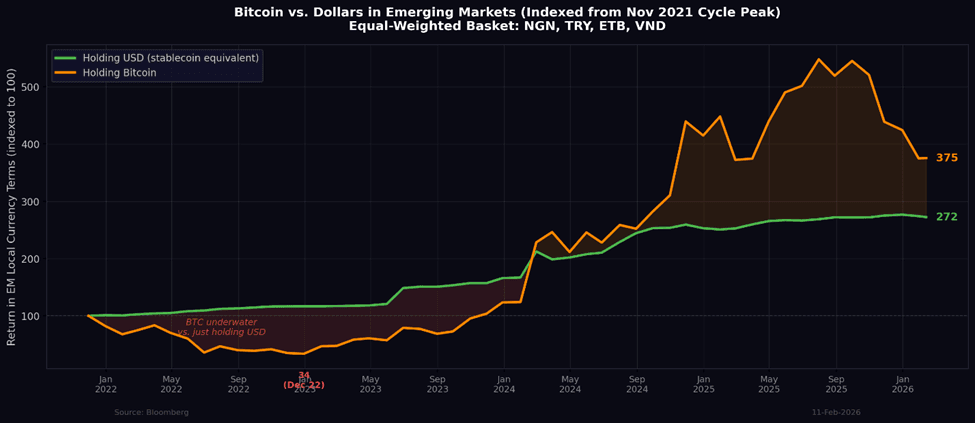

Risk-adjusted data makes this concrete. Since the cycle peak in November 2021, buyers in Nigeria, Turkey, Ethiopia, or Vietnam who held Bitcoin spent 26 of the next 52 months underwater compared to those who simply held US dollars. Both achieved strong absolute returns on a local currency basis. Bitcoin returned 275% and the dollar returned 172%. However, Bitcoin’s annual volatility was 68% compared to 18% for the dollar, and its Sharpe ratio was around 0.5, compared to 1.5 when holding only dollars. Bitcoin’s maximum drawdown was 66%. Dollar holders accounted for 6%.

Chart: Bitcoin vs. Dollar in Emerging Markets, indexed from November 2021 cycle peak. Source: Bloomberg.

These buyers were not making speculative bets on digital gold. They were trying to hold onto the dollar. Bitcoin was the best wrapper available, but the returns specifically occurred on dollar exposure, not Bitcoin. Regulated stablecoins capture the same currency decline tailwinds without the drawdowns.

The transition was already underway $genius Activities. According to Artemis, B2B stablecoin payments have soared 30x to over $3 billion per month by early 2025, driven primarily by cross-border payments. This law accelerated changes that were already visible.

what happened after that

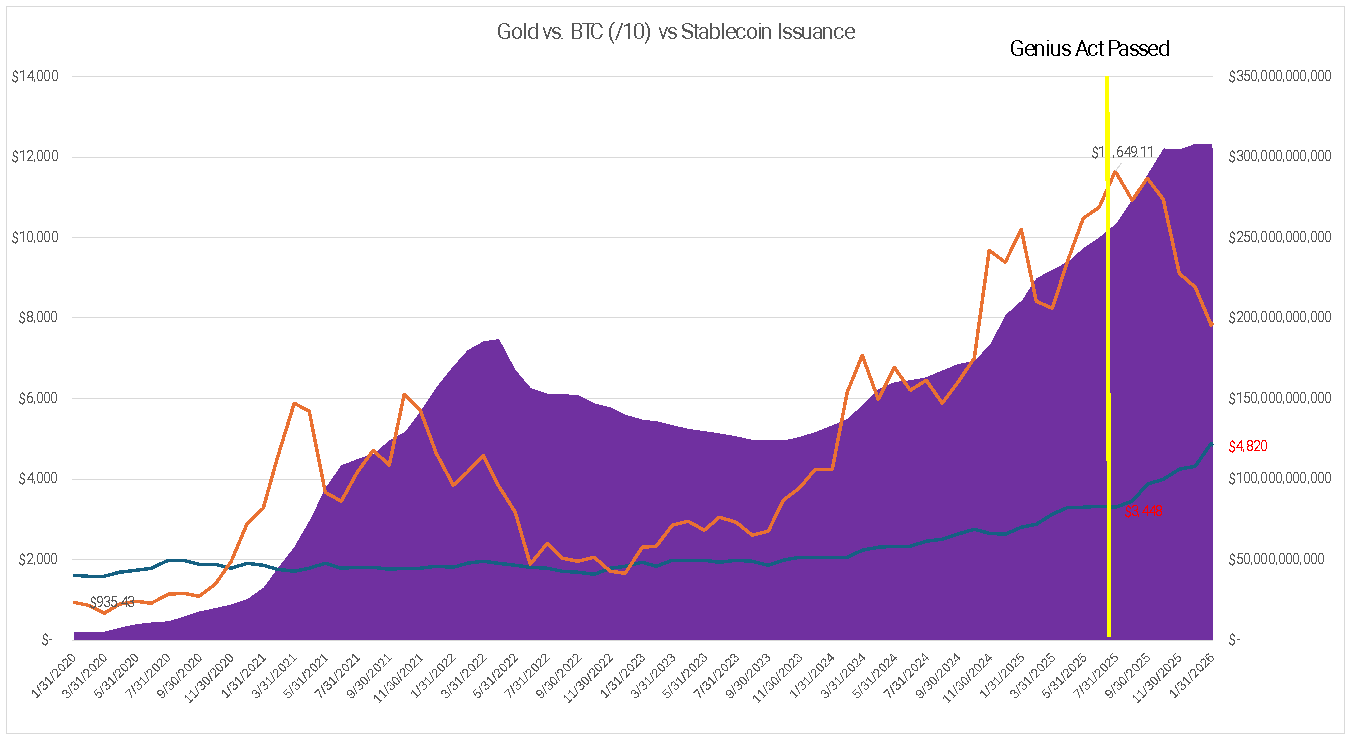

The market capitalization of stablecoins increased by 45% to over $306 billion in October, up from approximately $211 billion in January 2025. Monthly issuance amount doubles from last year’s approximately $6.6 billion$genius That rose to more than $13 billion in the three months after the bill took effect. Bitcoin fell 43%. Capital did not leave cryptocurrencies. You just don’t need Bitcoin to get to your destination.

Chart: Gold vs Bitcoin (scale) vs stablecoin supply (market cap), $genius The passing points of the act are marked. Source: Bloomberg author chart data.

Macro then clearly tested the digital gold theory. In the second half of 2025, a cyclical reacceleration occurred throughout the real economy. The product rebounded. Gold, silver, and copper have reached new highs until January 2026. Bitcoin was sold off along with SAAS stocks and unprofitable tech. By the fourth quarter of 2025, the quarterly correlation with IGV reached +0.64, the tightest since the 2022 bear market.

This cycle, the market did not treat Bitcoin as a financial hedge.

Upcoming tests

The CLARITY Act aims to regulate Bitcoin as a commodity. That classification can be important. Bitcoin is currently in regulatory limbo, making it difficult for institutional investors to include it in their commodity portfolios alongside gold and silver. Formal product status changes the compliance debate, creates index inclusion logic and gives pension funds and endowments an allocation framework.

of $genius This legislation could permanently damage the use case for access to dollars. CLARITY could revive the digital gold doctrine under a new regulatory identity.

The test is not whether Bitcoin will rise after CLARITY. Oversold assets can bounce off the catalyst. The test is a correlation regime. Will Bitcoin start recombining with gold within a quarter or two of the passage of CLARITY? Or will you continue trading for long-term growth?

There’s an irony here. The cryptocurrency industry spent years lobbying for regulatory clarity. The first major regulation officially created a competitor that made Bitcoin’s core functionality obsolete. It is an open question whether the second major regulation will give it a new structural identity or confirm that the old one is gone.

Focus on what Bitcoin trades with, not where it trades. The correlation regime is the signal.

principled perspective

looped $ETH Staking without lending market exposure

– Jesper Johansen, North Stake CEO and Founder

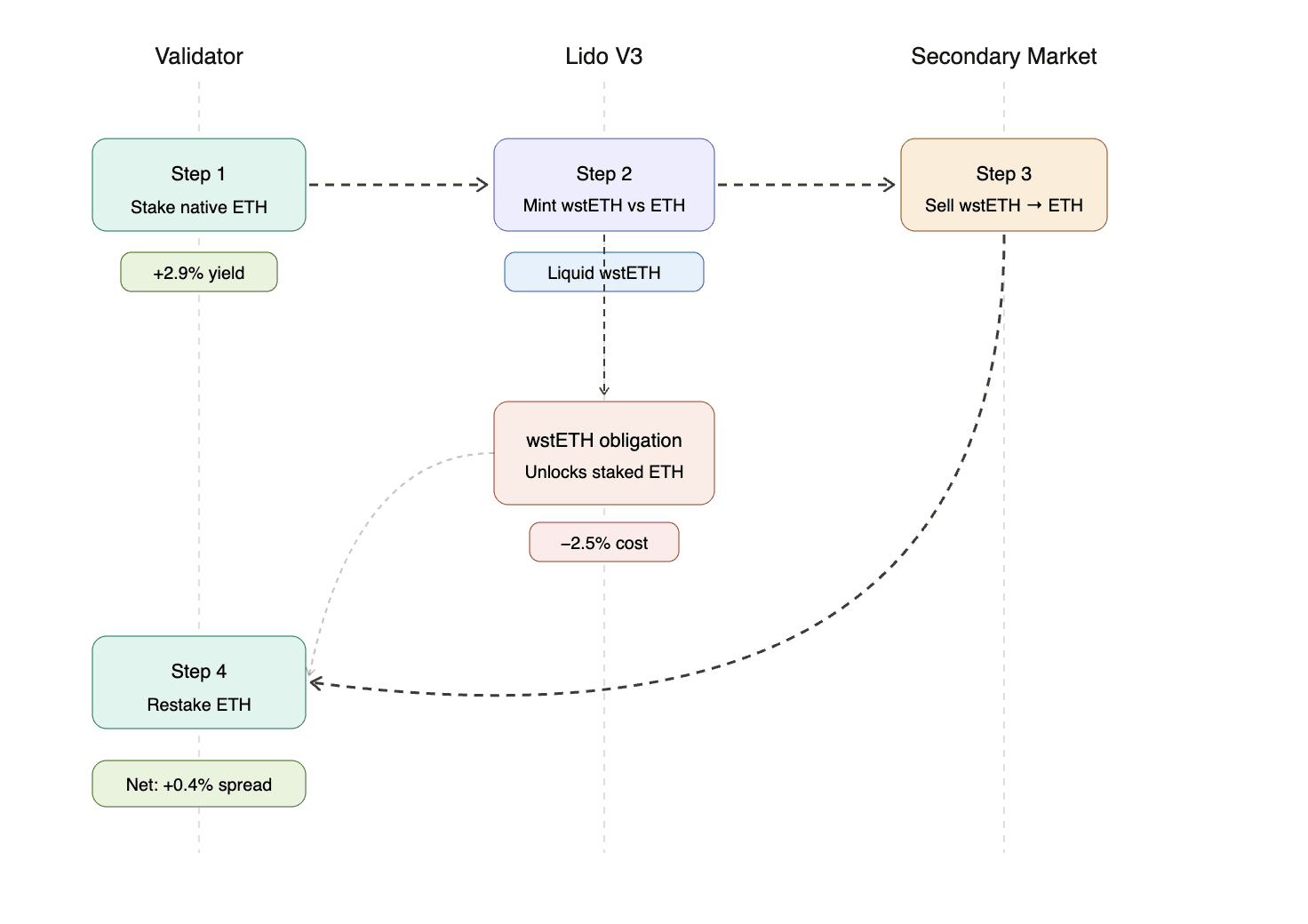

The most utilized staking strategy on Ethereum follows the same strategy: Deposit $ETHreceive a liquid staking token and repeatedly borrow against it in a lending protocol. It works – until it stops working. Liquidation risk, variable borrowing rates, and smart contract exposure across multiple protocols make this approach vulnerable at institutional scale.

There’s an easier way. One that allows you to earn comparable yields without touching any lending protocols.

rates and spreads

The current yield for native Ethereum validator staking is approximately 2.9% APY. Lido’s stETH (the largest liquidity staking token) yields around 2.4%. This gap exists because Lido offers rewards to all stETH holders, including: $ETH It sits idle in the entry and exit queues and doesn’t yield anything. The more activity a queue has, the wider the spread.

This interest rate differential fluctuates, but has recently reached 50 basis points. Interest rate differentials are the basis of this strategy.

structure

The strategy implementation leverages the Lido V3 staking vault and Northstake’s staking vault manager to capture and loop on rate differences. Vault operator’s stake $ETH Available natively on Ethereum validators, you can earn up to 2.9% APY in full. You then mint stETH against your staked position through Lido’s native minting mechanism within stVault, rather than borrowing. Minted stETH is exchanged for staked $ETHThis can be integrated back into the vault validator via the EIP-7251 integration. Each loop adds exposure. Minted stETH can also be exchanged for liquid $ETH However, since it is staked in stVault, it is eligible for the entry queue.

With 10 loops, this strategy achieves approximately 6.6% APY. This is approximately twice the base staking rate. A liquidity buffer of 6.94% is maintained in reserve. A full position can be unwound as quickly as the validator exit queue, which currently stands at about 8 days, or by returning stETH to the vault to reduce vault liability. $ETH Unstaking.

Importantly, no lending protocols are involved. This leverage is structural and is created entirely by leveraging the stETH rate differential within Lido’s vault architecture. There are no clearing standards, variable borrowing costs, and no counterparty dependence on the lending market.

Example: using wstETH (non-rebased version of stETH) and assuming secondary market rather than consolidation.

The risk is real but known

Continuing risk is the primary consideration. Initial seed capital must go through the validator entry queue, which currently takes approximately 56 days. Subsequent scaling uses validator integration instead of queues, but full deployment takes 60-76 days depending on the integration cycle.

Spreads can be harmed by validator performance degradation or slash events. Once the rate difference is compressed, additional loops can be added. If it spreads uncomfortably, you can reduce the position by partially unstaking.

Importantly, you can exchange 1 stETH for 1 stETH at any time. $ETH With Lido. Due to the way Lido’s stVaults manage vault responsibility, depegging stETH does not result in negative carry. In the worst case scenario, if the stVault debt becomes unhealthy, Lido will perform a forced rebalance of the stVault. $ETH The stakes are released and the liability reduced.

Adding downside protection using CESR

One notable new development is that staking risk insurance products now exist that can guarantee a minimum yield benchmarked to the Composite Ether Staking Rate (CESR), which represents the average annualized yield of validators. Under these policies, if a validator underperforms compared to CESR due to thrashing, technical failures, or operational errors, the insurance company will cover the shortfall. For institutional allocators who require predictability in yield, this transforms the strategy’s variable return profile into something closer to a fixed income product: a leveraged staking yield with a guaranteed floor.

Who is this for?

Institutional capital is moving towards staking structurally rather than speculatively. They are looking for strategies that allow them to achieve higher yields without introducing exposure to lending markets or adding complexity. For asset managers, this strategy also helps strengthen liquidity management of staking assets. $ETH ETF.

The spread is there. The infrastructure and tools exist to capture it.

this week’s headlines

– Written by Francisco Rodriguez

Just as the SEC pushed ahead with the introduction of tokenized stocks on DeFi and the liquidation of Nasdaq’s cash-settled Bitcoin options last week, Promethium staked its claim on broker-dealer distribution of on-chain securities, and HyperLiquid made further inroads into the same product line, institutional crypto continued to fill in at the last minute as prediction markets faced a House Oversight insider trading investigation.

- SEC to propose framework for tokenized stocks as Wall Street grapples: Planned innovation exemption would allow third parties to issue tokenized public stocks for DeFi transactions without issuer approval. The move extends the March approval of Nasdaq’s tokenized securities framework.

- Bitcoin options are coming to Nasdaq. What this means for you: The SEC has conditionally approved Nasdaq PHLX to track the CME CF Bitcoin Real-Time Index and list a cash-settled European-style Bitcoin index option under QBTC.

- FalconX says Hyperliquid is emerging as a challenger to traditional exchanges and prediction markets, with HIP-3 Markets drawing pre-IPO bets on Cerebras, Anthropic, and SpaceX onto the platform, and HIP-4 performance contracts and HYPE targeting Polymarket and Calsi up 94% in three months.

- Congress Hits Polymarket and Calci in Massive Insider Trading Investigation: After Bubble Map posted a 98% win rate on 80 polymarket bets related to U.S. military operations, House Oversight Chairman James Comer sent a letter to Shayne Coplan and Tarek Mansour by June 5 requesting records related to background checks, geographic restrictions, and abnormal trade detection.

- Promethium believes that distribution on Wall Street is the missing link for tokenized securities. The SEC-registered company has launched an infrastructure that enables broker-dealers and RIAs to offer tokenized securities and crypto assets through traditional brokerage accounts, covering issuance, trading, custody, clearing, and settlement.

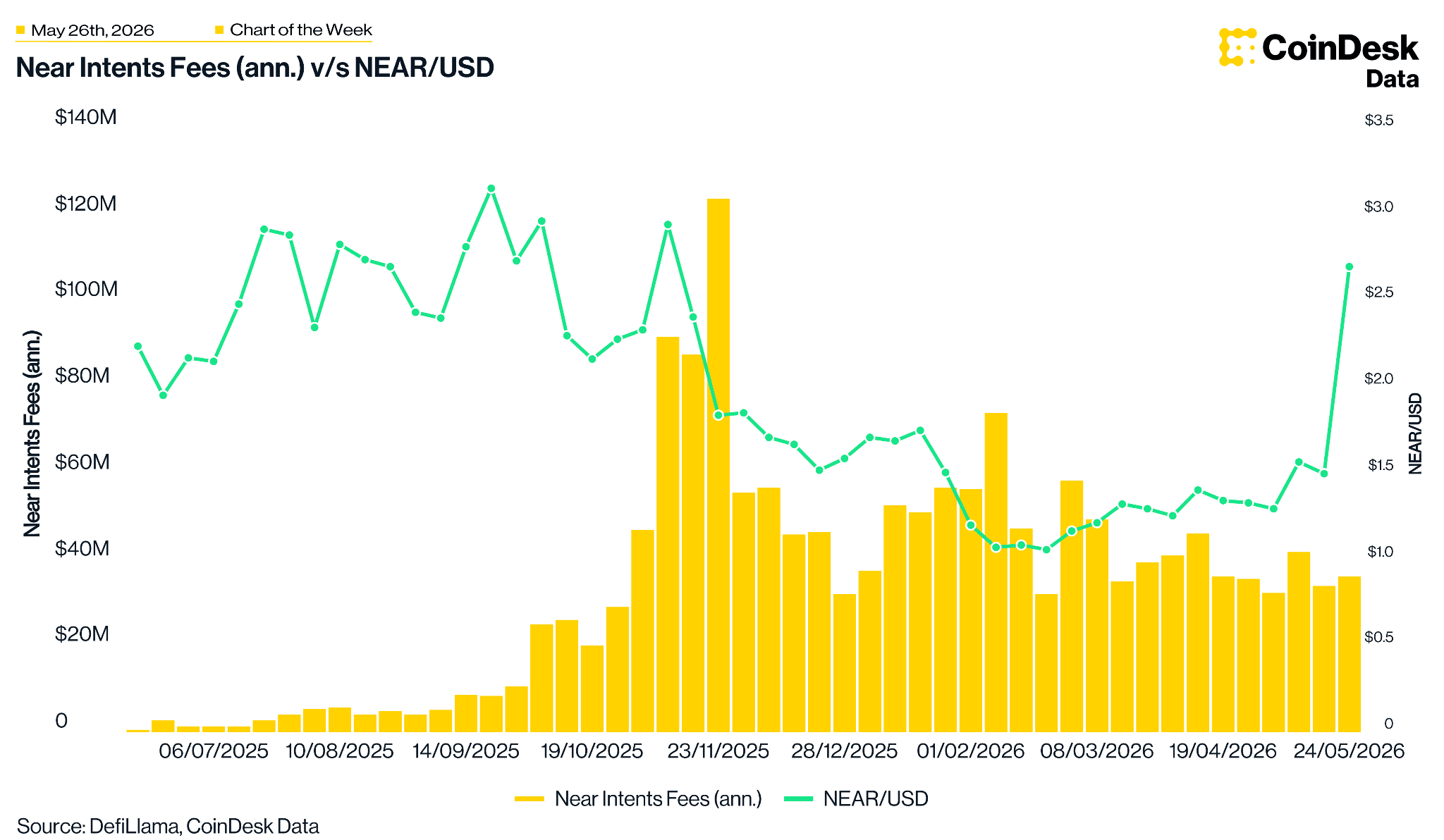

This week’s chart

$NEAR Intent’s fee run rate remains around $36 million annually as price recovers from lows of $1

Weekly rates available $NEAR As of the week ending May 24, Intent was at an annualized value of $36 million, having ranged between $32 million and $58 million since late February after peaking at $124 million in mid-November. $NEAR It fell from $3.16 in late September to a low of $1.06 in late February, but recovered to $2.7 earlier this week.

listen. read. clock. engage.

- listen: Did you hear that? CoinDesk newsletters (Crypto Long & Short and Crypto for Advisors) have been shortlisted for The Publisher Newsletter Awards 2026. Congratulations to all the candidates.

- read: In “Crypto for Advisors,” Morgan Stanley Investment Management’s Sarah Cummings provides insights and considerations when evaluating crypto ETFs.

- clock: “Morgan Stanley’s ETF boom, Grayscale’s staking push, and BitGo’s IPO: Wall Street’s crypto race is on.”

- engage: David LaValle, President of CoinDesk Data & Indices, will moderate a panel discussion at SPI’s Solana Summit in Chicago on Tuesday, June 16th.

Looking for more? Receive the latest cryptocurrency news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect the views of CoinDesk, Inc., CoinDesk Indices, or their owners and affiliates.