Bitcoin was already capped below the dense on-chain supply zone by the Fed’s decision yesterday, and Fed Chairman Jerome Powell’s press conference gave buyers little reason to push past it.

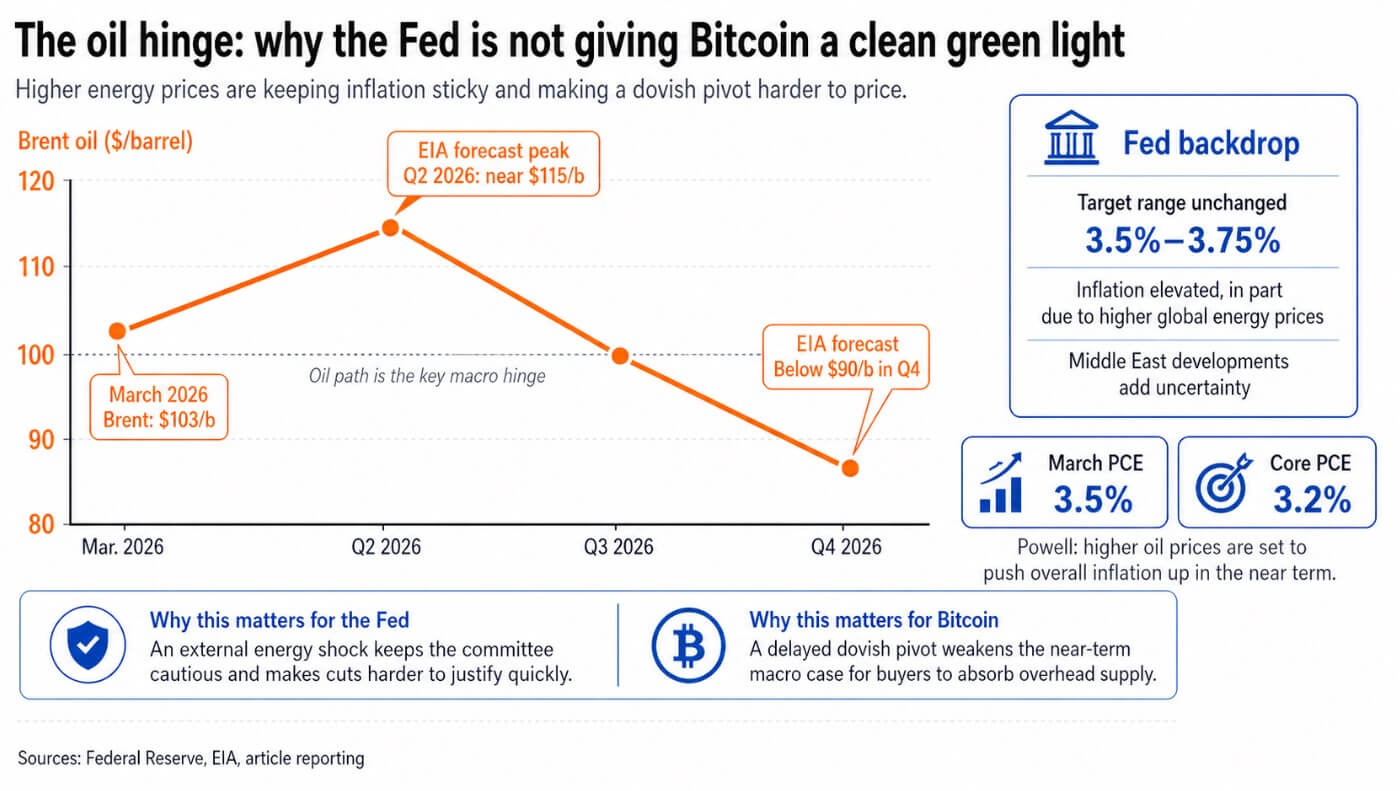

The Fed left its target range unchanged at 3.5% to 3.75%, citing tensions in the Middle East as a source of uncertainty in the economic outlook, and explicitly linked rising inflation to rising global energy prices.

In his opening remarks, Chairman Powell added to this framework by predicting that total PCE through March would remain at 3.5%, core PCE at 3.2%, and that rising oil prices would push up overall inflation in the short term.

The committee was also divided on the most divisive Fed vote since 1992. Eight officials supported the move, and one opponent wanted the rate cut, while Hammack, Kashkari and Logan opposed leaving any easing bias in the statement.

Internal divisions exposed the commission’s actual stance on mitigating bias, leaving that language in the text, while three officials argued the language was already too permissive.

The result for Bitcoin is a macro environment that makes it difficult to price in a dovish pivot, even though the March Economic Forecast Summary still shows the median federal funds rate at 3.4% in 2026, suggesting one rate cut this year.

Futures markets say there is little chance of a rate cut before the end of the year, and some traders say a rate hike is unlikely in the next 12 months.

oil hinge

The Fed’s inflation problems stem from external energy shocks, which Powell said are out of the central bank’s control.

Brent crude averaged $103 per barrel in March, and EIA expects it to peak near $115 in the second quarter and fall below $90 in the fourth quarter.

As energy pushes up PCE, both headline and core inflation are rising through separate channels, while tariff effects continue to work through core goods prices.

This two-channel setup prevents the Fed from considering oil shocks quickly, as the committee must first ensure that rising energy costs have not affected inflation expectations before justifying a rate cut.

By Powell’s own account, near-term inflation expectations are already rising. Bitcoin currently sits below the oversupply zone, and the macro case for absorbing that supply has the least short-term traction.

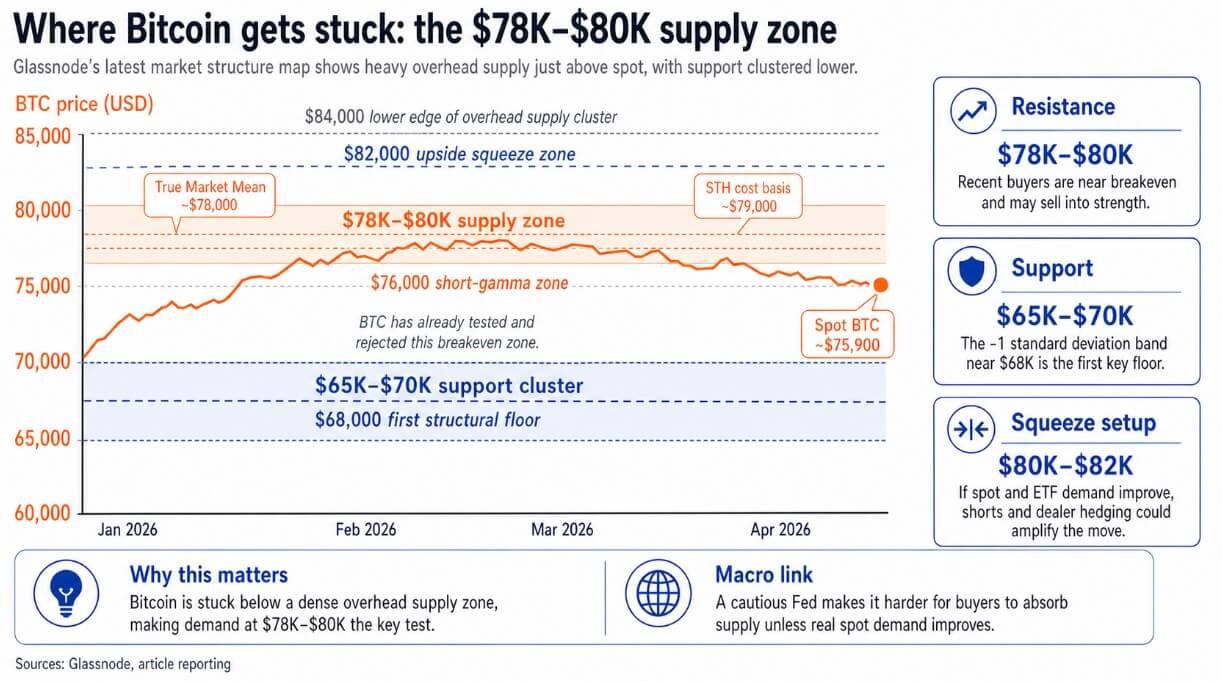

Where Bitcoin gets stuck

Glassnode’s latest report states that Bitcoin’s main resistance levels are near the true market average of $78,000 and the cost basis for short-term holders near $79,000.

Both levels converge to the supply zone between $78,000 and $80,000 that BTC has already tested and rejected. The pattern Glassnode describes is a classic bear market rally structure. Prices have risen to the break-even point for recent buyers, those holders have spread out, and incoming demand cannot absorb supply at that level.

Spot BTC trading around $75,900 has fallen below its resistance band and is approaching $76,000, which Glassnode flags as a downside short gamma zone.

At that level, the dealer’s hedge flow is structurally biased, amplifying price movements in either direction, selling if it falls further or buying if it rises, turning $76,000 into a volatility trigger.

Major support lies between $65,000 and $70,000, with the -1 standard deviation band around $68,000 providing the first meaningful structural lower bound.

We believe that the $68,000 test will test short-term market structure, and that a drop below this threshold will accelerate distributions and weaken broader fundamentals.

2 results

In the bullish case, oil prices will decline in line with EIA benchmarks through the second half of 2026, headline inflation will subside, and the Fed’s implicit interest rate cuts will once again gain credibility.

If this repricing begins and BTC clears $80,000, Glassnode says the $82,000 short gamma zone could force dealers to make strong purchases and amplify the move.

Perpetual futures positioning has already reversed to record negative levels, providing significant fuel for the squeeze. If spot and ETF flows confirm the move and there is a sustained break above $80,000, the market will gravitate towards the lower band of the glass node overhead supply cluster around $84,000.

In the bearish case, oil prices continue to rise to the EIA’s second-quarter peak, and headline inflation remains sticky enough to push rate cuts into late 2027.

Bitcoin continues to fail on a true market average and short-term holder cost basis, with the market retreating towards the $65,000 to $70,000 support cluster.

The $68,000 band then becomes a waypoint. If ETF flows do not stabilize and spot demand remains thin, the structure below $68,000 will deteriorate, paving the way for the deeper accumulation zone where the current bull market began.

| element | bull case | bear case |

|---|---|---|

| oil path | Brent follows lower EIA basepath after Q2 peak | Brent continues to rise through Q2 peak and stays sticky longer |

| inflation path | Headline inflation slows as energy pressures ease | Headline inflation remains stable as energy continues to push prices up |

| Fed outlook | The Fed’s implicit interest rate cuts become more reliable once again. | Interest rate cuts will expand further as Fed restraint continues |

| Powell / Macrotone | Inflation concerns begin to plateau | Inflation uncertainty continues to dominate |

| BTC 78,000-80,000 dollars | Bitcoin regains and maintains resistance band | Bitcoin continues to reject true market average and short-term holder cost basis |

| Positioning / Gamma effect | If it exceeds $80,000, it will enter the short gamma zone of $82,000, which may trigger buying by dealers. | Hedge flows amplify downside volatility, causing price to lock in or fall near $76,000 |

| ETF/spot demand | Spot and ETF flows improve enough to absorb overhead supply | ETF flows are unstable and spot demand remains too low |

| Next rising/falling level | Market likely to expand towards lower end of overhead supply cluster near $84,000 | The market is moving back toward the $65,000 to $70,000 support cluster |

| major structural levels | $80,000 triggers a breakout | $68,000 is key floor under pressure |

| remove | Oil softens, Fed problems ease, Bitcoin has room to rise | Oil prices are still trending higher, the Fed remains in the box, and Bitcoin remains vulnerable to further declines |

Between these two outcomes, the oil path is the deciding variable.

Powell said the committee cannot adjust for external energy shocks the way it manages domestic demand cycles, so Bitcoin bulls need oil’s cooperation at least as much as Powell’s softening tone.

Glassnode’s positioning data adds asymmetry to the cautious picture, as perpetual stocks are at record net short levels, suggesting the market has already priced in significant pain.

Even a plateau in the inflation story, with oil prices stalling below their Q2 peak, or even a single drop in PCE print could be enough to trigger a sharp rally from that position.

Glassnode also notes that spot selling has eased and ETF assets under management are starting to stabilize, both early signs that distribution at current levels is losing momentum.

Both the breakout and retest scenarios depend on whether real demand reaches the $78,000-$80,000 zone before macro uncertainties force further declines.

(Tag translation) Bitcoin