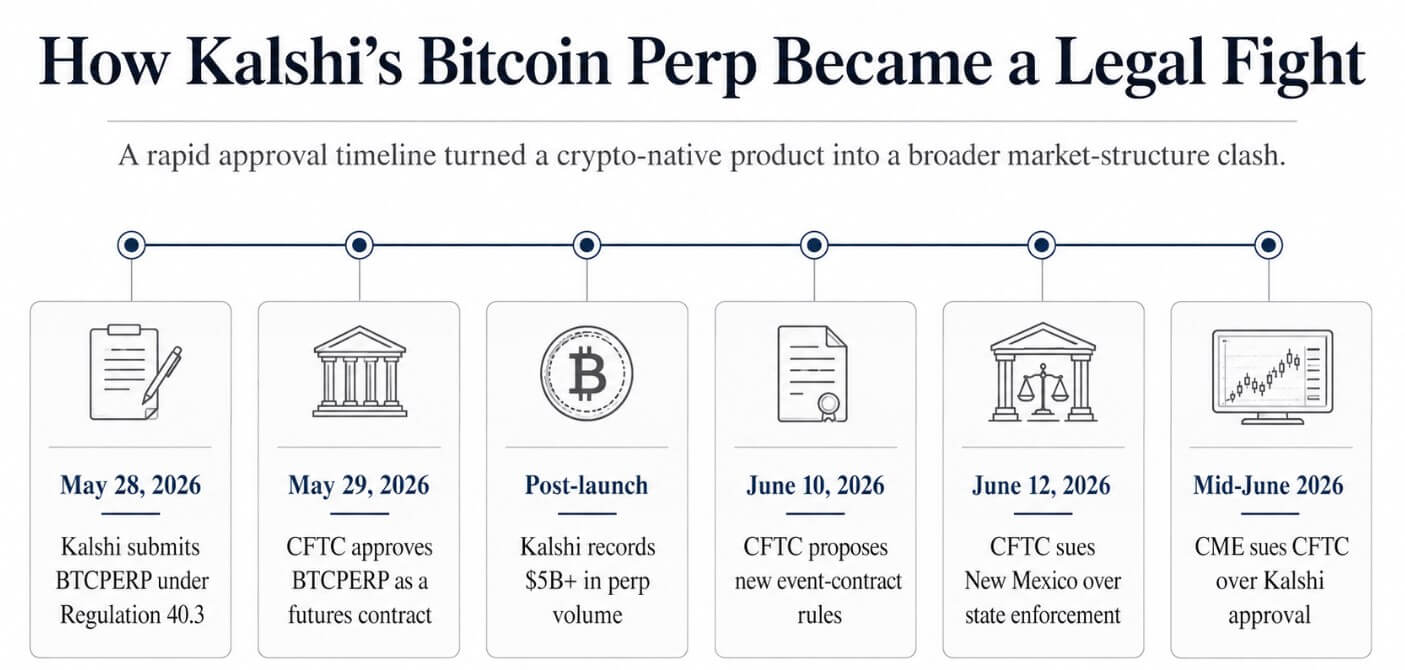

The CFTC approved KalshiEX’s BTCPERP contract on May 29, the day after Kalshi filed it under Rule 40.3.

The contract refers to spot Bitcoin, has no expiration date, and PERP typically allows leverage of up to 50:1 and allows automatic liquidation to eliminate positions in the event of sharp movements.

CME CEO Terry Duffy announced that the company will sue the CFTC, alleging that the regulator misclassified its products. As reported by the Wall Street Journal, CME’s complaint says Kalsi’s crime should have been classified as a swap and would have been subject to stricter Dodd-Frank rules.

Calci has already recorded more than $5 billion in PERP trading volume since its inception, and the stock prices of CME, Cboe, and ICE have fallen following the approval, as investors read the CFTC’s decision as a long-term competitive threat to incumbent exchanges.

This market reaction makes it clear why CME’s opposition is based not only on consumer protection but also on competition logic. Kalshi started as a platform where users traded event contracts such as Fed rate cut odds and election winners.

The addition of regulated Bitcoin criminals draws Kalsi to the same retail derivatives trading screen that CME has spent decades building. This lawsuit is CME’s attempt to use the courts to slow its expansion before it is structured.

wider repulsion

The Futures Industry Association (FIA) and its Principal Traders Group told the CFTC that perpetual derivatives raise questions about trading and clearing risks and called on the CFTC to establish clearer definitions and a formal rulemaking process before approving more such products.

A bipartisan coalition of 41 attorneys general told the CFTC that platforms like Calci and Polymarket operate as unregulated sportsbooks and that sports-related event contracts should remain under state authority.

The CFTC’s predictive market comment document includes the United States Gaming Association, the state gaming commissions of Arizona, Illinois, Maryland, and Michigan, the Indian Gaming Association, Major League Baseball, and the NBA.

| actor | target | core objection | bigger problem |

|---|---|---|---|

| CME | Karshi BTCPERP | Should be treated as a swap, not a futures contract | Protecting futures market boundaries |

| FIA / FIA PTG | perpetual derivatives | New trading and liquidation risks | Clearer CFTC process needed |

| 41 Attorney General | sports event contract | State gaming authorities must apply | Federal and state control |

| game group/tribe | prediction market | Event contracts are similar to sports betting | The boundaries of gambling law |

| MLB/NBA | sports contract | Integrity and Betting Market Concerns | Commercialization of sports risk |

| C.F.T.C. | National enforcement action | Federal DCM authorities should pre-empt states. | Who regulates the event market? |

The CFTC proposed new event contract rules on June 10, with a comment deadline of July 27, and on June 12 sued New Mexico to block state gaming enforcement on the CFTC registered contract market, citing similar disputes in Arizona, Connecticut, Illinois, New York, Minnesota, Rhode Island, and Wisconsin.

The CME’s derivatives classification debate, the attorney general’s defense of state gaming authorities, the FIA’s process objections, and the gaming industry’s sportsbook framework each have the same expansion goal, but come from different institutional interests.

The platform bundles tradable markets across categories that incumbents and regulators have kept separate for decades.

Convergence is already happening

Kalsi and Coinbase have brought regulated cryptocurrency criminals into the country, making it the first time such products have been made available to U.S. investors through a domestic regulated exchange.

Polymarket’s website directly promotes PERP and includes early access invitations.

HyperLiquid, which built a user base on crypto perpetual futures, added markets for the results of off-chain events such as US inflation data and Federal Reserve Board decisions via HIP-4, allowing users to trade forecast-style contracts alongside crypto derivatives in one account.

Each platform independently executed the same underlying product logic. This is because PERP generates continuous leverage-driven volume, event contracts generate media-driven attention spikes, and the platform hosting both captures both revenue streams.

From May 17 to June 10, SpaceX’s pre-IPO PERP generated approximately $3.2 billion in volume and $390 million in open interest across eight exchanges, with Binance accounting for $2.1 billion.

Even though these are synthetic products with no direct claim on the underlying stock, demand for tradable exposure to private company valuations generated $3.2 billion in trading volume in less than a month.

The list of assets that cannot be used as an underlying asset is getting shorter.

Two possible outcomes

If the courts reject CME’s swap classification argument, the CFTC’s regulatory boundaries remain in place, federal preemption encompasses state gaming enforcement, and platforms continue to add asset-to-asset markets, the exchange-for-all model will accelerate.

Bitcoin becomes the gateway collateral and risk asset for a wider range of retail derivative products. Mr. Kalsi’s initial trading volume was $5 billion, the Journal reported, and if he continues at this pace, the land-based criminals alone will be worth nearly $90 billion a year.

Prediction markets add depth to derivatives, derivatives platforms add involvement in event markets, and the boundaries between futures exchanges, sportsbooks, and crypto trading apps collapse into UX distinctions.

| scenario | what happens | Market impact |

|---|---|---|

| CFTC boundary hold | The court rejects CME’s argument. Preemptive action by the federal government limits state gaming enforcement. Platform continues to add cross-asset markets | Calci type land observer scale. The initial $5 billion in trading volume could grow to nearly $90 billion annually if maintained. |

| Existing companies are slow to grow | Injunction, remand, swap classification, or narrower event contract rules | Offshore venues continue to dominate the $61.7 trillion global PERP market. U.S. regulated criminals still have less than $154 billion in annual notional value |

| core question | Can one platform legally host BTC, inflation, elections, sports, and private company exposure? | Winning platforms are those that survive the regulatory boundary battle. |

If incumbents succeed in slowing expansion through injunctions, remands that force Karsi parties to classify their swaps, or a narrower event contract framework from the CFTC, platforms will absorb higher compliance costs, increased geofencing, and product cycle delays.

Offshore venues continue to dominate global PERP transaction value, reaching $61.7 trillion in 2025, a 29% year-on-year increase, while US onshore regulated PERP remains at less than $154 billion in annual notional value.

Users are already trading BTC, inflation, elections, and sports results. Platforms that absorb the current regulatory frictions will be those that are in a position to host whatever compliance frameworks survive.

CME’s lawsuit confirmed that this battle was already underway, with incumbents from the futures industry, gaming industry, and state government deciding to fight simultaneously.

(Tag Translation) Bitcoin