Bitcoin’s $10 billion-plus corporate credit market continues to attract new entrants after a sharp selloff in June led to margin calls that sent major preferred stocks well below par.

A new report from BitcoinTreasuries.net describes the economic downturn as the sector’s first meaningful stress test, providing an early indicator of whether companies can reliably build their funding structures around crypto reserves.

This decline showed how quickly a supposedly stable product can crumble when too much leverage is built up. Still, the market appeared to be functioning, albeit bruised. Dividend payments continued, secondary market trading volumes reached record levels, and corporate treasuries continued to add Bitcoin to their balance sheets.

This resiliency has won praise from industry advocates and continued interest from prospective issuers who are developing plans for new high-yield products across the U.S., Europe and Asia.

Investors are now betting that corporate Bitcoin holdings can support the broader market for preferred stocks and similar bond-like products.

How leverage turned a stable trade into a cascade

The leverage built up in preferred stocks, which had appeared to be stable, was undone in the ensuing rush of liquidations.

Strategy and Strive, the largest Bitcoin holding companies with over 800,000 BTC, used preferred stock to raise capital without selling common stock or relying entirely on traditional debt. Securities typically have an stated price of $100, pay fixed or variable dividends, and have no maturity date.

This structure provides issuers with long-term funds that can be used for Bitcoin purchases and other corporate needs. Investors receive income that exceeds the yield earned from many traditional fixed income products without directly owning Bitcoin.

Strategy’s STRC and Strive’s SATA have emerged as the two largest devices on the market. Strategy can adjust STRC’s dividend to keep the stock close to $100, while SATA offers a variable dividend and distributes dividends daily.

For several months, both securities traded within a relatively narrow range around their par value. BitcoinTreasuries.net said in its June company adoption report that this stability encouraged some investors to borrow funds to increase their positions and expand their dividend income.

This strategy worked as long as stock prices were stable and dividends exceeded the cost of financing the trade.

That calculus began to break down in June, when Bitcoin fell below $60,000 and selling pressure spread across crypto-related companies and securities.

Since June 18, STRC and SATA have fallen significantly below par. The drop in price led to margin calls for leveraged STRC holders, forcing them to sell into an already weakened market and prompting further liquidations.

SATA also fell due to pressure from its own market conditions and the spillover from the drop in STRC.

STRC eventually fell to about $75, about 25% below list price. Meanwhile, SATA has fallen to around $88. Even though preferred stocks continued to pay dividends on schedule, Bitcoin’s decline weighed on investor sentiment.

Leverage has turned a product created to generate stable income into another source of volatility. High dividends may attract buyers after a decline, but offer little protection to indebted investors once they have to sell.

Higher dividends have also made financing more costly for issuers. Strategy responded by increasing STRC’s annual dividend to 12% and implementing a broader capital framework, including $2.55 billion in cash reserves, preferred stock buyback authority, and permission to sell some Bitcoin under certain conditions.

The company said the reserves are sufficient to cover approximately 17 months of expected preferred dividend and interest payments. It also acknowledged that STRC could fall well below its target range, leaving the market to decide whether the dividend hike is enough to restore demand.

Price recovers as Bitcoin purchases continue

Despite the decline in June, the market stabilized faster than the initial liquidation suggested. Prices have recovered, trading volumes are at record highs, and corporate bonds continue to be bought. Bitcoin.

At the time of publication, STRC has recovered from a low of around $75 to around $87, while SATA has risen to around $97.

The uneven rebound suggested that investors were distinguishing between the two securities rather than abandoning the broader market.

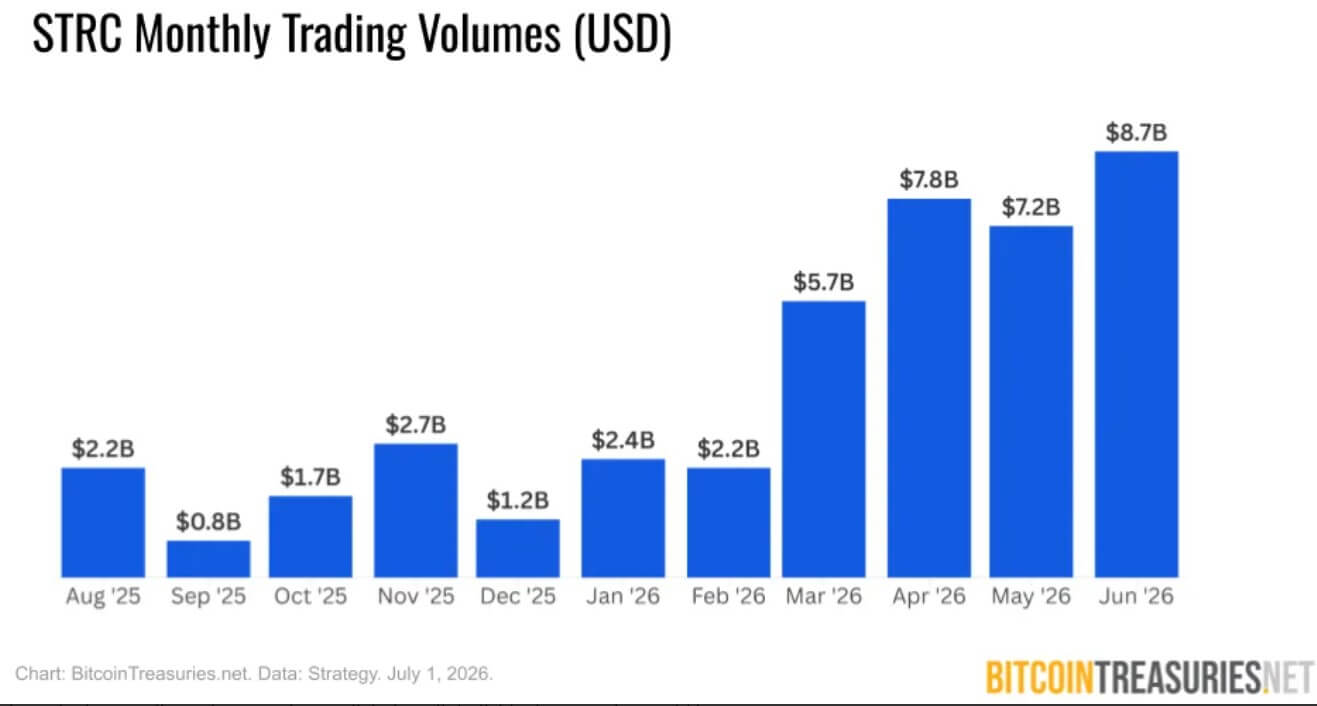

Trading activity also accelerated during the turmoil. Combined sales for STRC and SATA in June exceeded $10 billion, even though both products were below their list price of $100.

Of this, STRC accounted for $8.7 billion, the highest monthly trading volume ever, and two of the five busiest trading weeks. SATA generated nearly $1.5 billion, almost twice as much as in May, with three of its four strongest weeks occurring in that month.

The deal was maintained with significant price revisions. Buyers absorbed stock from leveraged sellers, kept the market open and dividend payments uninterrupted.

However, high activity in the secondary market did not lead to new capital for issuers. Both STRC and SATA were unable to raise funds through over-the-counter sales in June, as most transactions involved the transfer of existing shares between investors.

Still, Strategy and Strive expanded its Bitcoin holdings despite the moratorium on preferred stock issuance.

Strategy added a net amount of 3,625 Bitcoin during the month, while Strive acquired 3,364 Bitcoin. The two companies will be responsible for the majority of corporate Bitcoin purchases in June, each spending about $200 million.

Supporters saw the continued buying as evidence that June’s turmoil was due to overleveraging of securities rather than waning confidence in corporate Bitcoin accumulation.

New entrants push this model outside the US

The recovery in trading and continued purchases of Bitcoin by businesses is now prompting treasury firms to consider whether their credit models can expand beyond the United States.

On July 10th, Metaplanet provided the latest indication by announcing a joint study on tokenized credit products in Japan.

The Tokyo-listed company will collaborate with Siiibo Securities, Yen stablecoin issuer JPYC, and regulated security token platform Progmat to explore products that use Bitcoin as a backing asset or source of credit support. Metaplanet recently acquired Siiibo for $13 million.

According to the company,

“Digital credit backed by Bitcoin could evolve into a product that can be traded and settled around the world 24 hours a day, 365 days a year, and accrue interest and dividends on a daily basis depending on the holding period.”

The initiative targets long-standing barriers in Japan’s corporate credit market, where small and growing companies can face high costs in product design, distribution, investor management, interest payments and redemptions.

Metaplanet and its partners said digital infrastructure can reduce some of these costs. Their proposal combines stablecoins for payments and distributions, security tokens to record ownership and transfer rights, and Bitcoin as an asset to support securities.

This structure reduces reliance on traditional record dates by allowing investors to calculate interest based on how long they hold the product. Trading and settlement outside of normal market hours may also be possible.

This project is still in its early stages, with no publication date, return, distribution plan, or final structure determined. The companies have not yet decided whether to conduct a proof of concept.

Metaplanet also does not disclose whether investors have a direct legal claim to a given Bitcoin. The details will determine whether the product functions as a formally protected commodity or relies more broadly on the issuer’s balance sheet and crypto reserves.

Metaplanet holds 43,000 Bitcoins, ranking third among publicly traded companies in terms of BTC holdings.

Bitcoin digital credit growth forecast responds to tougher market

Metaplanet’s planned entry lends weight to expectations that Bitcoin-backed credit will expand, but the June selloff has made investors more aware of the risks behind these predictions.

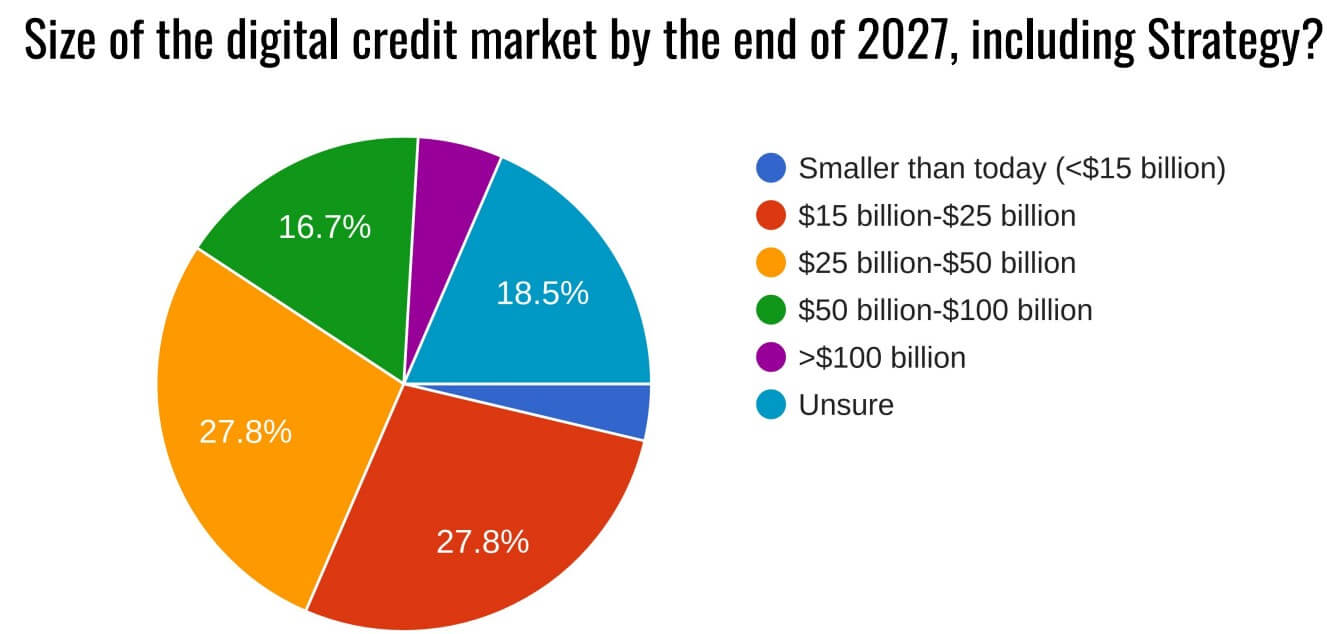

According to a BitcoinTreasuries.net survey, 78% of respondents expect the digital credit market to grow until the end of 2027. Additionally, 22% predict that the supply balance could exceed $50 billion, with some predicting it could exceed $100 billion.

However, this result reflects a group that is already more likely to support the product. According to the report, 87% of respondents view digital credit favorably, and 72% have invested in the sector. About 76% also expect similar sharp price declines to occur again.

This mix of confidence and caution has led to a more cautious assessment for June. Investors remain optimistic about the market’s long-term potential, while acknowledging that leverage and liquidity can cause significant deviations from par.

Michael Saylor argued that Bitcoin facilitates the assessment of digital trust because its main market risks are tied to globally traded and continuously observable assets. Investors can track Bitcoin price and volatility in real time and incorporate those movements into their valuation models.

June proved that Bitcoin-backed credit can withstand liquidation shocks. The next hurdle is persuading investors to fund the new issue as key products trade below par.

(Tag translation) Bitcoin