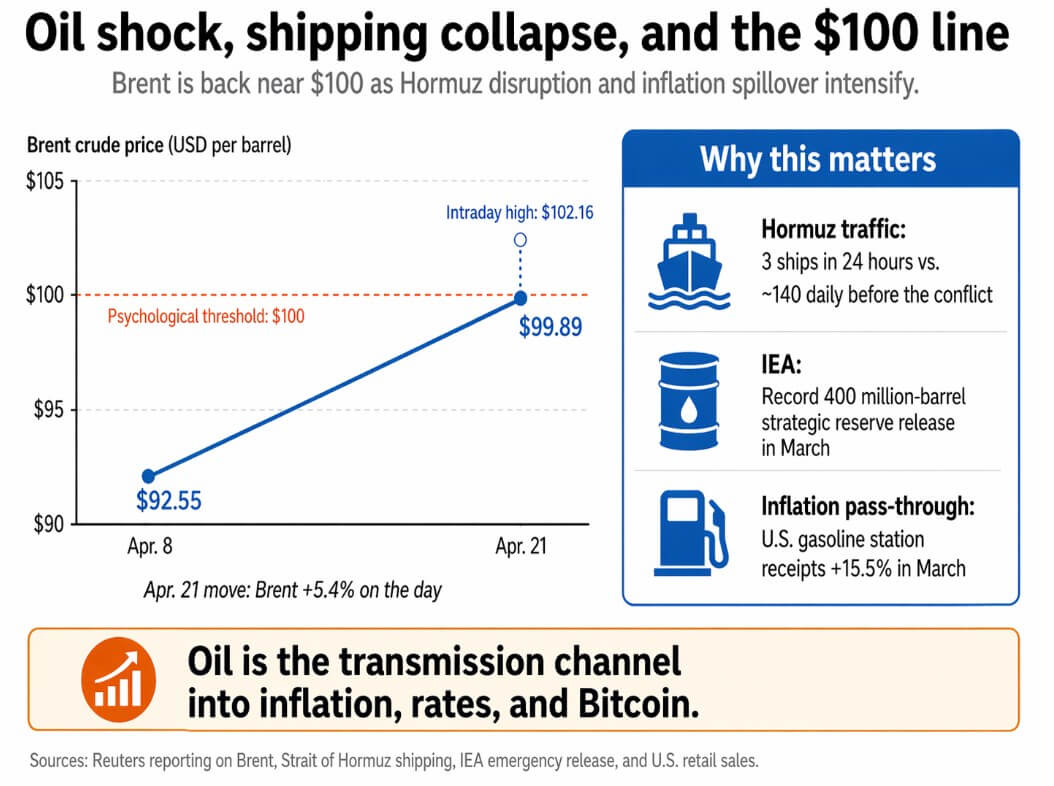

On April 21, Brent crude oil prices rose 5.4% to close at $99.89, hitting an intraday high of $102.16.

The move was driven by the fact that shipping operations through the Strait of Hormuz remain severely affected, with reports saying only three vessels passed through in the past 24 hours, down from about 140 vessels per day before the conflict began.

The IEA’s Fatih Birol called it the biggest energy crisis in history, orchestrating a record release of 400 million barrels from strategic stockpiles in March.

The energy shock is already having clear side effects on financial markets, with U.S. retail sales higher than expected in March, largely due to a 15.5% rise in gas station sales linked to war-induced fuel prices.

Oil shocks are specifically linked to consumer-level inflation, further reinforcing levels already priced in by interest rate markets.

pricing channel

This week, Bitcoin has been trading on the basis that oil prices have remained high long enough to keep inflation tenacious, yields are strong, and the Fed is likely to cut interest rates later than the market expects.

By late February, the federal funds futures market had priced in two quarter-point rate cuts through December. As of April 21, futures were pricing in only a 30% chance of one 25 basis point rate cut for the year.

This repricing of the interest rate path directly tracks the impact of the war on energy costs. On the same day, the 10-year Treasury yield was 4.313% and the 2-year Treasury yield was 3.802%, both of which rose during trading hours.

On April 21st, oil prices rose, the dollar strengthened, and US Treasury yields rose, but Bitcoin remained stagnant. Even the classic inflation hedge failed, with gold down 2% as rising real funding conditions and a strong dollar overwhelmed normal conditions.

Deutsche Bank made the downstream risks clear in its April 17 conference call, arguing that oil-driven inflation could cause the Fed to keep interest rates on hold until 2026.

As the April 7 ceasefire progressed and Brent fell to $92.55 the next day, yields fell, traders re-established a 50% probability of a Fed rate cut by the end of the year, and Bitcoin rose 2.95% to $72,738.16.

This sequence confirmed a transmission channel in which the rate path eases as the oil softens, and the BTC rises as the rate path becomes easier.

| macro variable | April 21st Reading Shift | Why is it important for BTC? |

|---|---|---|

| brent crude oil | Closing time $99.89touched $102.16 during the day | High oil prices increase inflation pressures and strengthen macro headwinds |

| supply path | from 2 quarter points reduction by December Only 1 year since late February The probability of one 25bp rate cut is 30%. throughout the year | Lower easing expectations mean lower liquidity support for BTC |

| 10 year government bond yield | 4.313% | Financial environment tightens due to rise in long-term interest rates |

| 2 year government bond yield | 3.802% | Rising front-end yields reflect tougher interest rate outlook |

| dollar | Strengthened on April 21st | A strong dollar is typically a headwind for Bitcoin and other risky assets. |

| gold | fell 2% | Classic inflation hedges also show pressure from yields and dollar strength |

| Bitcoin | Recovered towards the late $70,000 level and remained around $78,000 April 22nd | Although not a complete breakdown, macro sensitivity has been confirmed. |

| Comparison of ceasefire agreements | above April 8thBrent fell into $92.55cut odds improved and BTC rose 2.95% to $72,738.16 | Strengthening the transmission channel: softening the oil → facilitating the rate path → strengthening the BTC |

Hormuz disruptions are measured and documented, inflationary pass-through is visible in retail sales data, and futures markets track Fed price changes. What remains to be seen is how Bitcoin resolves the tension between these headwinds and its current position near $78,000.

There are two movements this week.

If Brent oil prices remain above $100 and the two-year Treasury yield continues to rise from its current 3.80%, market prices will likely see more persistent inflation, fewer interest rate cuts, and tighter liquidity conditions.

Bitcoin has fallen and retested support towards the mid-$70,000s, supporting the view that BTC is in high beta for interest rate expectations. The April 21st pattern of higher oil, higher dollar, higher yields, and lower BTC is playing out again with more conviction.

This is the more straightforward case in the short term, as most of the structural work has already been completed by re-pricing the Fed path based on war.

The bullish case will materialize if Brent remains near $100, Holmes remains impaired, yields remain high, and Bitcoin remains flat or near $78,000 while stocks and gold are under pressure.

This resilience will provide evidence of relative strength in the face of textbook macro headwinds. A week of this kind of robustness that has built up against sustained oil stress will weaken the war-established “higher oil = lower BTC” template.

| scenario | What Brent is doing | what does yield do | What BTC does | What the market concludes |

|---|---|---|---|---|

| Bears/macro pressure wins | keep the above 100 dollars | 2-year bond yield higher than current 3.80% area | BTC dips below mid-$70,000 and retests lower support | Bitcoin still trades like a high beta rate sensitive asset |

| Bull/relative strength appears | stay nearby 100 dollars but it doesn’t accelerate | Yields will continue to rise without collapsing | BTC remains flat or corporate around $78,000 | Bitcoin Shows Resilience Despite Typical Macro Headwinds |

Bitcoin’s April 21st session has already demonstrated that Bitcoin trades as a macro-sensitive asset in this setup. Given the unfavorable macro environment, which remains strong, the relative strength sustained over the week will carry more weight.

The three numbers we will be tracking closely this week are Brent, the 2-year US Treasury yield, and Bitcoin’s ability to sustain the high $70,000s.

(Tag to translate) Bitcoin