On April 22nd, Bitcoin prices hit an intraday high of $79,485 as broader risk assets rallied on release from the ceasefire.

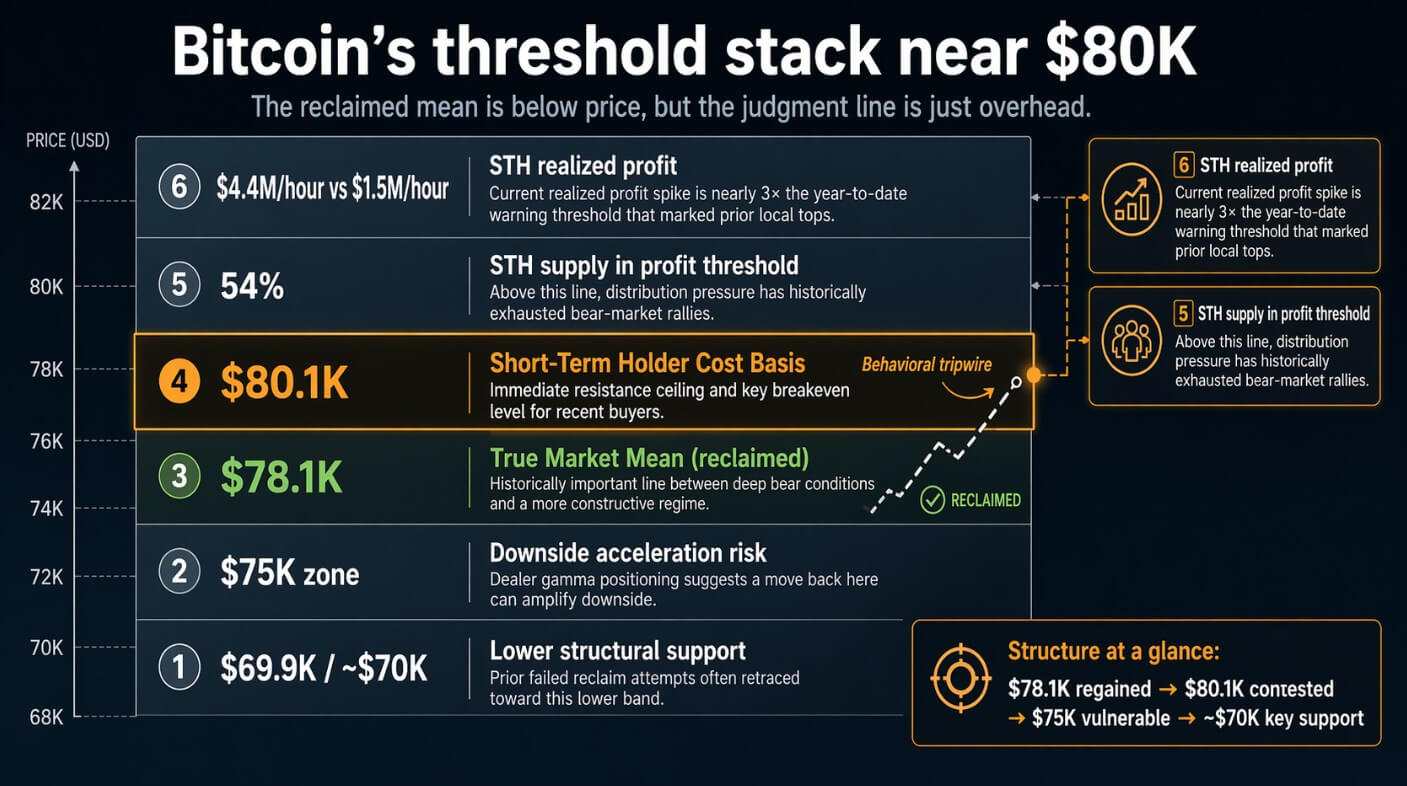

On-chain data frames Bitcoin (BTC)’s approach to $80,000 as a behavioral tripwire, an upper limit constructed from recent purchaser break-even sentiment.

Glassnode states that BTC has regained the true market average of $78,100, a threshold the company has set as the boundary between a severe bear market situation and a regime in which a return to the average is reliable.

In a recent report, Glassnode said the market faces a more difficult problem around $80,000 with three overlapping seller mechanisms, each reinforcing the next.

The first is the short-term holder cost basis, which is the average acquisition price of the coin purchased over the past 155 days, which is $80,100. This is the most price-sensitive segment of the market, and break-even points turn into supply, as buyers who have waited months for a leveling out are unlikely to take any further risks the moment the entry price recovers.

The second is the 54% profit line, where a push towards $80,100 would see the supply share of short-term holders contributing to the profit, pushing Glassnode above the statistical average of 54%, which is consistent with the peak share during the bear market rally.

Once enough recent buyers return to their funds, the bailout turns into a sell at a pace that the market has to absorb.

The third mechanism has seen realized gains for short-term holders surge to $4.4 million per hour, nearly triple the $1.5 million per hour warning line that Glassnode claims marked the local top so far this year.

The market is already testing whether new demand can absorb the selling.

macro background

Bitcoin is putting pressure on its overhead supply zone against the backdrop of a restrictive macro environment.

US CPI rose 0.9% month-on-month and 3.3% year-on-year in March, with gasoline accounting for nearly three-quarters of the overall increase.

Core CPI was 0.2% month-on-month and 2.6% annualized, indicating a moderate increase in the Fed’s assessment, although the headline acceleration remains intact. Even if the core trend remains at 2.6% year over year, the Fed cannot ignore a reacceleration of this magnitude in headline inflation.

The number of employed people increased by 178,000 in March, the unemployment rate remained at 4.3%, and the average weekly working hours decreased to 34.2 hours. The results are robust enough to delay policy easing while maintaining growth concerns, and are exactly the kind of report that locks in uncertainty in both growth and policy.

An April 22 Reuters survey of economists found that PCE inflation remained elevated at 3.7% in the second quarter, 3.4% in the third quarter, and 3.2% in the fourth quarter due to the impact of war-induced energy prices, reflecting the cumulative effect of the Fed waiting at least six months before cutting interest rates.

Nearly 33% of economists expect interest rates to remain unchanged through 2026. On the day Bitcoin rose, Brent crude oil was $100.58, U.S. crude oil was $91.54, and the 10-year Treasury yield was close to 4.286%, making up the rest of the picture.

While Bitcoin rallied following ceasefire relief, oil rose along with it, leaving the macro constraints that defined this year’s drawdown intact.

image of demand

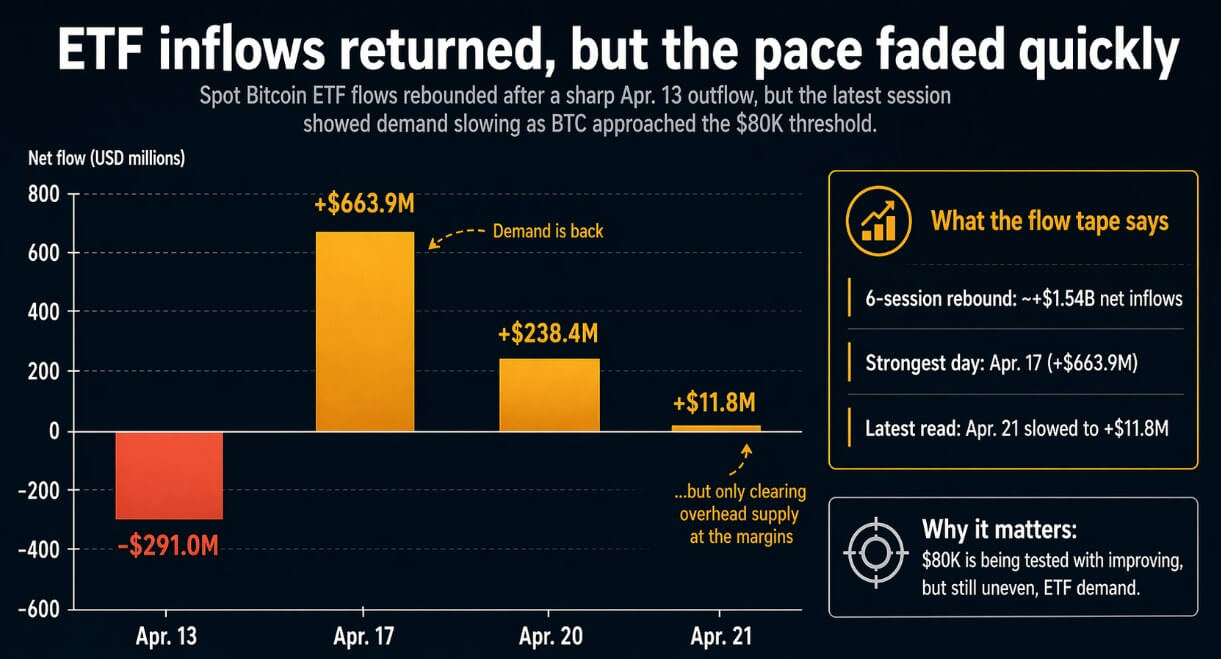

Six trading sessions have taken place since the $291 million outflow on April 13, resulting in total net inflows of approximately $1.54 billion through April 21, including $663.9 million on April 17 and $238.4 million on April 20, according to data from Pharside Investors.

In the most recent transaction, it decelerated sharply to $11.8 million, with bids returning and indicating that overhead supply is only being cleared at the last minute.

According to Glassnode, cumulative volume delta has started to increase, with Binance leading the buying curve, while Coinbase has remained relatively subdued. This split has led to offshore and crypto-native buyers driving the rally, while US institutional demand has been relatively quiet.

Derivatives convey a more cautious version of the same situation, with funding rates on major exchanges remaining negative in March and April. This positioning indicates that negative funding could fuel the squeeze if Bitcoin is forced to break out, and also indicates that the market is still positioned for further decline on this move.

Meanwhile, 30-day realized volatility has fallen to 40.7% from 49% at the beginning of April, and the volatility risk premium has compressed to near zero, indicating that options are pricing in range-based volatility.

Two solutions to the current situation

In the bullish case, demand absorbs breakeven sellers. If continued positive ETF flows and solid spot buying combine to sustain levels above $80,100, it would mean new buyers are finally overcoming the short-term holder distribution.

With funding still negative, this resolution could trigger a squeeze, forcing short covering and accelerating gains beyond those available from spot purchases alone.

Using Glassnode’s 40.7% realized volatility, the 30-day 1 standard deviation envelope is approximately $69,600 to $87,900. A bullish resolution pulls the market towards the upper end of its band.

In a bearish case, the judgment line is established. If the price stalls around $80,000 and ETF inflows remain modest, the realized profit trend is already at a level consistent with previous local highs.

A rejection from $80,100 comes with certain downside risk related to dealer positioning, as Glassnode’s options analysis shows the heaviest negative gamma around $75,000, where dealer hedging could amplify the downside.

A pullback into the mid-$75,000 area puts it in that acceleration zone, below which the next important structural floor is $69,900, and previous attempts to restore cost standards for short-term holders have historically fallen back toward this floor.

| macro input | read | Why is it important for BTC? |

|---|---|---|

| Consumer price index (March) | 0.9% compared to the previous month, 3.3% compared to the previous year | Hot headline inflation limits Fed flexibility |

| Core CPI | 0.2% compared to the previous month, 2.6% compared to the previous year | Softens, but not enough to change macro tone |

| Payroll calculation | 178,000 | Labor force remains strong enough to delay cuts |

| unemployment | 4.3% | No emergency mitigation signal |

| Fed outlook | At least 6 months before cutting | Delay in macro rescue of risk assets |

| Outlook for PCE | 2nd quarter 3.7% / 3rd quarter 3.4% / 4th quarter 3.2% | Inflation is expected to remain high |

| brent | $100.58 | Energy maintains inflationary pressures |

| US 10 year yield | 4.286% | Rising interest rates will limit the financial situation |

The same volatility envelope that gives room to the bull case also shows that the $75,000 test is well within normal 7-day volatility.

Bitcoin has regained the line that ended the deep bear market, but the reward for that recovery is a more difficult test almost overhead, owned by buyers who waited months for it to level out.

(Tag to translate) Bitcoin