Bitcoin enters the second half of the year with the support systems that underpinned its previous rally still under pressure.

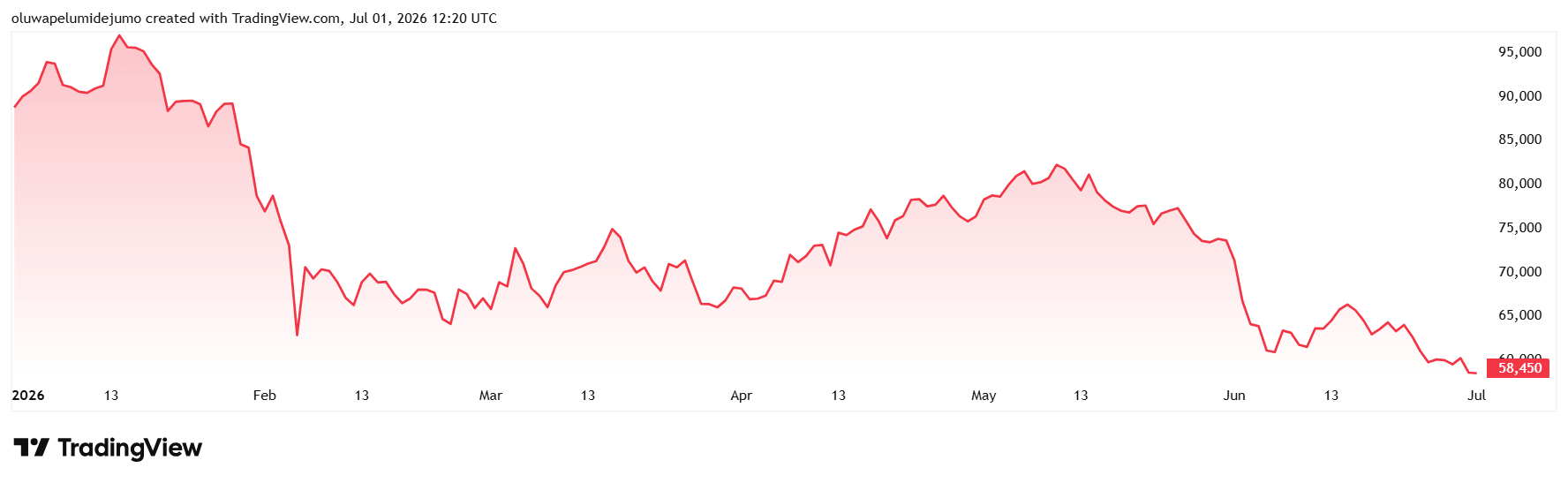

data from crypto slate The largest digital asset is down about 33% this year, down more than 50% from October’s record high of $126,000, and at the time of writing is trading near its lowest level since September 2024 at about $58,600, according to .

This price movement pushed Bitcoin below key long-term trend levels, giving the first half of 2026 its worst start since the 2022 crypto crisis.

Therefore, July will be a test of whether the market is nearing depletion or if a new decline begins. There are three pressure points over the next four weeks: whether exchange-traded fund (ETF) outflows slow, whether the Fed signals another rate hike, and whether Congress can pass the CLARITY Act before its August recess.

This outcome could determine whether Bitcoin rebounds toward $100,000 by the end of the year or retests the $50,000 to $55,000 area, which analysts currently see as the next major structural support zone.

ETF demand has turned from cushion to pressure

ETF flows have become one of the clearest signs that institutional support for Bitcoin is waning.

The U.S. Spot Bitcoin ETF recorded net outflows of about $4.5 billion in June, the worst month since the commodity began trading in January 2024, according to data from SoSoValue.

BlackRock’s IBIT accounted for the majority of withdrawals, highlighting how Bitcoin’s largest regulated demand channel is a source of sustained selling pressure.

The weakness was spread throughout the month rather than being concentrated in a single trading session. The Spot Bitcoin ETF recorded inflows on just three days in June, and those positive days totaled less than $100 million.

The remainder of the month was dominated by redemptions, with several sessions in which hundreds of millions of dollars were drained from the product.

This pressure continued as Bitcoin fell below the $60,000 area, calling into question one of the core assumptions behind the ETF-driven phase of the market: that regulated funds would provide a stable demand base during drawdowns.

Bitcoin analysis platform Ecoinometrics said the decline is consistent with pressures seen in capital flows, noting:

“Bitcoin falling below $60,000 should not surprise anyone who follows the ETF movement.The last 30 days have been a great sell-off, but they have actually been characterized by relentless selling.”

The firm said the Spot Bitcoin ETF has seen outflows in nearly every recent trading session, creating one of the most sustained outflows since the fund’s inception. He further added:

“This is a kind of demand shock that continues to push prices down.”

However, withdrawal does not necessarily indicate panic selling.

This is because many ETF investors may have entered the market at lower prices to book profits or reduce exposure following Bitcoin’s meteoric rise last year. But continued outflows indicate that institutional investors have not yet stepped in to absorb the decline.

This marks a clear shift from earlier in the cycle, when ETF demand drew Bitcoin deeper into mainstream portfolios and helped provide tangible new capital flows. In June, a similar structure showed how quickly large allocators can exit when prices decline, the macro environment tightens, and momentum weakens.

The market is currently treating ETF flows as a better measure of confidence in top cryptocurrencies.

Therefore, a return to steady inflows may suggest that institutional investors are willing to restructure their exposures after drawdowns.

But if redemptions continue, Bitcoin will become more dependent on long-term holders and less protected by Wall Street demand into the second half of the year.

The Fed has abolished its interest rate cut trade

The ETF withdrawal comes just as the rate cut narrative that underpinned much of the optimism at the start of the year has collapsed.

The Fed kept interest rates unchanged at its June meeting, but the decision itself did not move the market. That was the tone.

Under Chairman Kevin Warsh, policymakers have shifted to a more hawkish stance as inflation remains above target and tariff-related price pressures continue to show up in consumer data.

This has forced traders to reprice the stock for the second half of the year. The easing in interest rates that many crypto investors expected to occur under a Trump-appointed Fed chairman is no longer the base case. Markets are currently considering the possibility that the next move will be a rate hike rather than a rate cut.

This change is significant for Bitcoin because this asset does not pay any yield.

As Treasury yields rise and the dollar strengthens, investors have less incentive to hold assets whose value depends heavily on liquidity expectations. Bitcoin is absorbing that pressure even as its ETF channel is being redeemed.

The Fed’s change in tone also overturns one of the market’s previous assumptions about Warsh. Since President Donald Trump has long pushed for lower interest rates, many crypto investors expected him to become dovish.

But the expectations weren’t as solid as the market was treating them to. Although the survey suggested only a slight dovish tilt on interest rates, many investors expected Mr. Warsh to take a tougher stance on the Fed’s balance sheet and maintain some degree of independence from the White House.

A reset was forced at the June meeting. In March, policymakers were still leaning toward one or two rate cuts by the end of the year. By June, the median forecast had shifted in favor of a likely rate hike, although the committee remained divided.

This will prevent Bitcoin from receiving the macro support many investors were hoping for heading into the summer.

Financial conditions are not easing, the dollar is firm and US Treasury yields are moving back toward recent highs. This is a difficult backdrop for an asset that is still treated as a high-beta liquidity trade by many allocators.

Strategy shift raises questions about demand for BTC government bonds

Meanwhile, market pressure spread to corporate Bitcoin financial transactions, with Strategy’s first sale in years attracting attention far beyond the size of the transaction.

Strategy (formerly MicroStrategy) revealed in May that it had sold 32 Bitcoins worth approximately $2.5 million. This sale represented only a small portion of the company’s holdings and had little impact on the company’s overall exposure.

But the bigger concern was the signal it sent to a market that has long seen Strategy as Bitcoin’s most avid corporate buyer.

For most of the cycle, Strategy represented a simple trade: raise money, buy Bitcoin, and maintain volatility. This has made it an important reference point for investors, especially as spot ETF inflows and corporate bond purchases reinforce each other.

The sale complicated that view. The report suggested that Strategy may be ready to treat Bitcoin as part of a broader capital management strategy, rather than as an asset reserved solely for accumulation.

The company later strengthened that policy, saying it may sell some of its Bitcoin holdings to strengthen its balance sheet, support perpetual preferred securities and fund share buybacks.

The statement gave investors a clearer view of how management plans to balance Bitcoin exposure with liquidity needs, funding costs, and shareholder returns.

The strategy remains closely tied to Bitcoin. Their holdings are still large, and one small sale after years of purchases does not change the market supply balance.

Still, the company’s new flexibility raises broader questions about whether Bitcoin treasury companies can continue to serve as stable buyers if prices slump and funding conditions tighten.

This issue has become more important as Strategies adjusts its funding structure, dividend commitments, and reserve policies.

This framework could increase corporate resilience by improving liquidity and reducing balance sheet strain. It also gives management more room to prioritize financial discipline over continued Bitcoin purchases.

This change adds another source of uncertainty to a market already under pressure from ETF outflows. Stable corporate ownership could help absorb weaknesses. A slowdown in purchases and further deleveraging would result in the loss of some of the demand base that had supported Bitcoin’s previous rise.

AI competes for the same risk capital

Despite this, Bitcoin is competing for capital in a market where artificial intelligence is the preferred risk trade.

Over the past year, hedge funds, asset managers and wealth advisors have poured money into AI stocks as investors seek exposure to one of the fastest-growing themes in global markets.

That demand is spilling over into new public offerings, derivatives and exchange-traded products related to companies seen as benefiting from building AI.

That appetite is keeping risk-taking alive on Wall Street. But much of the money is going to chipmakers, data center operators, software companies, and other companies that have a clearer link between AI infrastructure and revenue, rather than cryptocurrencies.

This split complicates Bitcoin’s market signals. That decline was not caused by investors completely abandoning risk. Capital is still moving into the speculative space, but Bitcoin is no longer the primary destination.

As major technology companies continue to invest heavily in chips, cloud capacity, and data centers, AI provides investors with a more direct company growth story.

In contrast, Bitcoin is entering the second half of the year with reduced ETF flows, policy uncertainty, and new questions about corporate financial needs.

This divergence has left Bitcoin out of the rally of other high-growth assets. If AI continues to absorb capital over the summer, it may take a more powerful catalyst than a drop in price for Bitcoin to regain investor attention.

CLARITY Act triggers policy in July

After an early period shaped by ETF outflows, new interest rate pressures, and questions over corporate Bitcoin buyers, the Senate date was one of the few short-term openings for a change in sentiment for cryptocurrencies.

The CLARITY Act would create a federal market structure framework for digital assets and define the roles of the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

This passage will give exchanges, banks, asset managers, and token issuers a clearer foundation on which to build products and expand services in the United States.

Any delays or failures will leave the industry facing the same regulatory uncertainty that has weighed on investment, product development and market confidence for years.

The timing is tough, as Senate leaders have limited time until the August recess, while lawmakers still need to coordinate committees, address Democratic concerns over ethics and illicit finance provisions, and secure enough votes to pass the bill on the floor.

Therefore, July will be an important test for the market. If the bill moves forward, Bitcoin could receive a policy boost at a time when ETF redemptions and macro conditions are weighing on risk appetite.

But if this effort is pushed into the fall, one of the clearest sources of potential positive sentiment in the second half of the year will fade.

With this in mind, Kraken Chief Economist Thomas Perfumo said the Clarity Act is a trigger to watch over the next four weeks, and its passage could help restore sentiment and momentum.

Notably, Grayscale also ties this bill to Bitcoin’s near-term path, placing it alongside Strategies’ balance sheet decisions and the Fed’s interest rate outlook as factors that could determine whether Bitcoin approaches its lows or remains exposed to further losses.

(Tag translation) Bitcoin