Quantum computing has long served as Bitcoin’s most cinematic threat. This includes grave warnings, strange machines, broken ciphers, and the right ingredients for a possible future rewriting of digital trust.

But the bigger danger facing Bitcoin today seems much more mundane and much more commercial. It is artificial intelligence, and its key point is electricity.

The pressure is already visible. As of today, Bitcoin is trading at $77,845 crypto slateincreased by 5% in 24 hours, 6.7% in 7 days, and 9.2% in 30 days.

Although prices have rebounded over the past month, the mining side of the network still operates in a tougher economic environment than the casual surface of the market would suggest.

CoinShares said in its Q1 2026 mining report that the weighted average cash cost to produce one Bitcoin among listed miners rose to approximately $79,995 in Q4 2025. The report states that with current hash prices of about $30 per petahash per day, an estimated 15% to 20% of the world’s fleet could remain underwater if power costs were high enough.

That’s where AI comes in, with a much sharper edge than quantum. Quantum remains a serious long-term crypto problem. The transition clock is real, IBM’s roadmap targets the first large-scale fault-tolerant quantum computer by 2029, and NIST has already completed the first post-quantum standard.

Those milestones are noteworthy. They also describe the technology path we need to take in the future.

AI is already bidding for the same powered campuses, the same substations, the same fiber routes, and the same land locations that gave industrial Bitcoin miners strategic value in the first place.

The roadmap includes one threat. Another is already signing leases and making capital conversions, changing how these companies use their best assets.

AI has already taken over premium sites

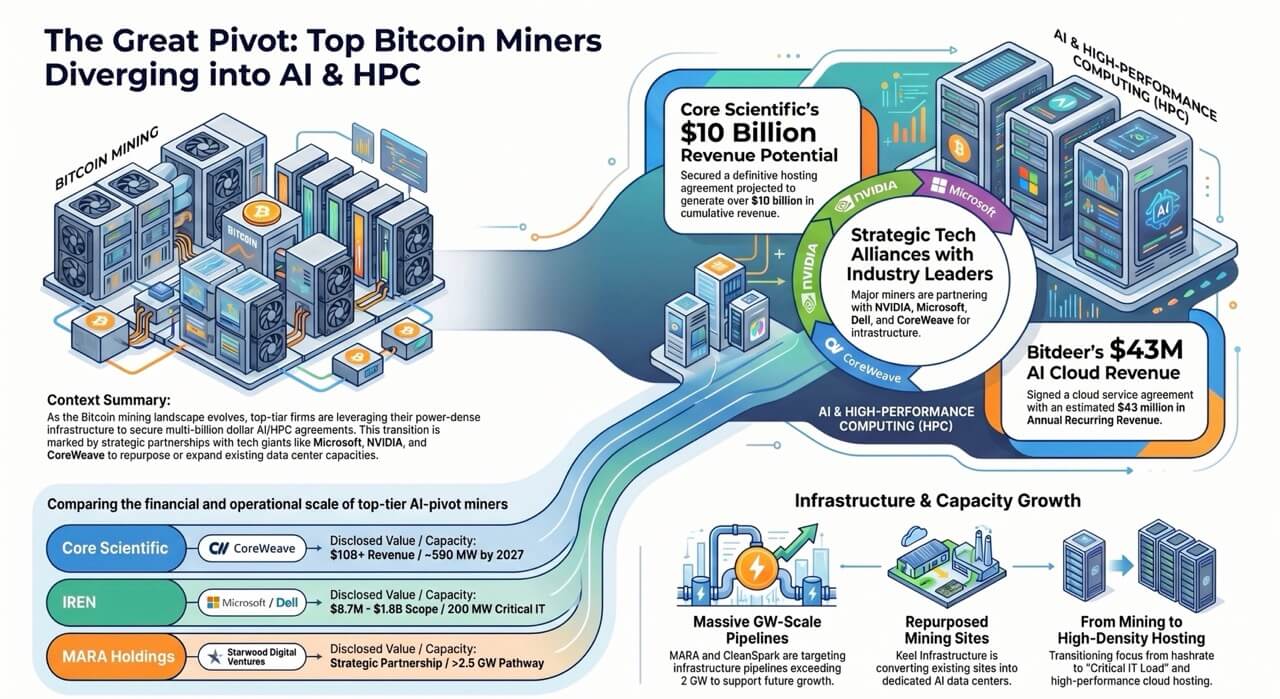

The strongest evidence comes from what miners physically do at the facility. Bitdeer announced in March that it had begun decommissioning Bitcoin mining rigs at its Tidal site in Norway to make room for a new AI data center.

That’s more important than many future disastrous posts about “Q-Day”. Miners with deep Bitcoin roots have chosen to remove rigs from active mining sites because the economics of AI infrastructure allow for better use of space.

Bitdeer also revealed that its annual recurring revenue from external GPU cloud subscriptions was approximately $21 million as of February 28, and negotiations are underway with additional colocation tenants. The movement is concrete and has already begun.

Riot came to a similar conclusion from a different angle. Riot said in its 2025 full-year financial results that its data center lease with AMD is up and running and generating revenue from January 2026.

The company also revealed that Rockdale could evolve into an even larger data center campus over time.

Core Scientific goes even further. The company said in its fourth quarter 2025 financial results that it has already delivered approximately 350 MW of power under the CoreWeave contract and is on track to deliver approximately 590 MW by early 2027.

MARA’s partnership with Starwood was equally revealing in another sense, as it described a campus designed to operate both Bitcoin mining and AI computing, with the ability to switch workloads depending on pricing and customer demand.

This pattern extends far beyond a single company. According to the current hash rate ranking of public miners, the top public miners by operation size are Bitdeer with 69.5 EH/s, MARA with 61.7 EH/s, CleanSpark with 47.3 EH/s, IREN with 43 EH/s, and Riot with 36.4 EH/s.

This is an important part of the Bitcoin mining industry, which is already divided into three camps. Some miners have entered into actual AI or HPC contracts and are moving capacity. Some come with frameworks and initial pilots. Some are still heavily tied to Bitcoin.

CoinShares estimates that with more than $70 billion in cumulative AI and HPC contracts currently announced across the public mining sector, publicly traded miners could derive 70% of their revenue from AI by the end of this year, up from around 30% currently.

| rank | miner | Current EH/sec | Planned EH/sec | AI/HPC | situation |

|---|---|---|---|---|---|

| 1 | BitDeer (NASDAQ: BTDR) | 69.50 | 8.60 | AI Cloud’s ARR is approximately $43 million. Tydal Norway AI colocation construction. Tenant value is not disclosed | Build out in progress |

| 2 | MARA Holdings (NASDAQ: MARA) | 61.70 | Not applicable | Starwood Digital Ventures; AI Infrastructure Platform. 1GW capacity in the short term. Value is private | framework |

| 3 | Clean Spark (NASDAQ: CLSK) | 47.30 | 2.70 | Submer framework for AI and HPC campuses. Contract amount not disclosed | framework |

| 4 | IREN (NASDAQ: IREN) | 43.00 | 3.00 | The Microsoft AI cloud contract is approximately $9.7 billion. Dell hardware purchases approximately $5.8 billion | signed |

| 5 | Riot Platform (NASDAQ: RIOT) | 36.40 | 6.10 | AMD Lease and Service Agreements. The base price is approximately $311 million. Up to approximately $1 billion with extensions | signed |

| 6 | Cango (NYSE:CANG) | 27.98 | 9.03 | DL Holdings funds EcoHash AI and HPC. $65 million investment and $10 million bill | signed loan |

| 7 | HIVE Digital (NASDAQ: HIVE) | 22.20 | 3.30 | BUZZ HPC signs AI cloud contract. The total value of the two-year contract is approximately $30 million. | signed |

| 8 | American Bitcoin (Private) | 21.90 | 6.20 | No AI or HPC contracts disclosed | No disclosure |

| 9 | Core Scientific (NASDAQ: CORZ) | 15.70 | 2.20 | CoreWeave Hosting Agreement. Potential cumulative revenue of over $10 billion | signed |

| 10 | keel infrastructure | 14.80 | Not applicable | Washington AI and HPC Site Transformation. $128 million binding contract | binding |

This reversal is shaping the sector today. The publicly traded companies that once peddled leveraged bets on Bitcoin are increasingly looking like owners of scarce power infrastructure that can be rented to a richer customer base.

This change does not require anyone to stop believing in Bitcoin. All you need is a board that compares cash flows from mining with cash flows from leasing premium power and computing space. The rest is done by fiduciary duty.

Bitcoin crisis is imminent

Although the average price of Bitcoin is around $80,000, the revenue picture is still skewed toward sector-level mining.

Even using the current hashrate distribution of the top 10 public miners and allocating annual block rewards proportional to operational hashes, this group still generates a larger Bitcoin revenue pool than the AI contract base currently seen across the same cohort.

Therefore, even after the sector gains attention to AI and HPC, Bitcoin will remain in the lead in terms of total revenue.

The balance shifts when the comparison moves from the group as a whole to the companies with the strongest infrastructure contracts. This is because a small number of companies already have AI economics that match or exceed what the Bitcoin fleet could produce at this price level.

| company | Current hash rate (EH/s) | Estimated BTC mined per year | BTC revenue $80,000 | BTC revenue is $160,000 |

|---|---|---|---|---|

| bit deer | 69.50 | 11,210.2 | $896.8 million | $1.794 billion |

| Mara | 61.70 | 9,952.1 | $796.2 million | $1.592 billion |

| clean spark | 47.30 | 7,629.4 | $610.3 million | $1.221 billion |

| Airen | 43.00 | 6,935.8 | $554.9 million | $1.11 billion |

| riot | 36.40 | 5,871.2 | $469.7 million | $939.4 million |

| Kango | 27.98 | 4,513.1 | $361 million | $722.1 million |

| hive | 22.20 | 3,580.8 | $286.5 million | $572.9 million |

| american bitcoin | 21.90 | 3,532.4 | $282.6 million | $565.2 million |

| core scientific | 15.70 | 2,532.4 | $202.6 million | $405.2 million |

| keel infrastructure | 14.80 | 2,387.2 | $191 million | $382 million |

| total | 360.48 | 58,144.5 | $4.652 billion | $9.33 billion |

That division is the important part. Sectors no longer move at the same speed in one direction. For miners without large contract AI revenue streams, Bitcoin still appears to be the main driver of top-line performance as long as prices remain around current levels.

For some companies that already have large AI leases and cloud agreements, the revenue mix will start to look very different.

As a result, the market becomes dual-track. One track still relies primarily on Bitcoin price and network economics. The other is increasingly dependent on whether miners control premium power sites that can be turned into long-term computing revenue.

| company | Verified annual AI revenue | If the contract amount doubles |

|---|---|---|

| bit deer | $21 million | $42 million |

| Mara | $0 | $0 |

| clean spark | $0 | $0 |

| Airen | Not applicable from the disclosed annual occupancy rate | Not applicable |

| riot | $31.1 million | $62.2 million |

| Kango | $0 | $0 |

| hive | $15 million | $30 million |

| american bitcoin | $0 | $0 |

| core scientific | Not applicable from the disclosed annual occupancy rate | Not applicable |

| keel infrastructure | Not applicable from the disclosed annual occupancy rate | Not applicable |

| total | $67.1 million | $134.2 million |

The comparison becomes even clearer when we model Bitcoin at $160,000. At this level, mining revenues grow fast enough that even when annualized large AI contracts signed for comparison, the top 10 groups of Bitcoin businesses significantly outpace the current AI contract base. However, this does not mean that AI’s appeal will disappear.

This changes the relative urgency of the pivot. Rising Bitcoin prices give miners more room to justify their opportunity costs while keeping the best sites open for hashing. It also raises the bar that AI must clear before boards feel pressure to move away from Bitcoin and repurpose major campuses.

| scenario | annual revenue |

|---|---|

| Bitcoin earnings, BTC $80,000 | $4.652 billion |

| Bitcoin earnings, BTC $160,000 | $9.33 billion |

| AI Revenue, Verified Annual Uptime | $67.1 million |

| AI revenue doubles in confirmed contracts | $134.2 million |

| AI Revenue, 10 Year Sensitivity | $2.07 billion |

| AI revenue, 10-year sensitivity to doubling | $4.14 billion |

A more obvious sensitivity test is achieved by doubling the AI contract base.

Under that scenario, AI’s annual revenue would be significantly closer to what the group would earn from mining at a Bitcoin price of $80,000. That’s the zone where business models really seem to be contested.

Bitcoin still holds the larger total pool in the base case, but the gap narrows as site quality, contract length, funding terms, and execution begin to matter more than ideology. Once that happens, the debate will no longer be about whether miners “believe” in Bitcoin, but instead will shift to whose power usage will yield better returns in the coming years.

This is also where firm-level results matter more than sector averages. The aggregate numbers show that Bitcoin remains the stronger asset, especially in a high price environment.

Company-level numbers tell a different story. A small group of miners already has the potential for AI revenue that could exceed mining revenue at today’s Bitcoin price assumptions. These are names that lend credibility to broader threats.

They show that AI does not need to replace and rebuild the entire mining industry. All that is needed is enough premium capacity taken away from Bitcoin to change who mines, where mining occurs, and the proportion of public miner complexes that act like direct proxies for Bitcoin itself.

Taken together, the return calculations support a more accurate conclusion than either extreme.

Bitcoin mining still offers significant profit opportunities across the top 10 groups, and that advantage will grow even further if Bitcoin enters a significantly higher price regime.

AI still has a strong case on the best campuses, as the economics are still better for some carriers and its dominance will increase rapidly as contract values continue to grow.

The result will probably be a hybrid sector rather than a complete break, with some miners remaining Bitcoin-first and others becoming power and computing businesses that treat Bitcoin as a secondary workload.

| company | AI annual revenue, 10-year sensitivity | If the contract amount doubles |

|---|---|---|

| bit deer | $21 million | $42 million |

| Mara | $0 | $0 |

| clean spark | $0 | $0 |

| Airen | $970 million | $1.94 billion |

| riot | $31.1 million | $62.2 million |

| Kango | $0 | $0 |

| hive | $15 million | $30 million |

| american bitcoin | $0 | $0 |

| core scientific | $1.02 billion | $2.04 billion |

| keel infrastructure | $12.8 million | $25.6 million |

| total | $2.07 billion | $4.14 billion |

Why AI will reach Bitcoin’s security budget first

The clearest way to understand this comparison is to distinguish between engineering risk and economic risk. Quantum is an engineering risk to cryptography. AI is an economic risk to Bitcoin’s industrial security infrastructure.

It has been noted that in the future, the signature scheme will need to be upgraded and the protocol strengthened over time. The other is already changing where capital goes, where machinery is deployed, and which activities deserve optimal power on the grid.

As such, AI becomes a more pressing pressure point for Bitcoin’s security budget. Bitcoin remains secure because miners use real money to generate hashes and defend against block generation under known attack assumptions.

Difficulty adjustments continue to add blocks, but do not erase the underlying economy. Networks where the most connected industrial operators treat Bitcoin as a premium campus, low-value use case are slower and face more real problems.

The security layer can continue to function as the best sites, best interconnect rights, and most financially viable infrastructure migrates to AI tenants.

Over time, Bitcoin mining will be pushed towards cheaper, more interruptible, and often lower quality electricity. CoinShares says just that in its sector review, arguing that AI will likely drive Bitcoin mining towards more intermittent and cheaper power sources in the long term.

The scale of external demand helps explain why. The International Energy Agency says in its Energy and AI Outlook that global data center electricity consumption is projected to nearly double to about 945 TWh by 2030 in the base case.

This is a significant increase in power demand, making an already difficult site even more difficult to assemble. Land, interconnections, permitting, cooling design, and transmission access all take time. Bitcoin miners have spent years collecting exactly these materials.

AI now wants them, too, and AI customers often bring longer-term contracts, larger balance sheets, and smoother revenue visibility than mining can offer in a post-halving environment.

Quantum lacks short-term commercial appeal for Bitcoin mining fleets. It could someday force protocol migration and widespread wallet migration, and the prospects are serious.

However, Quantum does not currently offer miners a more profitable alternative for the same substation. AI does.

Quantum is not currently emerging as a tenant willing to sign up for hundreds of megawatts of critical IT load. AI does.

Quantum has not raised board-level discussions about removing miners from live sites this quarter. AI is already doing that.

How miners and networks will be reshaped in the next decade

A complete exodus from Bitcoin remains extremely unlikely as the network adapts and many miners continue to have one foot in both worlds for as long as the numbers warrant.

A more realistic path is a long winnowing process, with premium always-on campuses moving toward AI, while Bitcoin mining focuses on interruption-tolerant, flexible power environments where site economics are difficult to exploit for hyperscale AI tenants.

The results still result in significant changes for Bitcoin.

First, public miner shares will no longer be a direct substitute for Bitcoin itself. Investors who buy publicly traded miners often treat them as an amplified representation of the Bitcoin cycle. This relationship weakens as more of the company’s value comes from data center leasing, power monetization, and AI execution risk.

Second, the composition of Bitcoin’s industrial hash will change. While public miners may still be mining large amounts of Bitcoin, much of the marginal security spending may come from operators with cheaper power, smaller footprints, or lower-cost regions.

Third, Treasury behavior may change. As companies fund campus renovations, cooling systems, and increased density computing, Bitcoin on their balance sheets begins to look more like a source of funding than a sacred reserve. Riot’s previous decision to sell Bitcoin to fund the Rockdale land purchase provided a clear preview of that logic.

The biggest real variable is still Bitcoin price. If Bitcoin returns to its all-time high near $126,000, the hash price could rise towards $59 per daily petahash. Such a move would improve mining economics and delay the urgency of a pivot.

However, this will not erase the ongoing structural changes.

The demand for AI is fueling the creation of a global infrastructure that goes far beyond cryptocurrencies. The IEA demand curve, the signed large contracts already on the miners’ balance sheets, and the actual physical reuse of campuses are all pointing in the same direction.

Over the next 10 years, it may no longer be a question of whether miners will move away from Bitcoin completely. The sharper question is what parts of the mining stack remain worth devoting to Bitcoin once the AI is willing to pay more for the best land, the best power, and the best grid location.

Quantum remains on the list of strategic risks for Bitcoin.

AI is now included in the list of operational and financial risks.

As technology reaches scale, it can threaten your code. The other is already competing for the machines, megawatts, and talent to keep networks secure.

This is a threat that will be directly relevant to Bitcoin’s security budget in the coming years, and is already visibly rewriting miners’ business models.

(Tag translation) Bitcoin