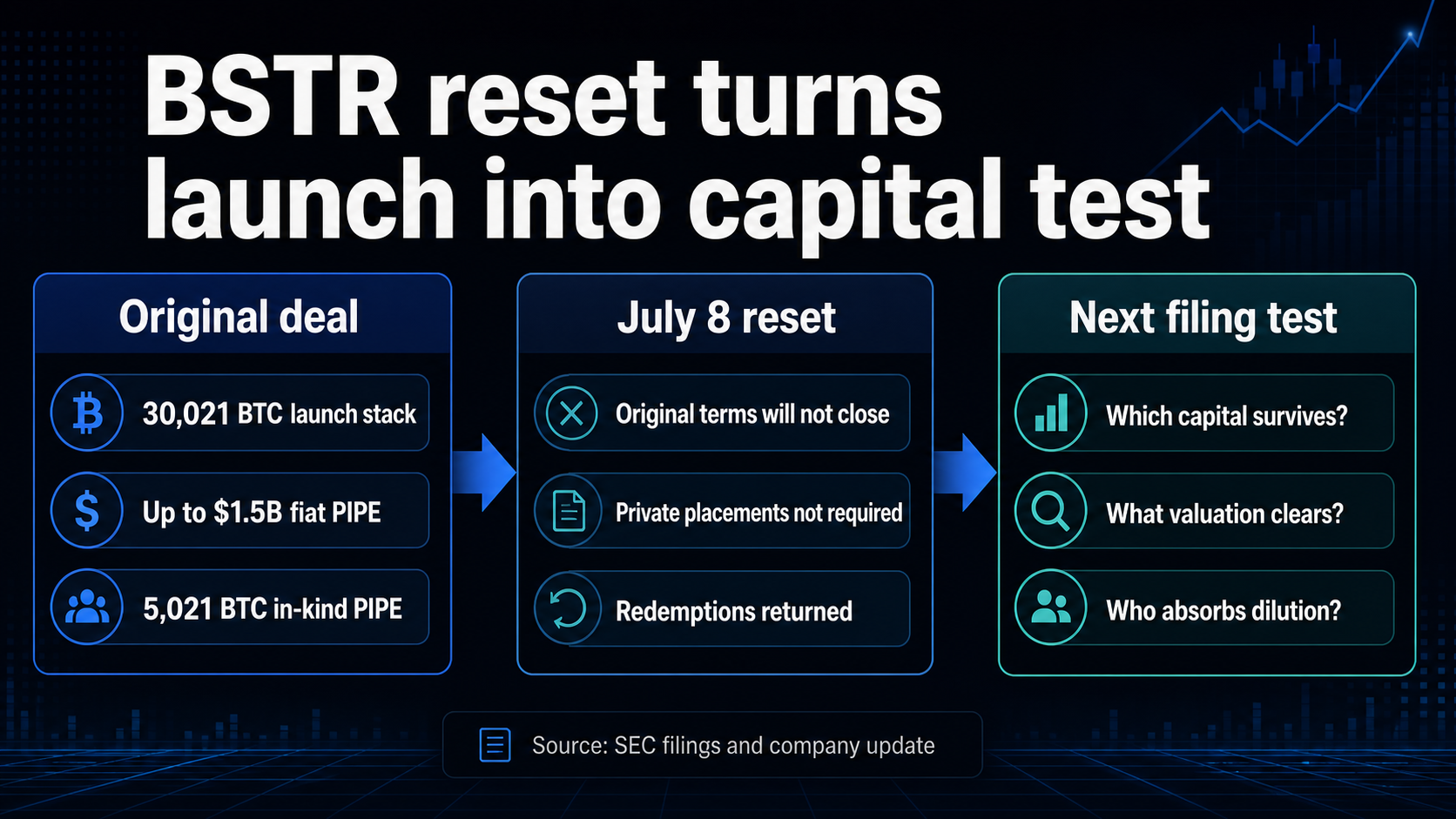

Kantar Equity Partners I and BSTR said they will not close Adam Back’s 30,021 BTC treasury transaction under the July 2025 contract.

One of the hottest Bitcoin government bond launchers on the market is currently stuck restructuring its funding before BSTR reaches retail investors.

Cantor Equity Partners I and BSTR said in their July 8 Form 8-K that they are discussing structural changes and modifications to the proposed business combination. The companies will not complete the transaction under the terms of the original agreement, and the pending private placement related to the transaction will not be required to complete, according to the filing.

In an accompanying update, the company said the revised structure and terms are intended to better reflect current market conditions. The same update said the general meeting of shareholders scheduled for July 10 will be postponed indefinitely, while public shares submitted for redemption will be returned and no redemptions will take place.

Funding reset is where Bitcoin Treasury trading meets reality. BSTR needs to prove that investors will fund the launch on viable terms before worrying about the performance of its stock.

Old trading was built around scale

BSTR’s original proposal was based on scale and access to funding. A company release filed with the SEC in July 2025 said BSTR will be created with 30,021 Bitcoin on its balance sheet, up to $1.5 billion in statutory PIPE funding, 5,021 Bitcoin in in-kind PIPE, 25,000 Bitcoin from founding shareholders, and up to approximately $200 million from Cantar Equity Partners I, subject to redemption.

The same release tied the vehicle to Adam Back, CEO of BSTR and co-founder of Blockstream. It also framed BSTR around a Bitcoin per share mandate, rather than just a passive holding company model.

The detailed business combination filing shows that the 30,021 BTC figure is made up of the following separate components: a 25,000 BTC seller contribution, a 4,156.11 BTC CEPO Bitcoin stock PIPE, and an 865 BTC Newco stock PIPE. The same filing also listed cash capital, convertible debt, preferred stock, and Bitcoin-denominated commitments that will be relied upon to complete the transaction.

These commitments have done the heavy lifting, turning the massive Bitcoin stack into a vehicle built for public market funding. The original structure combined a SPAC shareholder base with common stock, convertible debt, preferred stock, Bitcoin-funded subscriptions, and redemption rights across several investor groups.

Once the July 8 update announced that the existing private placement did not need to be closed, the question shifted from whether BSTR had announced sufficient capital to whether it could get that capital back on new terms.

This will also change the role of the postponed general meeting of shareholders. Postponing the vote itself would be a procedural matter. Returning shares submitted for redemption while the parties renegotiate has greater significance as the public shares, CEPO contributions and shareholder base remain unresolved. These variables are exactly what Bitcoin treasury companies need to iron out before they can definitely commit to expansion.

This structure has led BSTR to claim that it wants Bitcoin more than other companies. This was a test to see if Bitcoin Treasury promoters could combine stock market access, PIPE capital, physical Bitcoin commitments, and public shareholders into a single funding machine.

Now you need to rebuild or replace your old machine.

Reset gives investors back control

BSTR and Cantor are still negotiating, and the original terms are now off the table.

If the parties reach an amended agreement, it is expected that additional SEC filings will amend or supplement the registration statement and proxy materials. The next filing will show how much of the original transaction remains, including the Bitcoin stack, PIPE commitments, and the price investors are currently demanding to raise capital.

It will also show how much demand remains for digital asset treasury companies, even though Bitcoin’s arrival has not been easy.

igcurrencynews’s Bitcoin Markets page showed Bitcoin was trading around $63,688 on July 12, giving it a market capitalization of about $1.27 trillion and about 58% control of the broader cryptocurrency market. This backdrop is not catastrophic for Bitcoin, but it is very different from markets that treat financial vehicles as automatically rising.

igcurrencynews readers have already seen pressure points in other financial structures. Recent reports have focused on the economics of dilution and Bitcoin per share, Strategy’s preferred stock stress, and the broader point that the treasury company is actually funding the stack with a Bitcoin wrapper.

BSTR is raising the same questions along the way. Rather than asking whether the stock will trade at a premium after trading begins, Reset asks whether the premium assumption still funds the company before investors receive publicly traded stock.

The difference is important for companies measuring the success of Bitcoin per share. Capital reaching lower valuations with higher yield demands, greater dilution, or lower Bitcoin commitments could change the economic landscape, even if the deal is still done. Accordingly, the amended application will be construed more like a market clearing document than a relaunch notice.

Therefore, future conditions are more important than the brand of the vehicle. Investors do not have to reject Bitcoin for balance sheet exposure, redemption risk, or demanding a different price for future capital calls.

The next application is a test

A company’s own risk language indicates the variables that currently matter. The July 8 filing and release cited risks related to public shareholder redemptions, public equity, liquidity, exchange listings, Bitcoin price volatility, competition, regulatory uncertainty, and difficulty accumulating Bitcoin and expanding financial operations.

That is the condition for the next negotiation.

The digital asset treasury company’s deal will have a stronger answer if the revised BSTR contract can maintain the launch size of 30,021 BTC, maintain meaningful investor commitments, and avoid passing on excessive costs to new shareholders. It would show that the market can reprice large-scale Bitcoin Treasury transactions without breaking the model.

The message will change if the revised terms reduce the Bitcoin stack, increase the cost of capital, weaken investor protections, or tip the scale further toward dilution. This reset would suggest that the next wave of Bitcoin treasury companies cannot rely on the old premium from the previous cycle.

BSTR has become a live price check for all Bitcoin financial transactions. The revised terms will indicate whether investors still want to fund expansion or whether shareholders continue to pay for the reset.

(Tag Translation)Bitcoin