This article first appeared in Miner Weekly, BlocksBridge Consulting’s weekly newsletter with the latest energy news. Bitcoinand the AI is calculated from The Energy Mag. Subscribe to receive it in your inbox once a week.

Bitcoin Miners no longer need to talk only about hash prices, fleet efficiency, or the next difficulty adjustment. They could talk about campuses, lease terms, hyperscalers, neoclouds, inference workloads, and “critical IT loads.” The same substations that once powered racks of ASICs have been reintroduced to investors as a gateway for scarce energy to the artificial intelligence boom. In power-constrained markets, that story worked.

It worked so well that the new question of who got it begins to matter. liquidity While the story progresses?

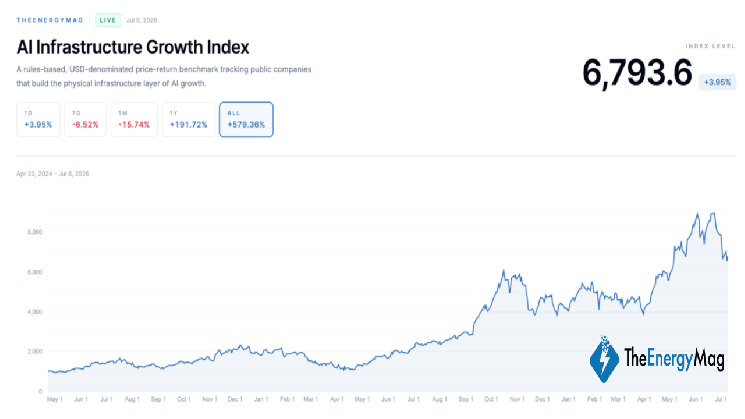

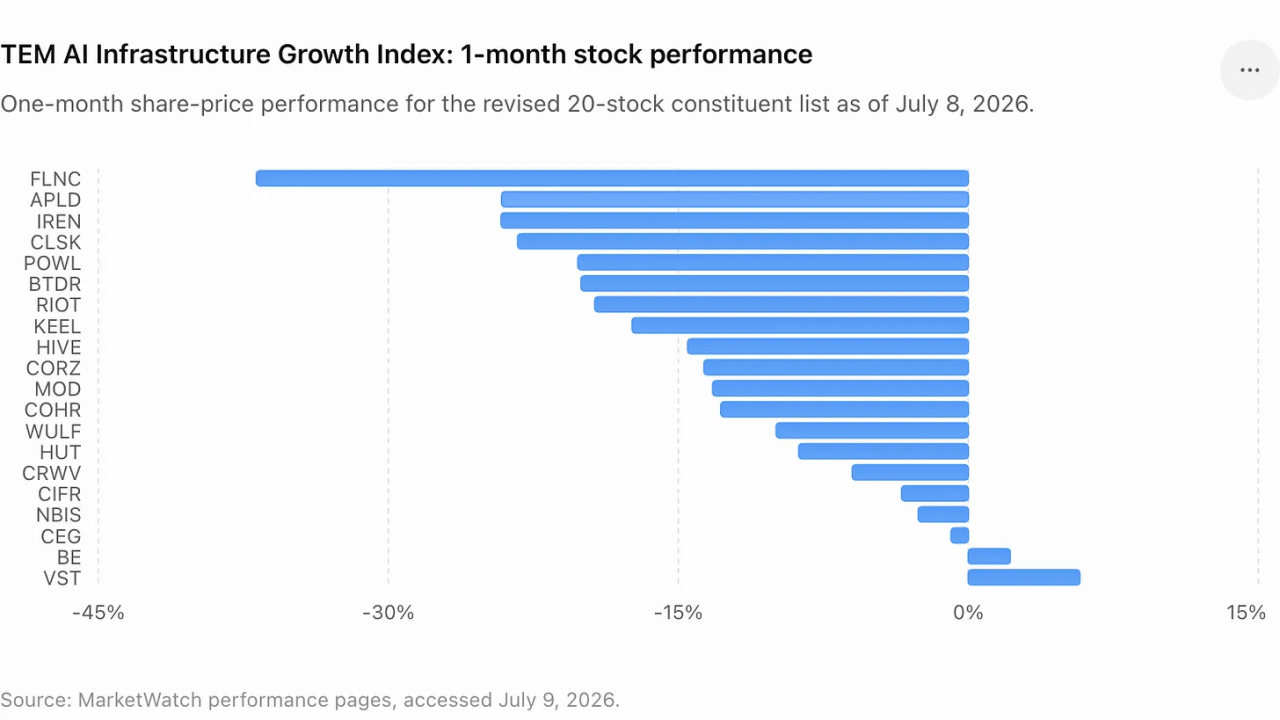

This question is moving to the forefront with the TEM AI Infrastructure Growth Index, a basket-tracking indicator. Bitcoin Miners, neoclouds, power providers, and other companies involved in the physical construction of AI infrastructure declined by 16% over the past month. This withdrawal does not erase the long-term debate for energy-enabled computing. Nor is it intended to suggest that recent insider sales or shareholder transactions were improper. Many of the transactions were disclosed as prearranged transactions under Rule 10b5-1 plans designed to allow insiders to sell stock according to preset instructions.

However, market views change rapidly. Sales planned during rallies may seem routine. The planned sell-off and subsequent sector-wide drawdown starts to look like this: liquidity window.

Recent tapes provided investors with some examples to understand. Core Scientific’s (NASDAQ: CORZ) general counsel sold his shares after news coverage of the company’s AI data centers helped boost the stock price. The CEO of Riot Platforms (NASDAQ:RIOT) revealed a pre-planned sale after the mining company’s stock price recovered. Tether has reduced its exposure to BitDia (NASDAQ: BTDR) after buying during the initial dip and selling during the recovery. TeraWulf (NASDAQ: WULF) has revealed a new stock sale by its chief, just ahead of the sector’s most significant AI lease announcement.

And in IREN, the controversy is not about insider sales, but about insider compensation. The company’s board approved more than 18 million restricted stock units for its co-founder and co-CEO, adding governance and dilution arguments to the stake, which has become one of the most visible winners in the miner-to-AI transformation.

Taken together, these episodes signal a shift in AI infrastructure transactions. Investors are no longer just asking which companies have the power. They are asking who knows the economics, who absorbs the dilution, who maintains the upside, and who monetizes the rerating before trading cools.

TeraWulf turns heads

TeraWulf remains one of the clearest AI infrastructure stories in the space, and therefore provides the most vivid case study.

On June 29, Beowulf E&D Holdings, managed by TeraWulf Chairman and Chief Executive Officer Paul Prager, announced the sale of 275,000 shares of TeraWulf stock at a weighted average price of $26.596 per share, generating gross proceeds of approximately $7.3 million. The sale comes a week before TeraWulf announced a 20-year AI infrastructure lease with Anthropic.

The June transaction was part of a wide range of sales disclosed by Prager and Beowulf E&D Holdings since late March. In total, Prager and the companies he controlled sold approximately 1.59 million shares of TeraWulf stock for gross proceeds of approximately $32.7 million. This means the weighted average selling price per share is approximately $20.55.

And on July 6, TeraWulf announced a 20-year lease agreement with Anthropic at the Justified Data campus in Hawesville, Kentucky. The lease is expected to generate approximately $19 billion in contracted revenue over the initial term and support approximately 401 MW of significant IT load. TeraWulf also agreed to sell a 50.1% interest in the Abernathy joint venture to a Fluidstack-led investor group, allowing it to monetize approximately $450 million worth of investment and redeploy the company’s capital to wholly owned AI infrastructure projects.

This is the kind of deal investors have been waiting to see from power-rich miners. Long-term AI customers, significant contract revenue, and the claim that traditional mining infrastructure can be upgraded to a higher multiplier asset base.

This is also a notable moment for insider liquidity.

Cipher, Riot, and Core Scientific show the same pattern

Cipher Digital (NASDAQ: CIFR) has added the latest example to its liquidity window theme.

On July 8, Cipher CEO Tyler Page filed to sell 112,500 shares of CIFR stock with a market value of approximately $2.38 million, implying an average price of $21.19. This sale was associated with a Rule 10b5-1 trading plan adopted on December 19, 2025. Cipher previously revealed that Page’s plans include the potential sale of up to 1.5 million shares by December 24, 2026. The 112,500 shares notified represented 7.5% of the total cap of 1.5 million shares under the plan.

Riot Platforms had its own version of the story. In May, CEO Jason Les sold 175,000 shares valued at approximately $4.2 million pursuant to a Rule 10b5-1 plan adopted in August 2025. On June 22nd, he sold another 250,000 shares for a market value of $7.03 million.

Core Scientific is another focus of AI and mining crossover deals. The company emerged from bankruptcy in 2024 and has since repositioned itself around high-density colocation and AI infrastructure, but continues to report declining self-mining revenues.

Todd Duchesne, Core Scientific’s chief legal and administrative officer, filed on July 6 to sell 140,000 shares at a market value of $3 million. This planned sale follows 12 dispositions of 10,000 shares since April 13, for a total disclosed sale price of approximately 260,000 shares under the plan and total proceeds of $5.9 million.

These are important notes. Rule 10b5-1 refers to pre-arranged trading plans designed to separate insider trading from subsequent corporate development, and sales by executives with significant stock holdings may reflect diversification, taxes, or personal liquidity rather than a negative view of the company. That’s not a confession of weakness. Executives with large stock compensation packages often sell, even if they remain optimistic about the company.

But open markets do more than just take care of legalities. Handle alignment. As stocks rise reflecting AI expectations, then management sells and sectors exit, investors begin to wonder if the balance of risk and reward has shifted from insiders to public float.

The theme of liquidity windows is not limited to C-suite executives.

Tether’s recent BitDeer trades show how strategic holders have taken advantage of the AI mining rebound to reduce their exposure. As reported by TheEnergyMag, Tether reduced its BitDeer position in early June at an average price of about $20, after acquiring the company for $8.85 per share during the market crash earlier this year. While Tether remains one of BitDeer’s largest shareholders, this deal still fits the pattern. This means buying on weakness, adjusting AI-related valuations, and maintaining a position large enough to stay involved if the story continues.

IREN adds governance layer

IREN focuses on another related issue.

The company has become one of the hottest names in AI infrastructure after pursuing large-scale AI cloud and data center opportunities beyond Bitcoin mining. However, the company’s latest compensation disclosure sparked a backlash among some retail investors and market commentators.

On June 30, IREN’s Board of Directors approved the granting of 9,099,328 restricted stock units to co-CEOs William Roberts and Daniel Roberts each. The award has a vesting and holding period of six years. The company said both co-CEOs will not receive any new equity incentive grants until fiscal year 2031, and the awards are intended to retain and encourage executives through IREN’s next phase of growth.

That explanation did not quiet the debate. Critics focused on the size of the package, its dilution, and the fact that the company is still proving that its AI infrastructure strategy can generate lasting benefits. IREN stock fell sharply following a broader selloff in AI stocks due to governance concerns.

The IREN episode is not about insider sales. Perhaps more important is the debate about how much upside AI infrastructure should be received by founders and executives before the business model is fully mature.

This is where AI infrastructure trading begins to resemble other capital-intensive booms. The first phase of the rise was related to shortages. The next stage is about governance, capital discipline and execution. At that stage, disclosed insider sales, strategic holder interest adjustments, and large founder equity subsidies become part of the same story. They tell investors where the private incentives lie amidst the public market boom.

This article first appeared in Miner Weekly, BlocksBridge Consulting’s weekly newsletter featuring the latest energy, Bitcoin, and AI computing news from The Energy Mag. Subscribe to receive it in your inbox once a week.