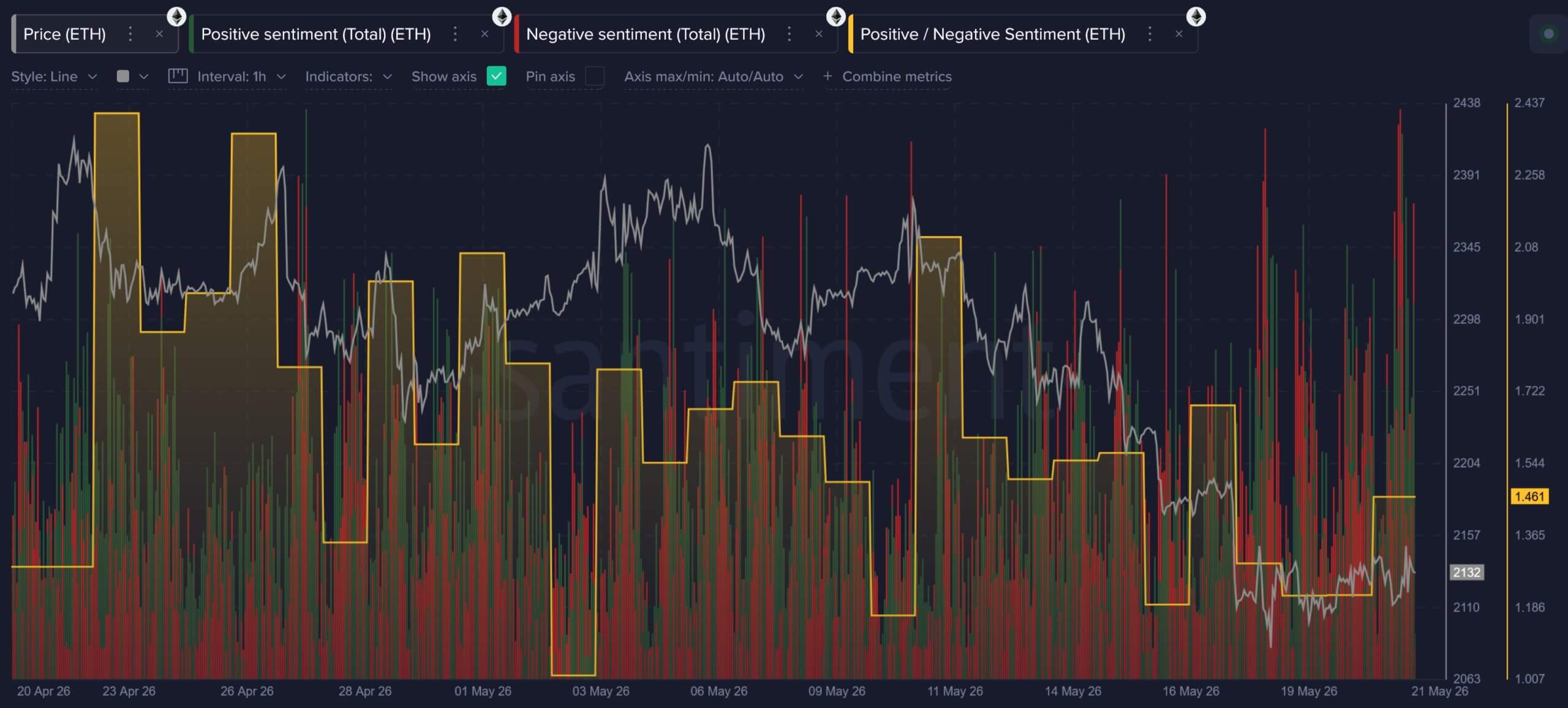

Ethereum market sentiment has deteriorated significantly as the blockchain network’s native ETH token enters a medium-term bearish phase.

According to data from blockchain analysis platform Santiment, the frequency of ETH-related discussions increased throughout May, but the tone of the commentary shifted toward frustration, disappointment, and concern about the possibility of a deeper downturn.

The firm’s analysts noted that this change in sentiment reflects a combination of concurrently increasing market pressures, including weak spot price movements, sustained exchange-traded fund (ETF) outflows, high-profile departures from the Ethereum Foundation, public criticism from longtime ecosystem supporters, and stronger price momentum across competing layer 1 networks such as Hyperliquid, Zcash, and Solana.

Extensive market data from CryptoQuant supports this institutional slowdown picture. The company’s spot market and fundamental indicators indicate severe structural weakness as ETH price declines towards the key support level of $2,000.

This spot weakness is most evident in Ethereum’s performance compared to the broader market. The ETH/BTC ratio recently fell to around 0.02758, its lowest level in nearly 10 months, indicating that Ethereum is lagging behind Bitcoin amid the current market downturn.

This created a fragmented market identity in which spot investors steadily reduced their exposure, the market became less liquid, and institutional buying pressure from large trading desks all but disappeared.

Spot sales end Ethereum without permanent bids

Indeed, CryptoQuant’s money tracking data highlights the extent of contraction in institutional bids over the past two quarters.

According to the company, the fund’s total holdings, which peaked at over 7 million ETH in October 2025, have steadily declined to a range of around 5.5 million ETH.

This sustained unwinding indicates that large allocators have systematically reduced their core exposure through the current multi-month drawdown.

Notably, the regulated ETF market is reinforcing this structural pressure. Total assets under management across Ethereum ETFs now stand at nearly $12.14 billion, down 23% from its peak in January.

May was particularly tough, with two consecutive weeks of net outflows totaling around $470 million, making it one of the year’s biggest episodes of concentrated capital flight, according to SoSoValue data.

This institutional withdrawal is further illustrated by the Coinbase Premium Index, which tracks the price differential between Coinbase Pro and major offshore platforms.

The index remained negative throughout May, indicating the absence of spot demand from US institutional investors.

At the same time, with this decrease in capital reserves, the liquidity of ETH also decreased.

According to CryptoQuant, daily fund trading volume has been on a downward trend since February 2026 and remains well below the recent one-year moving average range of $17 million to $42 million.

This compression in volume suggests that the appetite for spot buying has waned and the spot market, where assets are more exposed to spikes in volatility during periods of negative news, has become thinner.

ETH options traders hedge as leveraged longs continue

Behind the scenes of spot market liquidations, derivatives data reveals that the debate continues over whether ETH is entering a structural decline or forming the basis for a leveraged pullback.

This disconnect has fragmented the derivatives market, with speculative perpetual futures traders holding long positions while professional traders actively hedge against downside risk.

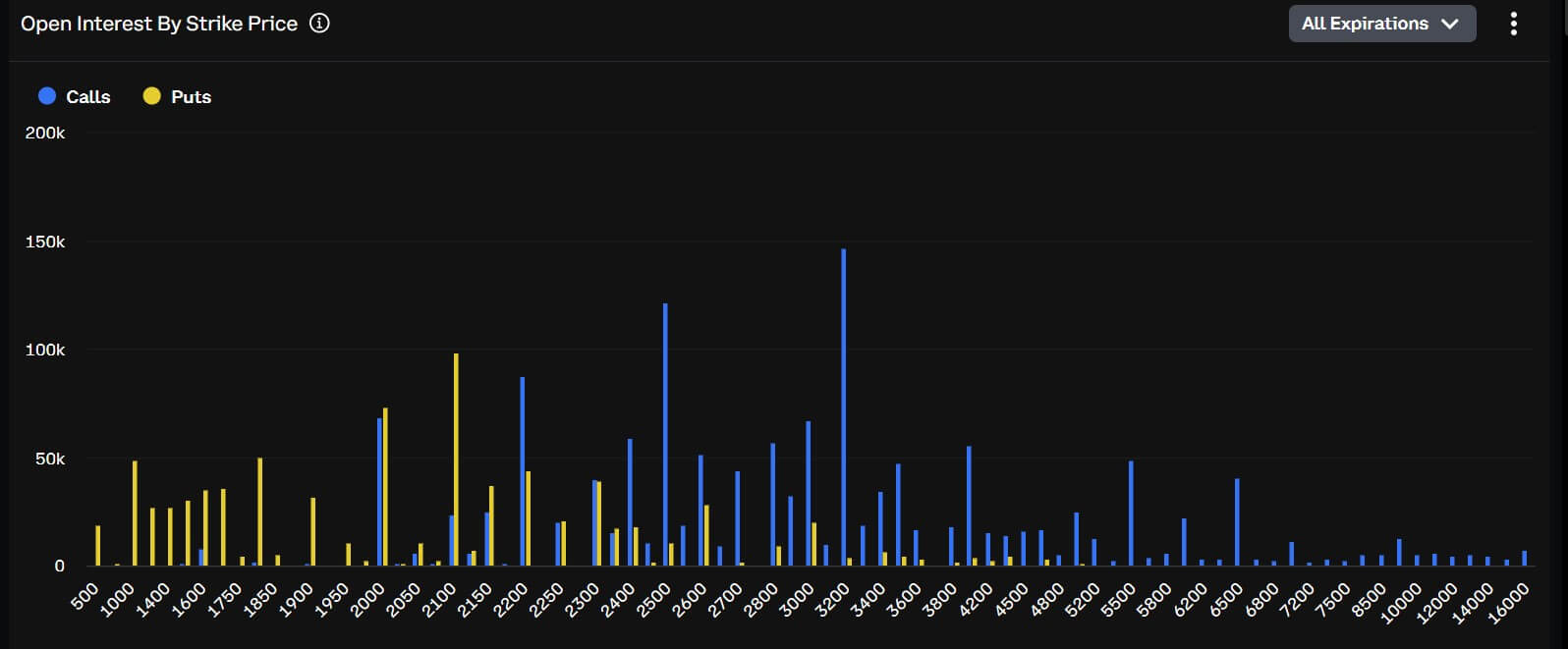

ETH’s seven-day 25-delta risk reversal skew is trading close to 7%, according to Brock-Scholes data, indicating that options market participants are paying a premium for downside put protection.

This defensive posture is supported by the erasure of data from Deribit exchanges, where there is a concentration of over $380 million in open interest in put options with strike prices of $2,100 and $2,000, making these technical areas central to the short-term institutional position.

Market Note: This intensive options trading reflects the market bracing for an extended period of weakness. Already below the $2,100 support shelf, the Brock-Scholes Risk Appetite Index shows slowing momentum, leaving assets reliant on defensive hedging in the absence of spot accumulation.

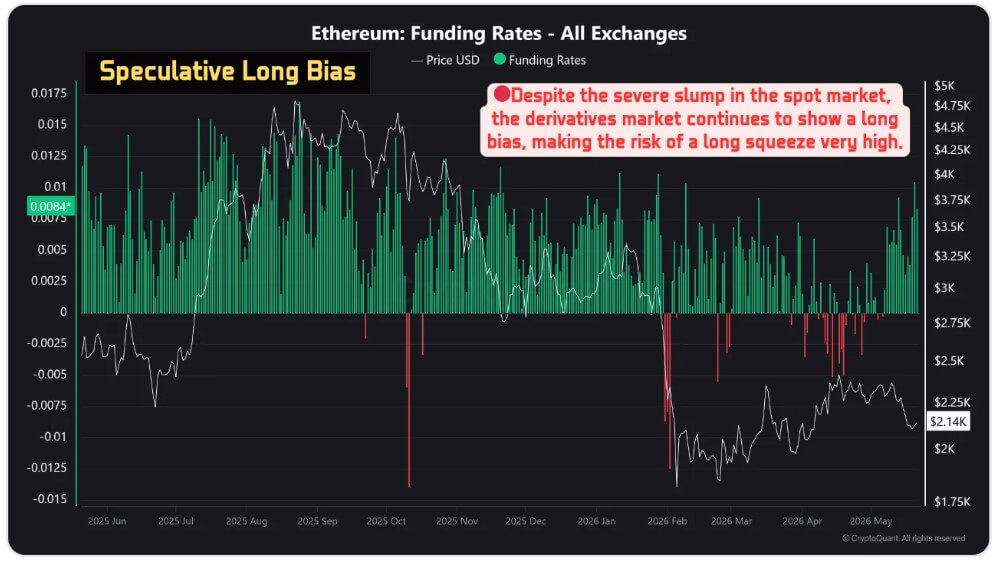

At the same time, the perpetual futures market sends a more mixed signal. CryptoQuant data shows that Ethereum derivative funding rates are firmly entrenched in positive territory, reaching 0.0082 on May 21, 2026.

This positive ratio indicates that the speculative long bias has not completely broken down despite the decline in market capitalization, fund holdings, and spot trading volume.

The resulting divided identity creates a delicate technological backdrop. While options traders are positioning for a breakdown, perpetual futures traders continue to hold leveraged long exposures.

This structural discontinuity could facilitate a rapid short squeeze if spot demand returns unexpectedly, but it also significantly increases the risk of cascading liquidations if spot prices break through heavy open interest concentrated at the $2,000 floor.

Ethereum Foundation’s withdrawal collides with ETH value decline theory

Ethereum’s financial slump coincides with an accelerating departure of senior personnel from the Ethereum Foundation (EF), the Swiss nonprofit organization that manages the blockchain’s core development.

The internal turmoil intensified after research veterans Karl Beek and Julian Ma officially resigned. Beek focused on Beacon Chain’s design for seven years, and Ma created the network’s Incentivized Laboratory Transfer Oversight Committee (FOCIL) framework.

Their retirements bring the total of senior retirements or withdrawals since February to at least nine, with five landing in May alone.

The list includes former co-executive director Tomasz Stańczak, board co-executive director Josh Stark, Protocol Guild contributor Trent Van Epps, and protocol cluster leaders Barnabé Monnot and Tim Beiko.

Additionally, Senior Research Scientist Alex Stokes recently began a three-month sabbatical, further diluting the organization’s visible technical leadership during a period of severe market stress.

Ecosystem analysts trace this management shift back to the foundation’s “mandate” document issued in mid-March.

The 38-page framework codifies the Foundation’s commitment to the CROPS principles of censorship resistance, open source deployment, privacy, and base layer security.

Importantly, this document positions the Foundation as a steward of the ecosystem rather than a company, and clearly states that its purpose is to protect network neutrality, rather than maximizing token prices, optimizing investor returns, or actively coordinating commercial expansion.

As alternative networks gain speculative market share, this neutrality-first stance is becoming increasingly difficult for some segments of the market to accept.

Tommy Shaughnessy, co-founder of Delphi Ventures, said the departures are more serious than they appear, adding that with the departure of reform-minded staff, there are fewer internal voices challenging the foundation’s structural direction.

Reform calls for testing Ethereum’s neutrality-first model

Several prominent former insiders have called for structural governance reforms due to a perceived lack of commercial enforcement by the Foundation.

Prominent researcher Danclad Feist, who left the foundation last year to join the Stripe-backed Layer 1 network Tempo, has publicly advocated for the creation of an entirely separate entity to protect the network’s economic relevance.

Feist proposed creating an independent alternative entity backed by at least $1 billion in capital, partially funded by network staking proceeds. This proposed entity would be directly accountable to token holders and have a clear mandate to drive the financial adoption and market value of ETH.

Feist emphasized that the current foundation controls less than 0.1% of the total ETH supply in circulation and receives no direct inflows from base layer staking yields or network transaction fees.

He said this will leave the ecosystem without nimble institutions to promote assets in the capital markets.

Bankless co-founder Ryan Sean Adams supported this view, stating that the future of Ethereum does not depend solely on foundations.

Mr. Adams argued that the ecosystem requires competitive, well-capitalized institutions that specialize in capital efficiency, proactive communication, and commercial enforcement. These are roles that Foundations were not structurally designed to play.

The consensus among these reform proposals is not to replace foundations, but to establish a dual agency model, one to protect foundational neutrality and public goods, and the other to promote assets and compete for institutional capital.

This push for reform has drawn a direct reaction from Ethereum bulls, who argue that the market is overreacting to short-term price fluctuations and natural organizational transitions.

ETH investor member Ryan Berkmans characterized the talent turnover as a healthy handover to a younger generation of developers.

Berkmans argued that Ethereum has successfully weathered previous regulatory pressures and leadership changes while still offering major upgrades such as merges, blob transactions, and a dominant position in on-chain application capital.

He noted that the growing deployment of stablecoins and tokenized assets by global companies continues to support the network’s long-term trajectory.

This perspective is shared by substantial institutional holders.

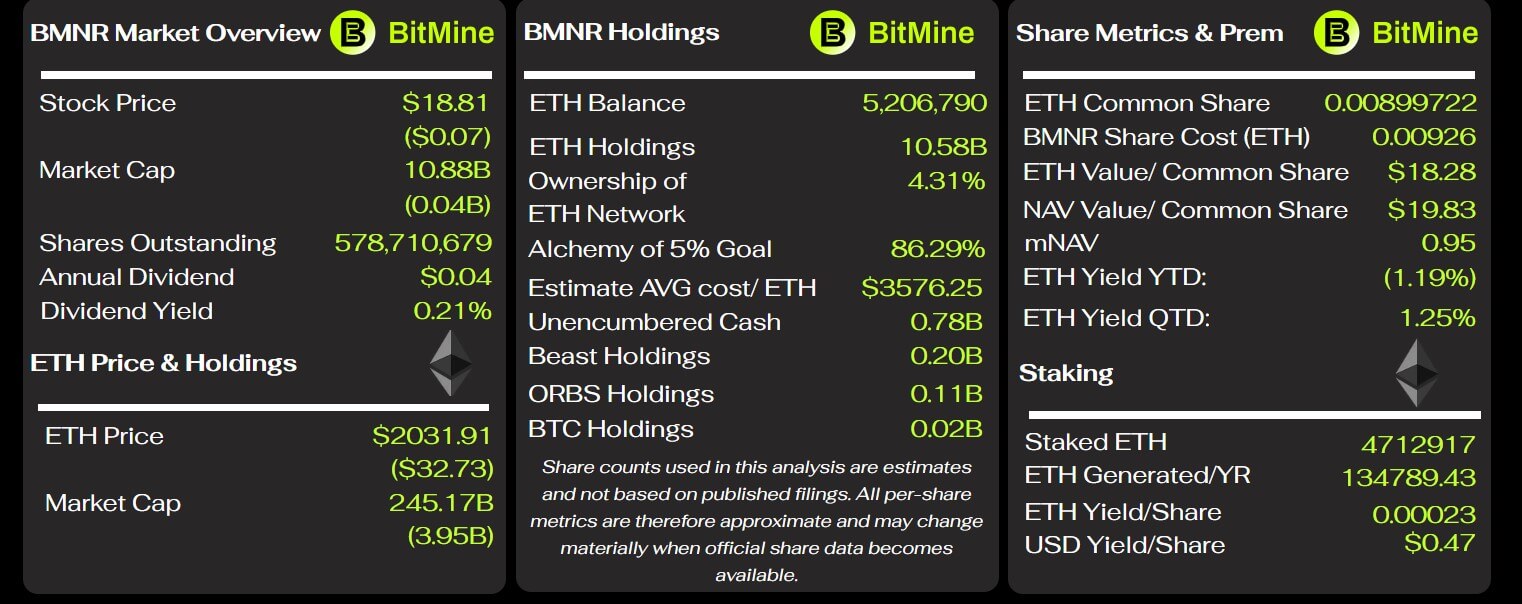

BitMine Chairman Thomas Lee dismissed the current market jitters as a typical cyclical capitulation. BitMine is the largest publicly traded holder of ETH, with a portfolio of 5.2 million ETH and over $10 billion in active tokens.

Lee argued that blockchain infrastructure represents a fundamental payments highway for agent-based artificial intelligence commerce and institutional finance, and that Ethereum is positioned to maintain a clear structural advantage due to its established security record, deep liquidity, and familiarity with institutions.

How Ethereum recovers from current FUD

Market observers note that Ethereum’s near-term trajectory now depends on whether its technological roadmap and commercial moat lead to a coherent investment thesis for ETH.

Galaxy Digital’s strategic analysis shows that the network needs to execute a disciplined operational plan to reverse the ongoing capital flight.

According to Galaxy’s recovery framework, the immediate focus must be on getting the Gramsterdam upgrade shipped, the subsequent deployment of Hegota on track, clarifying management responsibilities within the Foundation, and focusing resources on core commercial areas.

These key areas include high-value decentralized finance, institutional asset issuance, tokenized RWA, stablecoin payments, and privacy-preserving financial infrastructure. These are areas where Ethereum’s trusted neutrality and security record serve as a commercial necessity rather than an abstract principle.

Galaxy also pointed to the need for Ethereum to more quickly address the narratives that will likely define the next cycle, including layer 1 scaling, on-chain privacy, post-quantum security, and AI-native economic infrastructure.

A large part of this technical architecture is Although documented in the open source Strawmap development framework, a more complex challenge is the coordination between them. commercial and institutional actors;

This adjustment gap is at the heart of Ethereum’s current market friction.

Although the Foundation’s mission articulates base-layer engineering principles, it does not provide the capital markets with simple answers about value generation, nor does it create an organization designed to protect assets from aggressive layer 1 competitors.

As a result, the current drawdown has evolved into more than just a price correction. This is an active test of whether a decentralized structure can distribute commercial responsibilities to new institutions without losing operational consistency.

If the ecosystem can transform the current administrative chaos into clearly defined roles and technical roadmaps into concise asset cases, this period of underperformance could serve as a needed governance reset.

However, if it is unable to do so, the market may continue to treat weak spot demand, senior defections, and economic changes in the application layer as evidence that Ethereum’s network strength no longer guarantees protection of the value of the underlying tokens.

(Tag translation) Featured