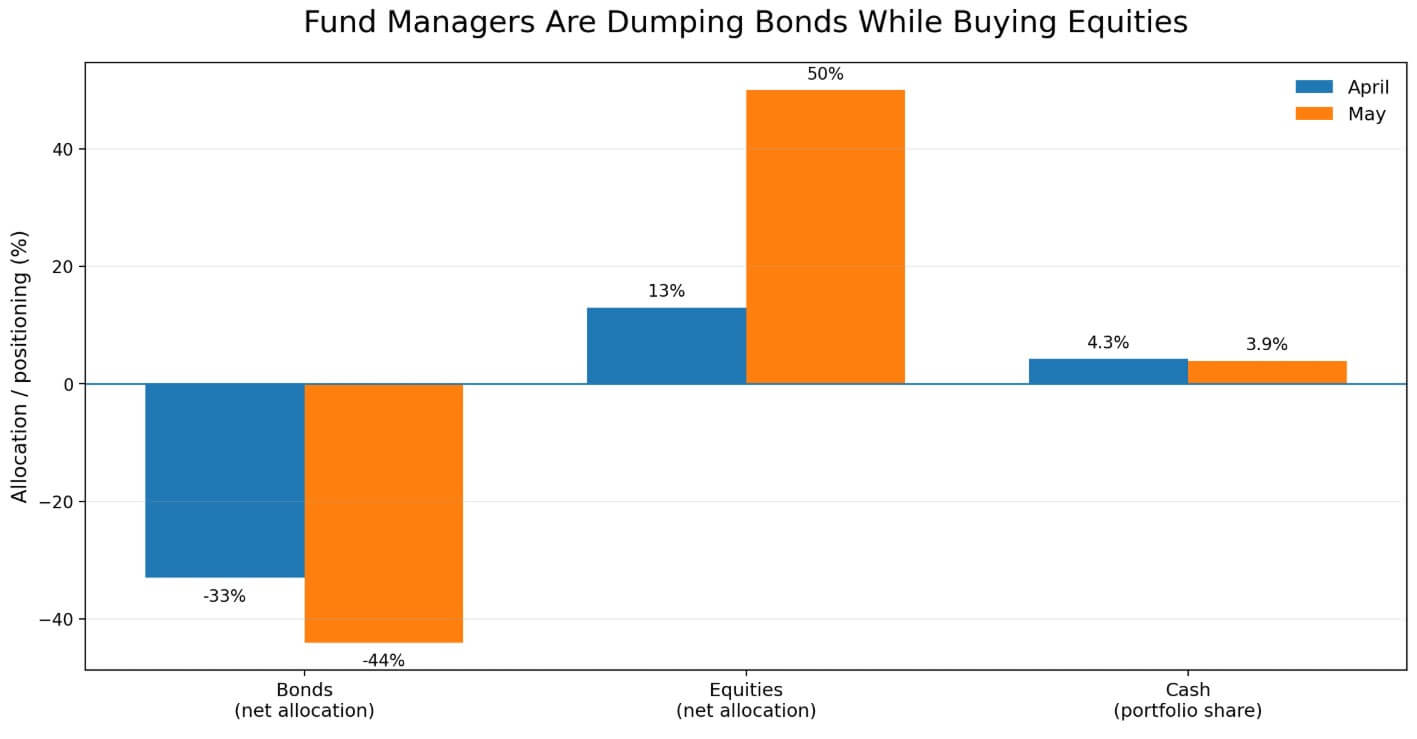

Bitcoin ETF outflows make rising US Treasury yields a direct test for BTC prices after Bank of America’s May Global Fund Manager Survey showed professional investors reduced their bond allocations to a net 44% underweight, the deepest positioning since June 2022 and down from 33% underweight in April.

At the same time, management increased global equity exposure to a net 50% overweight from 13% in April, while cash fell to 3.9% from 4.3%. Fund managers are rejecting duration and turning to risk, at the fastest pace in nearly four years.

In the case of Bitcoin, this combination creates a non-negligible problem for the asset, with 40% of managers surveyed citing second-wave inflation as their biggest tail risk, and 18% citing a chaotic rise in bond yields.

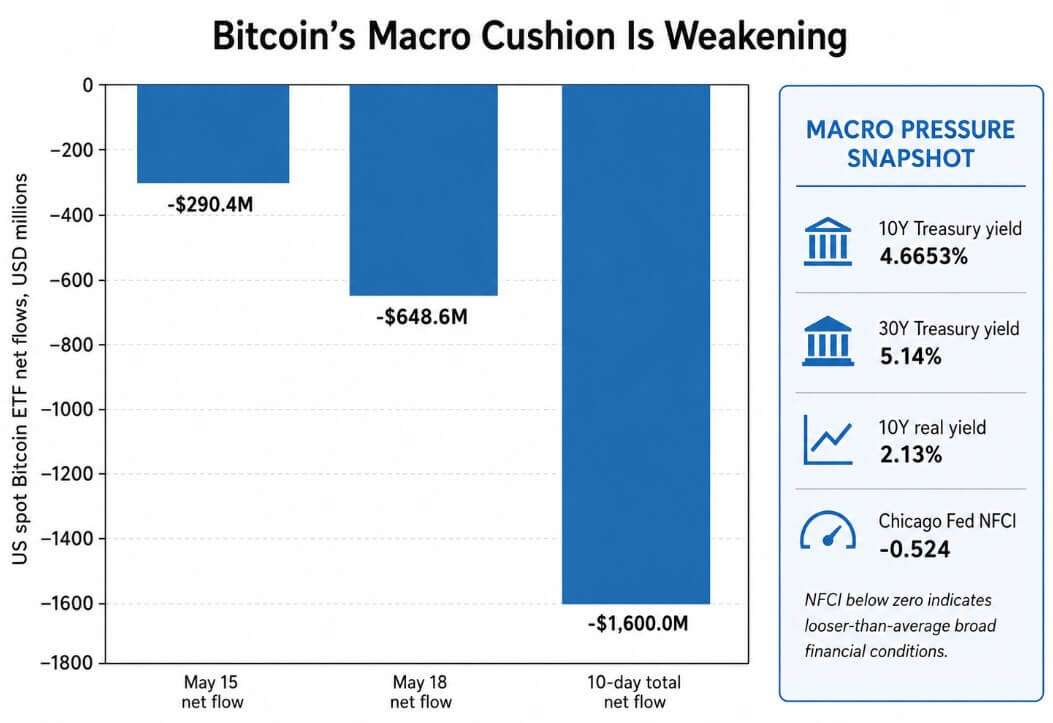

The yield on the 10-year US Treasury note reached 4.6653% on May 19, the highest level since January 2025, and the 30-year Treasury note reached 5.14%, with the 10-year real yield rising to 2.13%. Real yield repricing raises the hurdle rate for all non-yielding assets, but Bitcoin yields nothing.

Anti-duration trading is currently crowded

With a net underweight of 44%, anti-bond positions have been the dominant consensus trade in recent BofA research, making the next move in the Treasury market disproportionately important to risk assets.

As yields rise, duration is repriced, borrowing conditions tighten, and capital either seeks safety or withdraws from risk. Bitcoin, a 24/7 liquid asset with no contractual cash flows, tends to absorb selling before illiquid positions are reduced.

This explains why Bitcoin is trading around $77,000, close to the $75,000-78,000 support area that has absorbed macro-driven selling several times this cycle.

The Spot Bitcoin ETF was supposed to insulate BTC from these macro flows by locking in institutional demand. The US Bitcoin Spot ETF recorded net outflows of $648.6 million on May 18th, on top of the $290.4 million outflows recorded on May 15th, according to data from Pharcyde Investors.

These Bitcoin ETF outflows brought the 10-day total to -$1.6 billion. Although institutional bidding exists, it cannot counteract yield shocks in real time.

The Chicago Fed’s National Financial Conditions Index for the week ending May 8th stood at -0.524, indicating that overall financial conditions were more moderate than the historical average.

While the government bond market is tightening critical conditions for risky assets like Bitcoin, the broader system remains well above stress thresholds.

hedge or victim

In the long run, Bitcoin benefits from a framework in which government debt is structurally unsound due to its fixed supply, no central issuer, and no set maturity schedule.

The IMF’s April 2026 Global Financial Stability Report identified Middle East conflict, inflation, and core sovereign market rollover risks as threats to global financial stability.

The OECD’s 2026 World Debt Report said price-sensitive investors are holding more government bonds as central banks retreat, with foreign investors controlling 28% of global government bond holdings and hedge funds becoming more important marginal buyers in some core markets.

The Bank of Canada characterized the same situation in which long-term yields remain high as investors demand higher fees to absorb large bond issuances as a term premium problem.

Together, these structural forces create a long-term case for Bitcoin as a hedge of sovereign debt.

In the short term, Bitcoin will be a casualty of the chaotic spike in yields. When government bond markets move quickly, investors cut their most liquid positions first, and Bitcoin is at the top of that list.

Two potential paths

The anti-duration trade could quickly reverse if inflation data turns unexpectedly downside or the price of Fed rate hikes wears off.

The consensus net 44% underweight position in bonds comes with its own vulnerabilities, as a single failure of inflation could trigger a sharp unwind. If the 10-year bond yield declines towards 4.20%-4.40% and the 30-year bond yield returns below 5%, the financial situation for risk assets will ease.

ETF inflows resume, the $80,000-$82,000 resistance zone is broken, and strong demand from end investors anchors the Citi Bank bull market at $165,000, bringing Citi’s 12-month Bitcoin baseline forecast of $112,000 back into view.

Lower real yields reduce the opportunity cost of holding non-yielding assets, easing borrowing conditions for leveraged buyers and restoring risk appetite. Historically, Bitcoin has quickly regained ground when these three conditions are met.

Crowded anti-bond trades amplify the potential for a reversal, as all fund managers exiting underweight bond positions also ease the macro headwinds that have been suppressing BTC.

| scenario | financial triggers | market mechanism | Impact on ETF flows | Bitcoin levels to watch | Impact on BTC |

|---|---|---|---|---|---|

| Yield relief/bullish line | 10-year yield declines towards 4.20%~4.40%; 30Y slides under 5% | Anti-duration trading will be relaxed. Real yields will fall. Liquidity conditions for non-yielding assets eased | Spot BTC ETF inflows resume as macro pressures ease | BTC break $80,000 – $82,000 resistance | city’s $112,000 The base case comes back into view. bull case near me $165,000 If demand from end investors increases |

| Yield spike/bearish trajectory | Breaking through the 10-year yield 4.73%; 10-year real yield exceeded 2.13%; 30Y extends upwards 5.14% | The financial situation is becoming tight due to the decline in duration. Investors first reduce liquidity risk | ETF outflows accelerate, pressure increases due to long positions | bitcoin loses $75,000 – $78,000 support | BTC trades as a loss of liquidity. Downside of Citi’s recession $58,000 Become a major risk anchor |

If the 10-year Treasury yield breaks above the technical level near 4.73% and continues to rise due to persistent inflation, weak government bond auctions, and geopolitical escalation, Bitcoin’s position near the $75,000 to $78,000 support will become unsustainable.

With real yields above 2.13%, it becomes difficult to justify the opportunity cost of holding Bitcoin at yields comparable to historical equity risk premiums compared to sovereign-guaranteed government bonds.

ETF outflows will accelerate, leveraged long positions will face margin calls, and BTC will trade as the most liquid risk asset in the deleveraging cycle.

The macro downside for Bitcoin due to Citi’s recession is $58,000, and getting there from current levels would require a chaotic yield environment that forces deleveraging across multiple asset classes simultaneously.

According to the BofA survey, 18% of fund managers already cite unregulated rises in yields as their biggest tail risk, and the 30-year Treasury yield of 5.14% is close to levels that have historically driven widespread volatility in financial markets.

What the Bitcoin ETF outflow actually suggests

Bitcoin’s macro risk is currently dependent on the pace at which the US Treasury market tightens financial conditions compared to what ETF demand and risk appetite can absorb.

BofA’s research shows that financial institutions are saving money and converting it into equity while maintaining a cash reduction period. This rotation exposes Bitcoin to the same yield dynamics that compress all other non-yielding assets, with the added vulnerability of operating in a 24/7 liquid market where macro sellers can exit at any time.

If yields peak and the trade unwinds, the reversal could be rapid and the recovery from current support levels could be significant.

Until US Treasury yields stabilize, Bitcoin ETF outflows will put BTC at the worst consensus macro trading disadvantage in the last four years.

(Tag translation) Bitcoin