Bitcoin briefly regained the psychological level of $80,000 for the first time since February in early Asian trading on May 4, amid a quiet upward march in recent weeks.

data from crypto slate After reaching an intraday high of $80,529, the top cryptocurrency was shown falling towards $79,621 at the time of writing.

However, what looks like a winning milestone on the price chart hides a deeply contradictory market structure inside.

This is because a major cryptocurrency returning to this threshold is more of a high-stakes test than a clean bullish breakout.

However, market analysts pointed out that: $BTC Traders are now trying to determine whether a rebound in institutional spot demand can overcome a still hostile macroeconomic environment marked by tensions in the Middle East, a hawkish Federal Reserve return, and a derivatives market that remains deeply skeptical.

Aggressive but vulnerable breakout attempts

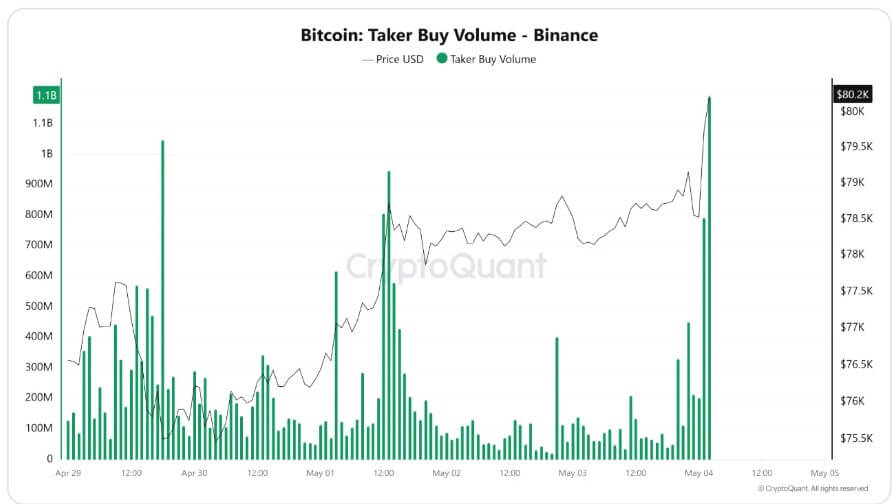

Bitcoin’s initial rise above $80,000 was marked by pure momentum rather than organic accumulation.

According to data from CryptoQuant, the activity was concentrated on major offshore platforms, particularly Binance, where taker-buy volume, an indicator that indicates traders cross the spread and immediately execute at market price, has surged.

According to CryptoQuant, $BTC The exchange saw two consecutive spikes of about $1.19 billion and $792 million, resulting in a buy volume of $1.98 billion within two hours.

When this level of aggressive buying materializes in a major resistance zone, it usually indicates that momentum traders are not waiting for a conservative pullback. Instead, they are actively chasing breakout confirmation.

However, market structure analysts warn that this type of trading volume creates immediate vulnerabilities.

CryptoQuant analyst JA Martun pointed out that the asset is currently facing a real test and stressed that if the rally is real, the price should not stay in this zone for long.

According to Maartung, Bitcoin needs to remain above $79,000 on a closing price basis to maintain structural strength. If it loses that level, he argues, the weekend rally was likely just a liquidity grab to clear out lagging short sellers.

Derivatives boost movement, but structural differences are exposed

The derivatives situation further complicates the story, revealing that markets are grappling with a wide disconnect between spot sentiment and leveraged positioning.

There are a plethora of call options targeting upside strikes, with a notional value of $1.7 billion pegged in $80,000 call options, along with large clusters at $90,000 and $100,000, according to Deribit data, and underlying sentiment indicators paint a picture of growing anxiety.

The market is not in a wave of bearish short selling, with cash confidence cooling sharply while leverage remains stubbornly long.

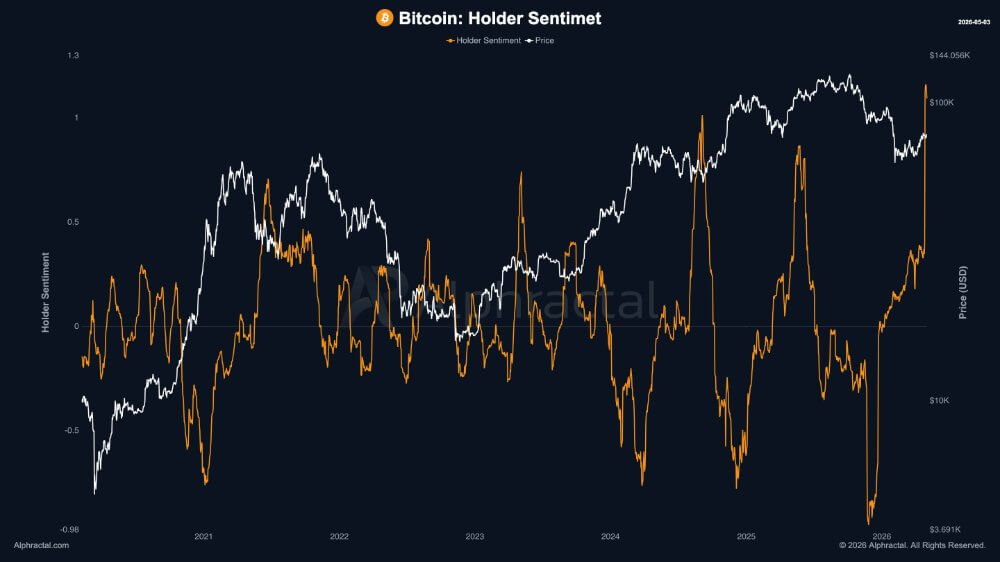

Bitcoin sentiment has dramatically reversed in less than a week, with the Fear and Greed Index dropping 10 points to a “fear” level of 43, according to data from analytics firm AlFaraktal.

But despite these spot-driven fears, futures traders are refusing to back down. Perpetual forward funding rates remain clearly positive, currently at +0.51%, according to Alfaractal data. This shows that while holder sentiment has cooled, speculative traders are still paying a premium to maintain their bullish bets.

This fear dynamic and skewed leverage over time in the spot market is critical to understanding current price movements. Historically, this particular divergence indicates a volatile “stress phase” for the asset.

As a result, the short-term push above $80,000 appears to have been driven primarily by leverage-sensitive traders rather than a clean fundamental macro reset.

While the market continues to rise, the heavy reliance on derivatives leaves the structure top-heavy, making it highly vulnerable to violent long-term liquidations if macroeconomic trends suddenly deteriorate.

ETF demand suggests durable spot bidding

Where derivatives offer volatile volatility, US spot ETFs offer the best crypto structural bottoms.

The US-listed Spot Bitcoin ETF has now recorded two consecutive months of net inflows, totaling $3.29 billion in investor funds, according to SoSoValue data. This follows the outflows that dominated the past four months.

Notably, it was the first consecutive inflow since September and October of last year, when the fund attracted nearly $7 billion in new capital.

Bitcoin economics platform Ecoinometrics said the current numbers “demonstrate high demand[for Bitcoin].” $BTC) is starting to take hold. ” He goes on to say:

“Over the past few weeks, Bitcoin ETFs have recorded nine consecutive days of net inflows, the longest period of consistent demand we have seen throughout this bear market.The last inflow was in October 2025, right around the time Bitcoin was hitting all-time highs.Then the demand disappeared and the market reversed.What is different now is not the size of the inflows, but their persistence.”

Given the above, this persistence is quietly changing the underlying architecture of the market as genuine spot demand gradually absorbs the volatility generated by the futures market.

Additionally, CryptoQuant data pointed out that the average cost base of early institutional ETF buyers currently serves as a formidable technical support level for top cryptocurrencies.

Macro risk casts a shadow on rebound

Even though the microstructure of the crypto market is improving, broader macroeconomic realities argue against open-ended beliefs.

The geopolitical situation in the Middle East remains tense. Although the ceasefire temporarily halted full hostilities, underlying tensions continue to actively drive global risk appetite.

Iran recently issued a stern warning to the US military to stay away from the Strait of Hormuz, the world’s shipping artery, even after President Donald Trump said the US would intervene to help the stranded merchant ship.

This geopolitical friction has pushed oil prices well above $100 per barrel, posing a major headwind to global disinflation efforts.

Meanwhile, the persistence of energy-driven inflation is forcing a rapid recalculation of US monetary policy.

Rather than a dovish reversal, the Fed faces pressure to abandon its easing bias altogether. As a result, major financial institutions are adjusting their models accordingly. Barclays recently revised its forecast to see zero rate cuts for the entirety of 2026.

Compounding this uncertainty is the impending change in central bank leadership. Chairman Jerome Powell’s term expires on May 15th, and his successor, Kevin Warsh, has been cleared by committee with a full Senate vote scheduled for the week of May 11th.

Warsh’s arrival introduces a new variable in the pricing of risk assets, and institutional investors remain hesitant to commit large amounts of capital without knowing exactly how the new chairman will navigate tensions between persistently high inflation and an increasingly burdened economy.