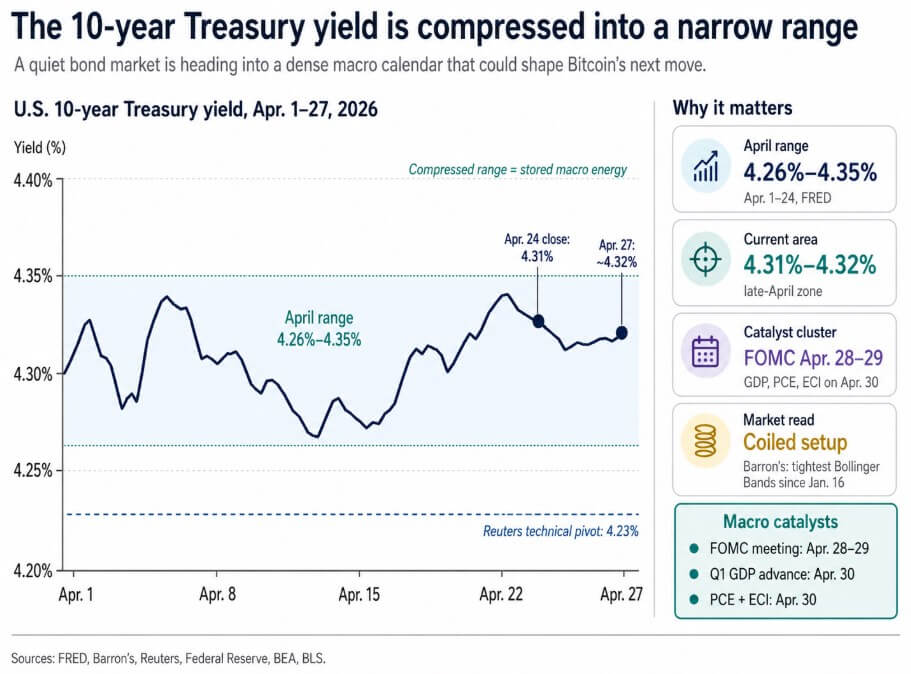

While everyone watching Bitcoin this week has their eyes on the Federal Reserve, the more important deciding factor may be the U.S. Treasury market. Just as a congested macro calendar begins, 10-year Treasury yields have compressed into one of the tightest ranges this year.

Bitcoin’s recovery currently relies on new capital inflows from institutional investors and the assumption that liquidity conditions do not tighten again. If U.S. Treasuries choose a direction before that assumption is tested, the bond market could drive Bitcoin’s next move independent of any crypto-specific catalysts.

According to FRED data, the 10-year Treasury yield ranged between 4.26% and 4.35% from April 1st to April 24th, and closed at 4.31% on April 24th.

Barron’s reports that the 10-year Bollinger Bands have narrowed to their narrowest level since the classic coiled setup on January 16, and Reuters technical commentary suggests that yields are positioned inside a larger symmetrical triangle that often precedes sharp directional moves.

On April 27, the 10-year rate rose again towards 4.32% as commodity prices and geopolitical risks affected inflation expectations, adding input into the direction of yields outside of the Fed’s control.

A compressed yield range is a market that stores energy before making a decision.

Events that can release that energy arrive one after another. The FOMC will be held on April 28-29, and the BEA will release advance GDP estimates for the first quarter on April 30, along with March personal income and expenditures and the PCE deflator, and the employment cost index will be released the same morning.

This is the third macro indicator in two days, enough to effectively move US Treasuries in either direction, and enough to change the context of the financial conditions that Bitcoin currently relies on.

Important points

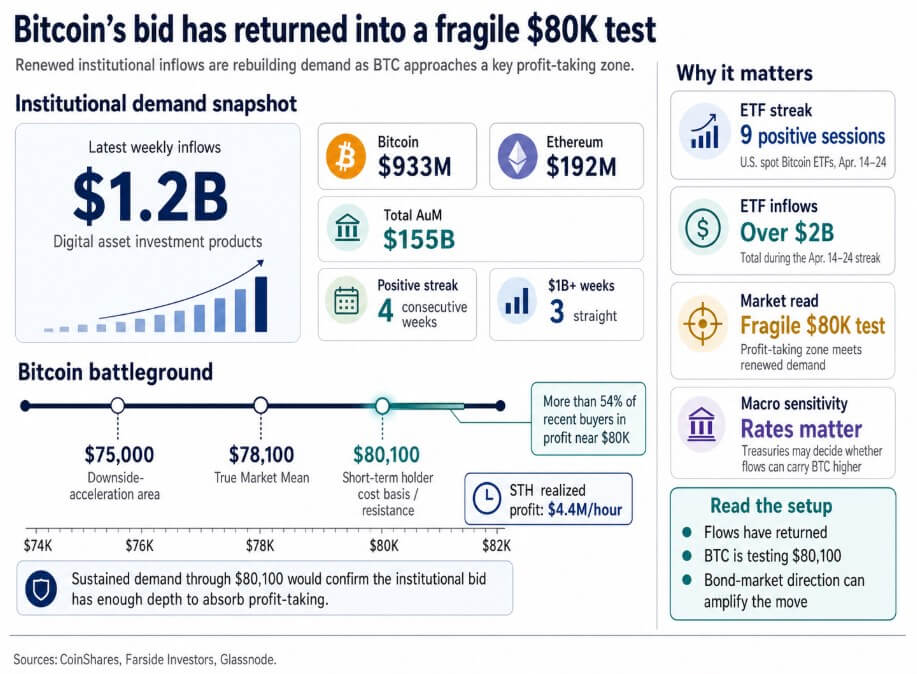

Bitcoin is likely to be the first to see Treasury repricing, as crypto bidding has reshaped itself into an already fragile technology sector.

CoinShares’ latest weekly report shows that inflows into crypto asset investment products reached $1.2 billion, the fourth consecutive week of positive growth and the third consecutive week of over $1 billion, with $933 million flowing into Bitcoin and $192 million into Ethereum, bringing total assets under management to $155 billion.

The U.S. Bitcoin Spot ETF recorded nine consecutive positive trades from April 14 to April 24, totaling more than $2 billion in inflows, according to daily ETF data from Farside Investors.

The risk is that buyers return just before Treasuries decide on a direction. According to a March 23 note from CoinShares, weekly capital inflows slowed sharply after the market interpreted the meeting as a pause for hawks, and crypto products suffered $405 million in outflows after the FOMC.

Crypto bidding was real at the time, and macro reprices overtook it anyway.

This episode has immediate relevance now as Bitcoin approaches the $80,000 test with the same ingredients and the unresolved variable of what the bond market will do next.

What on-chain data shows

Glassnode’s April 22nd report noted that Bitcoin has regained its true market average of $78,100, with $80,100 being the upper limit of resistance for the time being on a short-term holder cost basis.

ETF flows turned slightly positive again, spot demand showed an early recovery, and short-term holders saw profits jump to $4.4 million per hour.

Glassnode also pointed out that Bitcoin’s own implicit and real volatility has shrunk, leaving no premium in option pricing. The government bond market and the Bitcoin market are spiraling at the same time, and given the macro calendar in front of us, there is a more immediate cause for the interest rate market to move first.

Glassnode’s framework provides battleground coordinates as sustained demand up to $80,100 confirms institutional bids are deep enough to absorb profit-taking.

A failure here that pushes BTC back toward $78,100 would leave the true market average as the last meaningful support before Glassnode’s $75,000 downside acceleration region begins.

The direction of the bond market will determine which of these outcomes is resolved.

potential consequences

The bull case arises from falling yields. If the 10-year bond closes below April’s bottom near 4.26%, especially if it breaks above the Reuters technical pivot of 4.23%, then Bitcoin will get the cleanest macro environment the current bull market demands.

Lower yields will reduce the pressure on discount rates for risky assets, support liquidity trading, and increase the likelihood that a weekly inflow rate of $1.2 billion will allow BTC to break through the $80,100 resistance ceiling and maintain sufficient absorption.

In this setup, the ETF’s nine-session streak and CoinShares’ four-week positive streak would be seen as early evidence of a sustained demand regime, and the test period for the rally would end.

The October 2025 peak in total assets under management of $263 billion serves as a good benchmark for how far institutional investor re-engagement has yet to go.

The bear case arises from rising yields. If the 10-year note moves above 4.35% and moves towards Reuters’ 4.6% upside resolution area, financial conditions will tighten just as Bitcoin is about to enter the zone where more than 54% of recent buyers have booked profits.

BTC stalled at $80,100 and the profit-taking that Glassnode already has at $4.4 million per hour accelerates, with sellers testing the true market average at $78,100.

Below this level, Glassnode’s $75,000 downside acceleration zone will come into play and the market will reconstitute the entire series of inflows as institutional capital that arrived before the bond market closed.

The March case law embodies this trend, as once the macro reading became hawkish, even weekly demand of more than $1 billion could not prevent the $405 million outflow after the FOMC. The same mechanism will be available again.

| scenario | what happens at the treasury | BTC response | major level | what it means |

|---|---|---|---|---|

| bull case | 10-year bonds close near April bottom 4.26% and break through Reuters 4.23% technological pivot | Bitcoin gains the cleanest macro backdrop, ETF and ETP inflows gain support, BTC is likely to clear and hold on top $80,100 | 10 years: below 4.26%, then below 4.23% | Bitcoin: Cleared $80,100 and remained above $78,100 | Falling yields confirm the relevance of institutional bidding, and recent inflows provide evidence of a more durable demand regime. |

| Neutral/flow dependent case | 10 years stay within April range 4.26% and 4.35% | Bitcoin continues to rely on ETFs, ETPs, and spot demand to absorb supply near resistance, with no clear macro tailwinds or headwinds. | 10 years: 4.26%~4.35% | Bitcoin: Can hold from $78,100 to $80,100 | Macro remains unresolved, and Larry will live or die depending on whether the institutional flow can continue to work independently. |

| bear case | Interruption of the above 10 years 4.35% and starts moving towards Reuters 4.6% Upper resolution area | Financial conditions tighten as BTC enters profitable zone, Bitcoin stalls at next level $80,100seller test $78,100and $75,000 Works if support fails | 10 years: Over 4.35% and then heading towards 4.6% | Bitcoin: $80,100 Fail, $78,100 Loss, $75,000 Risk | Rising yields reprice liquidity as bond markets turn Bitcoin streak into yet another macro-driven failed rally |

Bitcoin’s next move could start in the U.S. Treasury market. Institutional bids have recovered in ample channels, confirming a broad recovery in demand.

But the bid came back before the bond market could indicate whether the macro environment was working in its favor or against it.

A fall in US Treasuries would make Bitcoin’s $80,000 test much easier, and the institutional thesis would be effectively macro-confirmed for the first time. If U.S. Treasuries rise sharply, duration repricing will be the determining factor, and the rally will fail based on macro reasons alone.

(Tag translation) Bitcoin