Just as investors brace for new signals from the Federal Reserve and the US labor market, Bitcoin prices are entering a key week with several on-chain models pushing the market floor lower.

This change has sharpened the debate not only on how much the flagship digital asset will fall, but also on how long the recovery process will take, even if the worst sell-off is near.

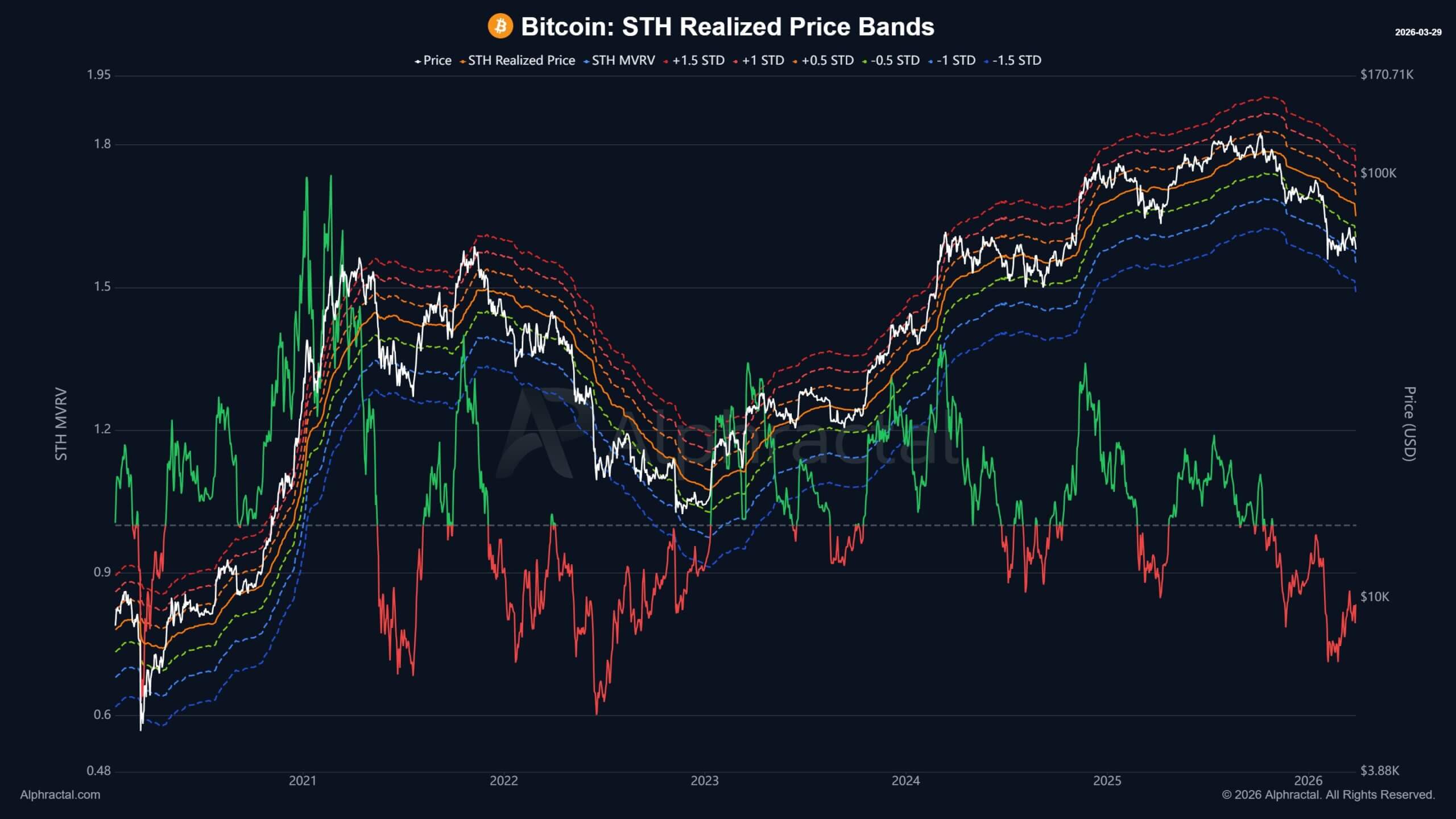

Short-term Bitcoin holders have noticed a sharp decline in the price range in recent weeks, pulling down levels that traders are watching for signs of capitulation, according to data from Alpharaktal.

CEO Joanne Wesson said that in past cycles, capitulation events were often completed when Bitcoin neared the bottom of the blue band, creating a strong local buying opportunity. With that band now lower, the model points to a possible bottom near or slightly below $50,000.

Meanwhile, other widely tracked on-chain signals are concentrated in a similar range. Willy Wu said Bitcoin could bottom between $46,000 and $54,000, but the CVDD floor is around $45,500 and continues to rise gradually.

Taken together, these indicators suggest that the zone has moved lower, where deep value buyers may begin to enter amid heightened volatility and uncertainty.

Support is building, but stress is still building

Glassnode’s cost-based data shows that the market is still trying to build top support.

According to the company, Bitcoin is trading near the lower end of the $60,000 to $70,000 range as new buyers accumulate supply, but the size of the cluster remains thinner than the foundation that formed before the strong recovery in the earlier cycle.

But as BTC continues to struggle, the pressure behind the surface is becoming harder to ignore.

According to CEX.io’s Bitcoin Impact Index, more than 30% of Bitcoin held by long-term holders is currently in the red, the highest percentage since 2023.

The company said more than 4.6 million Bitcoins owned by long-term holders are underwater, and 47% of all Bitcoins in existence are now in losses, matching levels seen during the most stressful weeks of February.

This deterioration is notable since long-term holders had only recently returned to selling at a profit.

By the end of the latest week, SOPR had fallen to 0.724, erasing six weeks of improvement and forcing long-term holders to sell at their biggest losses in three years. Short-term holders also came under pressure, with realized gains and losses falling to their lowest level since late January.

This pattern resembles an early failure stage. CEX.io compared the current configuration with mid-2018 and mid-2022. At the time, a similar disconnect between price movements and on-chain convictions appeared before Bitcoin fell further.

The company said the recent rise in the stress index was the steepest since late January, when Bitcoin continued to record one of its most difficult periods in 2026.

What is noteworthy is that market liquidity has also declined at the same time. Net stablecoin inflows to exchanges went from significantly positive to significantly negative on a daily average, losing one of the market’s key supports.

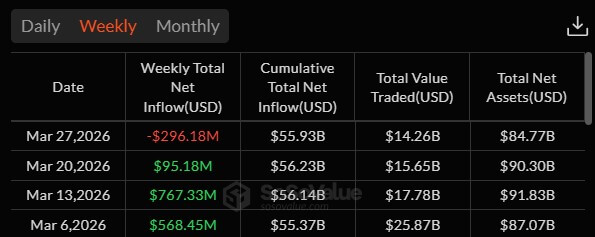

After four consecutive weeks of inflows, the Spot Bitcoin ETF recorded net outflows of $296 million for the week ending March 28, while the Spot Ethereum ETF posted a loss of $206.58 million, according to SosoValue data.

When institutional flows retreat, the burden of support shifts back to spot buyers, long-term holders, and short covering.

The mining economy is adding further pressure. Between 15% and 20% of miners are now unprofitable, as the hash price rate fell to its post-halving low in February, at around $28 per petahash per second per day.

Rising energy costs have raised the risk of a treasury sale, while Bhutan’s steady Bitcoin sales have reinforced widespread perceptions of oversupply in the market.

History shows recovery takes time

On the other hand, caution is not limited to price targets. Bitcoin analysis platform Ecoinometrics said that a sharp recovery in Bitcoin rarely happens in isolation and typically requires broader changes in the macro context, including changes in monetary policy.

This backdrop is not yet sufficiently supportive to justify expectations of a rapid recovery.

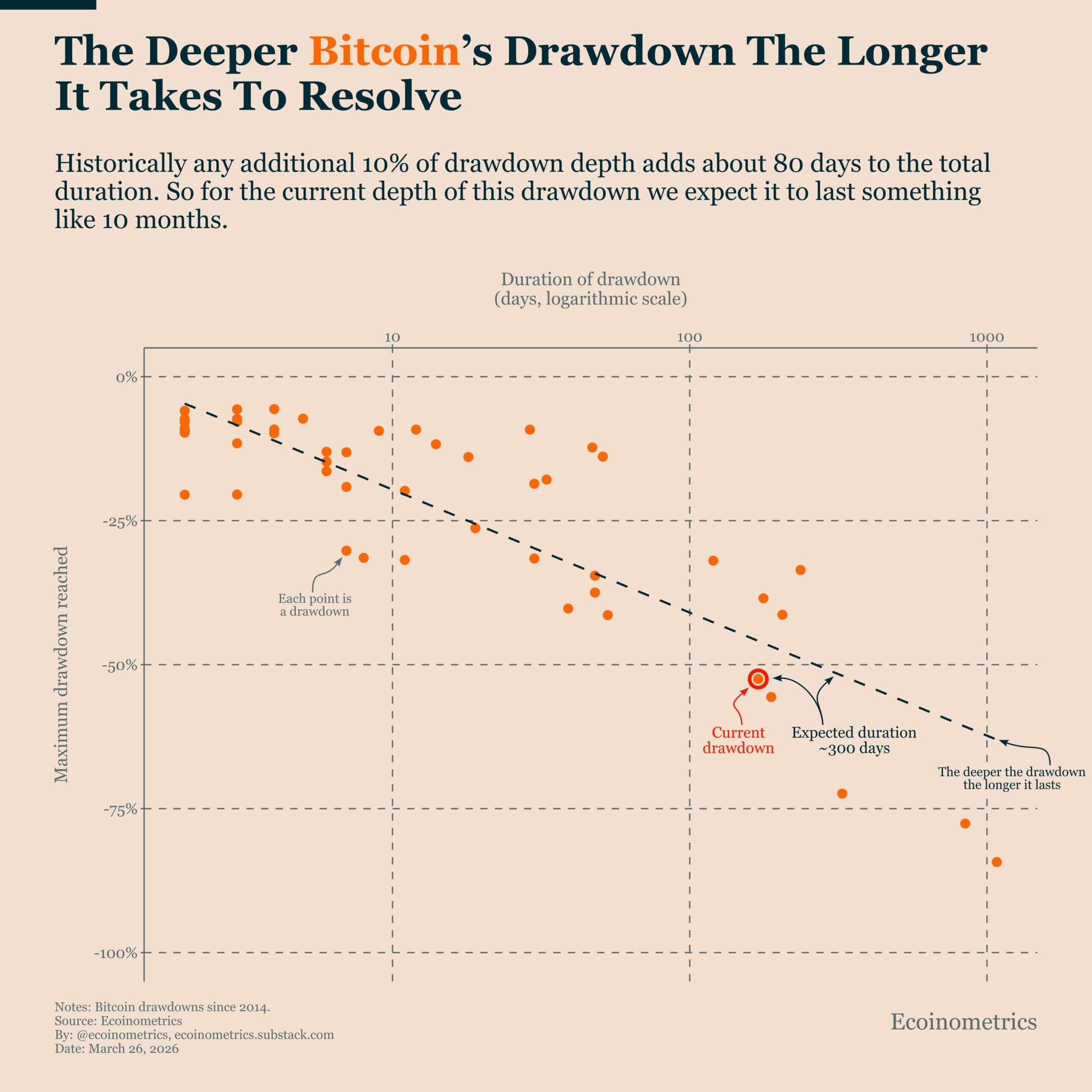

The company’s drawdown analysis helps explain why. Econometrics studied the entire Bitcoin cycle since 2014 and found a consistent relationship between the depth of the decline and the time it takes for the market to fully recover.

Every 10 percentage point increase in drawdown depth tends to increase the total duration by about 80 days. On top of that, the current decline means the recovery period is about 300 days and the market is still only about halfway through.

That doesn’t rule out the possibility of a rally. Bitcoin may bounce, consolidate, and reverse several times before a full recovery materializes.

However, historical patterns are against a linear return to previous highs. Even if the market is moving toward a reliable floor zone, the path out of that zone can be slower and more uneven than bullish traders would like.

This is where the lower-bottom model and the theory of slower repair begin to intersect. The token could approach the washout range without being ready for a new sustained uptrend.

This will require price support to be commensurate with stronger demand, more stable financial flows, and a macro context in which financial conditions are no longer tight.

Macro calendar will be carried over

The recovery timeline, which some analysts are already measuring in months rather than weeks, now hinges on a dense set of U.S. economic data starting Monday with Fed Chairman Jerome Powell’s appearance at Harvard.

Federal Reserve Chairman Jerome Powell is scheduled to participate in a moderated debate at Harvard University on March 30th, and the Bureau of Labor Statistics is scheduled to release its March employment report on April 3rd.

In between these events, investors are also watching consumer confidence data and labor market trends for signs of whether inflationary pressures from rising energy costs are starting to collide with modest growth.

At this point, markets will be trying to determine whether policymakers are facing a temporary shock or a combination that will keep interest rates under control for an extended period of time.

The connection between Bitcoin and the debate is becoming more direct. Leading digital assets are trading near the lower end of new buyers’ cost-based ranges as oil, yield and labor market expectations continue to drive risk appetite across assets.

Easing energy stress and softening labor products could help stabilize financial conditions and give Bitcoin room to maintain support. However, strong employment data alongside robust inflation expectations would point in the opposite direction, sustaining macro pressures and leaving markets vulnerable to further declines.

For now, the Bitcoin market is caught between a market that is starting to look statistically undervalued and a macro environment that has yet to turn decisively supportive. A model pointing at $45,000 to $54,000 is not a guarantee that the price will trade at that price.

Rather, they suggest that market capitulation predictions have been revised downwards and that a sustained recovery is likely to depend as much on the next turn in the macro cycle as on the next bid for cryptocurrencies themselves.

(Tag Translation)Bitcoin