Even as U.S. physical Bitcoin exchange-traded funds (ETFs) continue to attract new capital, gold has given up this year’s gains and fallen into bear market territory, sending the two assets on very different paths.

Spot gold prices were trading around $4,388 an ounce on March 23, down about 22% from the January 29 record of $5,594.82, according to goldprice.org. The decline accelerated after the recent Middle East conflict began on February 28th. Since then, gold has fallen about 17%, reversing the rally that sent gold higher in the early weeks of 2026.

At the same time, institutional money continued to flow into the US spot Bitcoin ETF market. The fund had net inflows of about $2.42 billion in the four weeks ending March 20, according to data from Pharside Investors.

This divergence has drawn attention across macro and digital asset markets, as gold and Bitcoin are often discussed in similar terms during times shaped by inflation concerns, currency dilution, and geopolitical stress.

But over the past month, investors have been treated very differently. Gold faced liquidation pressure as demand for cash increased and interest rate expectations remained high. Bitcoin continued to draw allocations through intermediation and advisory channels through ETF structures.

This move deserves attention, as the gold market entered 2026 with strong momentum. That pullback now meets the widely used market definition of a bear market: a decline of 20% or more from a recent peak. In contrast, Bitcoin has held up well enough to maintain interest among ETF buyers during the same period of volatility.

Gold regains year-to-date gains as interest rates remain high and investors raise cash

Gold’s decline unfolded against a macro backdrop of lower yields and less support for assets that tend to benefit from a weaker dollar.

The Fed kept interest rates on hold in March, forecasting a base rate of 3.4% at the end of 2026, while core consumer spending inflation would remain at 2.7%. The combination reinforced the view that restrictive policies could last longer than investors expected earlier this year.

For bullion, the impact is direct. Higher interest rates increase the opportunity cost of holding non-yielding assets. A rising dollar makes gold more expensive for buyers using other currencies, increasing pressure.

These forces also intensified as investors also sought cash and liquidity after the Middle East shock forced a reassessment of growth, inflation and energy expectations.

Fund flow data quickly captured the change. Global gold and precious metals funds recorded net outflows of about $5.19 billion in the week ending March 18, the largest weekly outflow since at least August 2018, according to LSEG Lipper data. Money market funds had inflows of $32.57 billion during the same week.

This rotation suggests investors have moved away from positions that had previously benefited from inflation and geopolitical hedging demands, seeking liquidity.

Gold’s decline therefore fits into a broader portfolio adjustment where maintaining flexibility has become more important as markets reassess the expected direction of monetary policy and commodity prices.

The decline also comes after a period when gold appeared to have solid long-term support. Central bank demand supported the bullion market through 2025, and the reserve case remained in place as 2026 began.

The recent decline shows how strongly the short-term macro environment can overwhelm structural support in a matter of weeks.

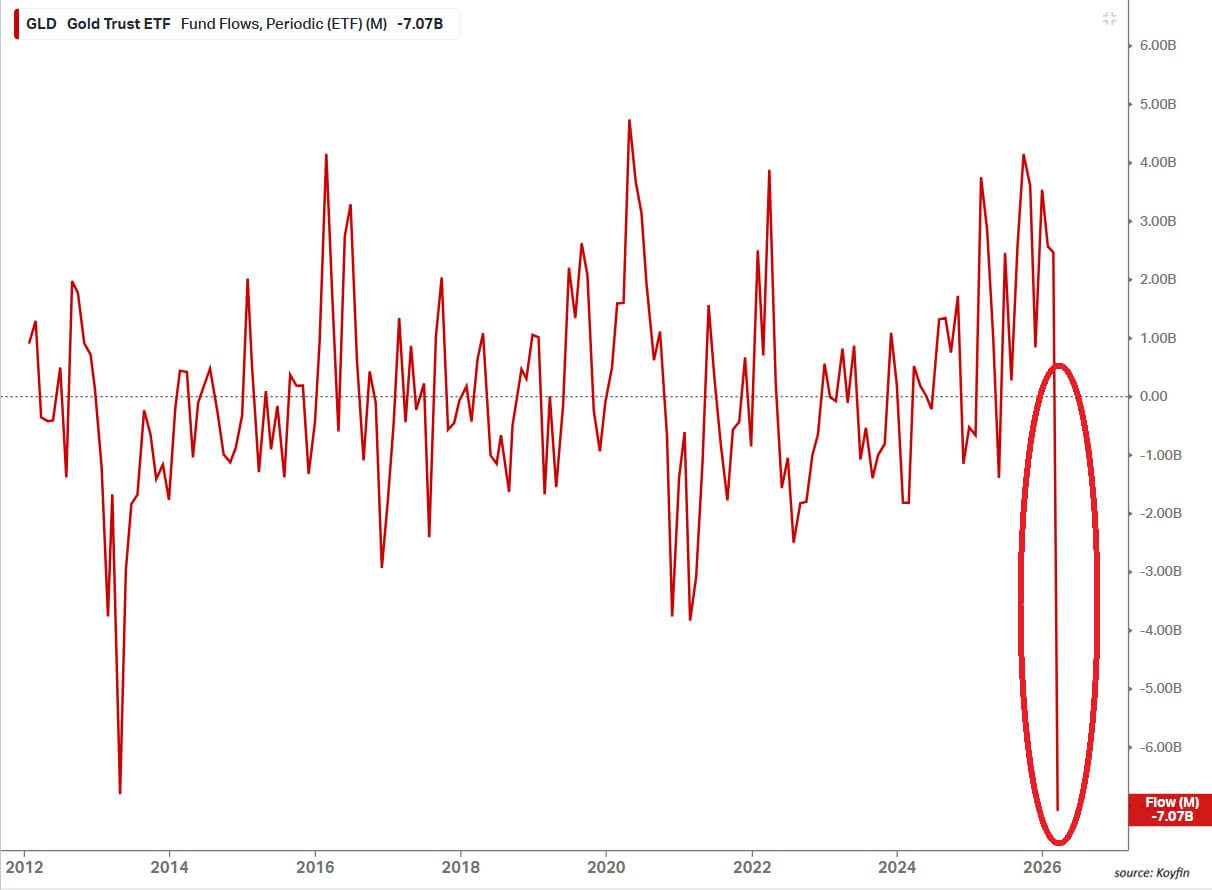

Additional fund data points in the same direction. SPDR Gold Shares (GLD), the largest gold-backed ETF in the U.S., recorded $7.07 billion in outflows in March, according to market data.

This exceeded the $6.8 billion in monthly withdrawals in April 2013. The pace of redemptions reflects the speed with which investors reversed their positions after the rally in gold prices at the beginning of the year.

According to the criteria used in financial markets, a 22% decline from the January peak clearly marks a move into bear market territory.

Therefore, gold’s decline represents more than a normal decline following a rally. This signals a broader withdrawal from trade, which has been underpinned by reserves accumulation, geopolitical hedging and concerns about sustained inflation.

Bitcoin Fund sets record for strongest inflow in 2026

While the gold market is in a downturn, US physical Bitcoin ETFs have recorded the strongest inflows this year.

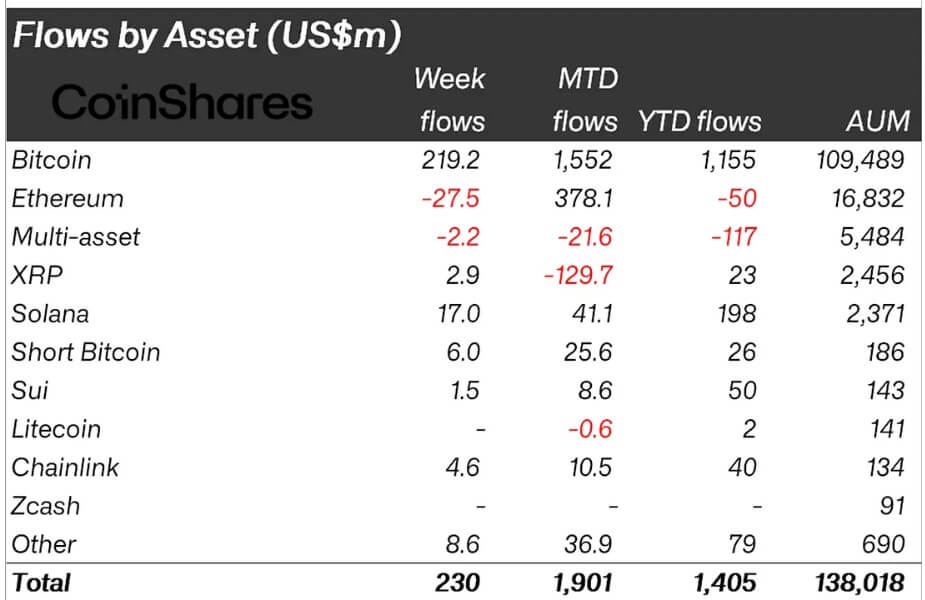

The 12 spot Bitcoin funds in the U.S. recorded net inflows for the fourth straight week, adding more than $2 billion during that period, according to Farside Data. This is the longest period in 2026 and the strongest since August and September 2025, when the fund absorbed more than $3.8 billion.

CoinShares data shows similar trends globally. The company announced that inflows into its Bitcoin exchange-traded products have hit $1.5 billion so far this month.

These inflows came at a time of war risks, changing expectations for U.S. interest rates, and renewed volatility across commodities. Even against this backdrop, financial institutions continued to use ETF wrappers to add or maintain Bitcoin exposure while gold funds experienced significant redemptions.

Bitwise said last week that Bitcoin and other major crypto assets have outperformed U.S. stocks and gold since the beginning of March.

The asset manager said the move could indicate the early stages of rotation, but cautioned that recent price movements could reflect temporary volatility or isolated liquidity events. Bitwise added that historically gold has led Bitcoin by 4 to 7 months.

State Street Global Advisors outlined the March Gold Monitor Volatility Gap. Over the past 10 years, Bitcoin’s rolling 30-day volatility has averaged around 52.0, compared to 13.6 for gold.

According to the report, from January 2016 to February 2026, Bitcoin had 30 months with losses of more than 8%, while gold had one such month.

These numbers show what kind of exposure investors were taking through Bitcoin ETFs. Buyers were accepting greater volatility and deeper drawdowns in exchange for access to assets that some investors see as a hedge against fiat dilution and policy risks.

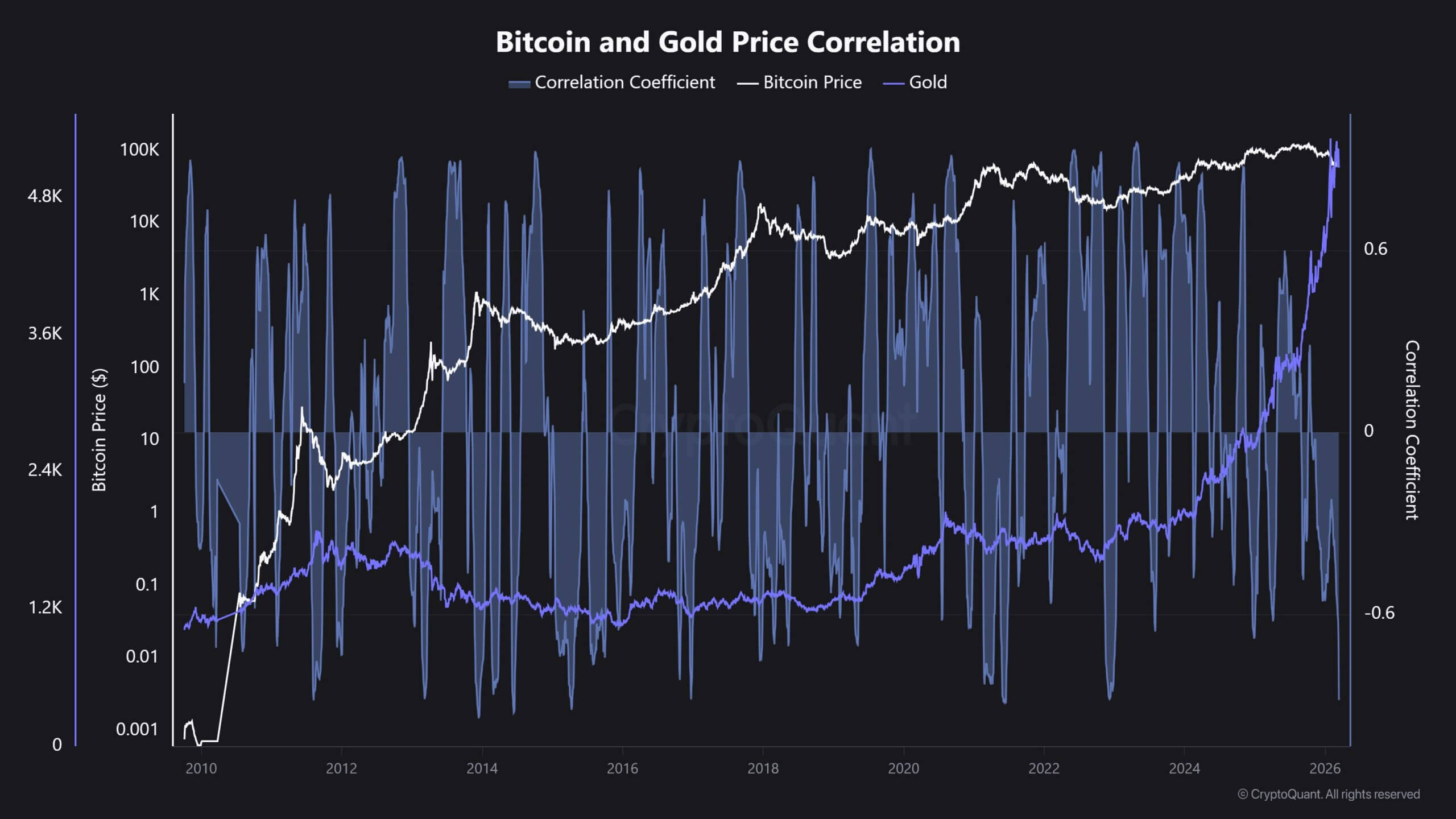

CryptoQuant data also shows how far apart the two assets are. The firm said the correlation between Bitcoin and gold has fallen to -0.88, the lowest since November 2022, indicating that the two assets have been moving in opposite directions with unusual momentum during the measurement period.

Oil and interest rates could shape the next step

Long-term support for gold has not disappeared even after the March crash, which is part of the reason why the current split between gold and Bitcoin is receiving more attention.

The World Gold Council announced that total demand for gold, including over-the-counter activity, will exceed 5,000 tonnes for the first time in 2025. Gold ETF holdings increased by 801 tonnes last year, with central banks purchasing 863 tonnes. In February 2026 alone, physically backed gold ETFs attracted $5.3 billion worldwide.

These numbers show that public sector buying and long-term investment demand remains strong heading into the current quarter.

The current drawdown therefore leaves investors balancing two forces: short-term macro pressures from interest rates, a strong dollar, and liquidity demands, and a structural reserve auction that lasted from last year into early 2026.

Oil prices are likely to play a central role in how that balance develops. Several banks have raised their 2026 Brent outlook in the wake of the recent Middle East shock. Bank of America raised its outlook to $77.50 a barrel, while Standard Chartered raised its outlook to $85.50. Bank of America also outlined a path to $130 in the event of prolonged supply disruptions.

Rising oil prices will stimulate inflation expectations, potentially prolonging the U.S. Federal Reserve’s cautious stance. That would impact gold and Bitcoin through different channels.

If policy remains restrictive, gold will continue to face pressure from rising real yields and a stronger dollar. Bitcoin will become more tied to liquidity conditions, institutional risk appetite, and the appetite of ETF buyers to continue to add exposure through regulated products.

For now, the clearest market signal is the split itself. Gold, long treated as a traditional store of value in times of stress, has fallen more than 20% from its January highs and entered a bear market. Bitcoin, an asset more commonly associated with large price movements, continued to attract ETF inflows throughout the period.

(Tag translation) Bitcoin