The U.S. economy added 178,000 jobs in March, nearly triple the consensus estimate of 60,000, and the unemployment rate fell to 4.3%. It’s the kind of print that resets the macro narrative and hits risk assets before the trader has even finished the first read.

Unfazed by the data, Bitcoin traded at around $67,000. The 10-year Treasury yield rose 4 basis points to 4.35%, and the dollar index rose to 100.08.

The initial reading of the market was straightforward. When the labor market looks this strong, there is less reason for the Federal Reserve to cut interest rates, resulting in tighter financial conditions and weighing on macro-sensitive assets like Bitcoin.

Why this is important: Bitcoin reacted to more than just a jobs win. A strong labor market signaled less urgency for the Fed to cut interest rates. If this view is correct, yields and the dollar could remain firm, maintaining pressure on liquidity-sensitive assets like BTC.

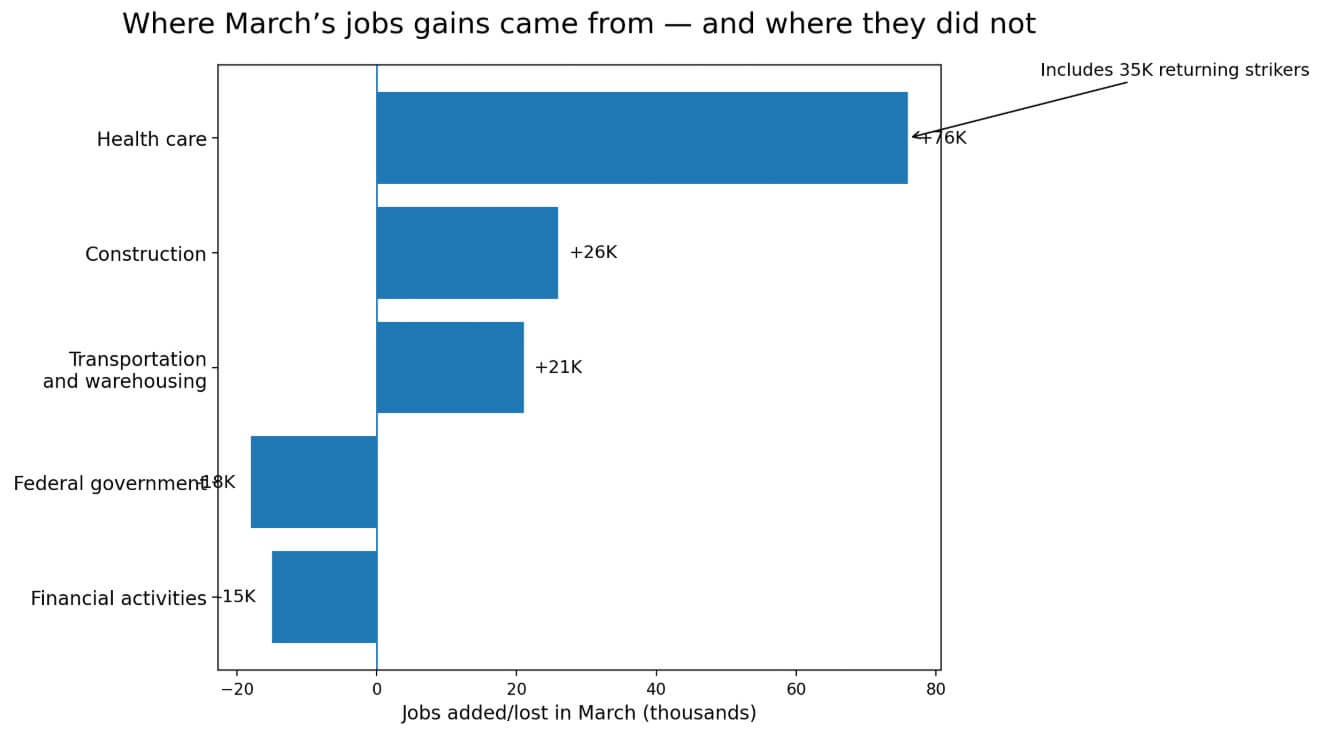

When you zoom in on where those 178,000 jobs came from, the picture becomes less pretty. In the medical field alone, 76,000 jobs were added, 35,000 of which were workers returning from strikes in doctors’ offices. This number represents a catch-up in recruitment.

Construction added 26,000 jobs, partly due to the weather, and transportation and warehousing contributed an additional 21,000 jobs. Federal government employment fell by 18,000 jobs, and financial activity fell by 15,000 jobs.

The BLS noted that the total number of salaried employees has changed little in net terms over the past 12 months.

Against this background, March appears to be a reactionary rebound from the tumultuous February, with sector-specific catch-up driving most of the gains.

Household surveys move in the opposite direction.

The household survey, which tracks employed and unemployed people across the population, moved in the opposite direction to payroll statistics.

The civilian workforce decreased by 396,000 people in March, and the participation rate fell to 61.9%. The number of household employees decreased by 64,000, and the number of people not in the labor force increased by 488,000.

The number of alienated workers rose by 325,000 to 1.9 million, and the number of disengaged workers rose by 144,000 to 510,000. The average working week will be reduced to 34.2 hours.

Average hourly wages increased only 0.2% month-over-month and 3.5% year-over-year, with no wage acceleration to compensate for wage increases.

| indicator | March reading | why is it important |

|---|---|---|

| Number of non-farm employees | +178K | Contrary to expectations, the headline beat is strong |

| unemployment rate | 4.3% | The labor market appears to be strong at first glance. |

| civilian workforce | -396K | Signs of weakening labor market participation under the heading |

| labor participation rate | 61.9% | Few people are working or looking for work |

| household employment | -64K | People-based research has gone in the opposite direction from salary research. |

| not working in the labor force | +488K | Enhances soft reads under the hood |

| marginal workers | +325,000 ~ 1.9,000 | Indicating that labor force cohesion is weak in the periphery |

| a demotivated worker | +144K to 510K | This suggests that an increasing number of workers are giving up on job hunting. |

| Average working hours per week | 34.2 hours | Shorter working weeks may indicate softening demand for labor |

| average hourly wage | +0.2% compared to the previous month, +3.5% compared to the previous year | No re-acceleration of wages to confirm payroll beat |

The February revision adds even more layers. BLS decreased from -92,000 to -133,000 in February and was revised upward from 126,000 to 160,000 in January. The two-month net correction is only -7,000, making the pattern noisy and lacking consistent direction.

Employment growth in the first quarter averaged about 68,000 jobs per month, a modest pace by any expansion standards.

The BLS will revise its monthly forecasts twice as additional employer reports arrive and seasonal factors are reset.

Since 2003, the average absolute employment number from the first to third estimates was 51,000. When this size is revised, the March population would be around 127,000, up from 178,000, which is not as dramatic.

To erase the entire beat, job creation in March would have to exceed 118,000, about 2.3 times the historical average, and the usual revision noise doesn’t reach that far.

The BLS’s annual benchmark revision eliminated 898,000 jobs from March 2025 pay levels, four times the average absolute benchmark revision over the past 10 years.

With this revision, the recent first edition of the jobs report established more uncertainty than the market would normally price in during the first trading hours after a strong print run.

Interest rate channel behind Bitcoin decline

The Fed kept its target range at 3.50% to 3.75% as of March.

The participants’ median forecast is for the unemployment rate to be 4.4% in 2026, the PCE inflation rate to be 2.7%, and the year-end federal funds rate to be 3.4%. With the unemployment rate in March at 4.3% and the number of employed people at 178,000, policymakers did not need to act urgently.

NYDIG’s research frames the relationship between Bitcoin and macros in the same terms. This means BTC is trading at real rates, liquidity, and risk appetite. The Fed maintaining its strong labor market position removes the short-term catalyst that Bitcoin needs most.

The February JOLTS report confirms this without causing alarm. Although the number of job openings remained at nearly 6.9 million, the number of people hired fell to 4.8 million, and the hiring rate fell to 3.1%, the lowest level since April 2020.

The number of new jobless claims for the week ending March 28 was 202,000, near the lowest level of the cycle.

Taken together, these data paint a picture of a stagnant labor market, with layoffs subdued, new hiring slowed, and companies holding staff numbers steady.

This environment will not cause the Fed to pivot, and if the Fed does not pivot, financial conditions will tighten for a longer period of time.

Potential consequences for Bitcoin

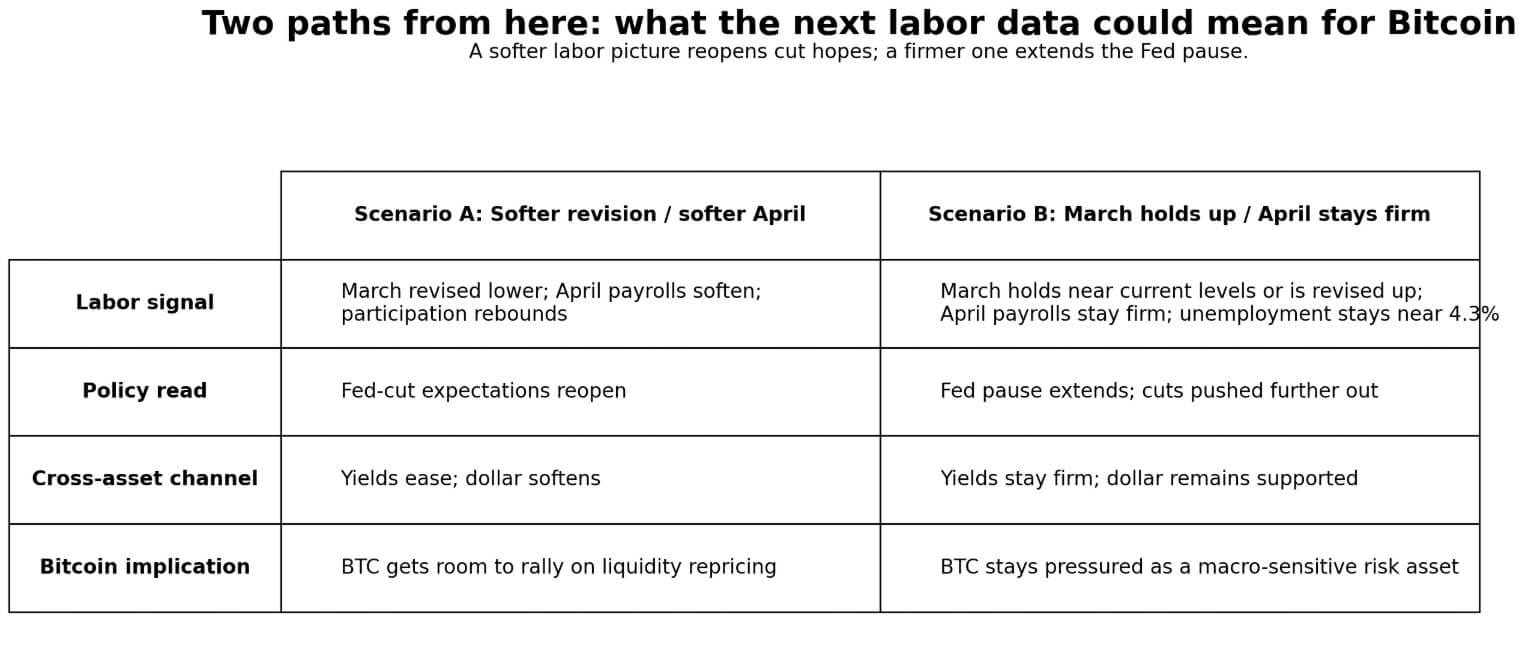

Bitcoin price movements on April 3 were carried out through the interest rate channel. A strong labor force has lowered expectations for rate cuts, yields have remained solid, and a strong dollar has tightened conditions for liquidity-sensitive assets. This channel can be inverted.

If the BLS significantly lowers the March payroll to less than 100,000 people, and if the number of participants recovers while April payrolls remain weak, the theory that “headline strength alone” will gain momentum.

Expectations will resume lowering, yields will fall, and Bitcoin will have room to reprice its liquidity. Weaknesses in the household budget survey, strikes and distortions in returns in the medical sector, and JOLTS employment declines all make that path plausible, but we will have to confirm it with the April statistics on May 8th.

If March stays close to current levels or the BLS revise it upwards, with April payrolls exceeding about 125,000 while the unemployment rate remains below 4.3%, February will be a clear outlier.

The Fed has become more confident in extending its suspension, interest rate cuts have been pushed back further, and Bitcoin continues to trade as a macro-risk asset with no short-term liquidity booster.

The move between assets on April 3, with yields rising, the dollar rising, and Bitcoin falling, showed that the market was already starting to price in that path.

The next employment announcement is scheduled for May 8 at 8:30 a.m. ET, with April salary announcements and the first revisions both in March.

This is therefore a real checkpoint for any discussion built on the April 3 print. The March CPI will be released on April 10, and the next FOMC meeting will be held on April 28-29, giving the Fed two data points to absorb before resetting policy.

In particular, the CPI will test whether a strong labor market translates into persistent inflation or the slowdown in wages that the March print edition had already hinted at.

(Tag translation) Bitcoin