Markets are pricing in any Fed rate cuts in 2026 as the U.S.-Israel war with Iran pushes oil prices above $110 a barrel and consumer gasoline prices approach $4 a gallon.

Important points:

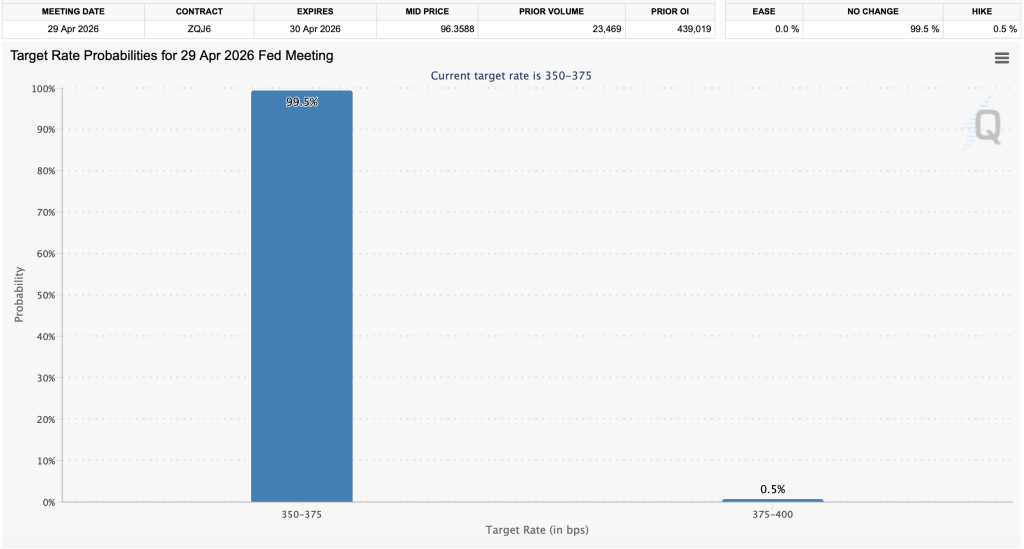

- CME federal funds futures indicate a 99.5% chance that the Fed will keep interest rates unchanged at 3.50-3.75% at the April 29th FOMC meeting.

- Following President Trump’s April speech, WTI crude oil exceeded $110 per barrel, and Polymarket’s odds of a zero rate cut for the full year of 2026 rose to 36%.

- The next big test comes on June 17th, with markets pricing in a 96.7% chance that the Fed will leave borrowing costs unchanged again.

Fed, market consensus: No interest rate cuts, no need to rush into easing

As of this weekend, federal funds futures tracked by the CME FedWatch tool had a 99.5% chance that the Federal Open Market Committee (FOMC) would leave benchmark interest rates unchanged at 3.50% to 3.75% at its April 29th meeting. A month ago, on March 4, traders had an 88.2% hold probability, with nearly 12% still expecting a rate cut to 325-350 basis points. That window has closed.

The changes follow President Donald Trump’s prime-time address to the nation this week, in which he vowed to attack Iran “very hard” in the coming weeks, threatened to blow up power plants and downplayed U.S. dependence on oil in the Strait of Hormuz. The market reacted immediately. WTI crude oil has settled above $110-112 per barrel, and Brent crude has settled above $107, levels not seen consistently since the Russia-Ukraine shock in 2022.

Houston’s spot crude oil premium rose to $5.50 above futures. The Strait of Hormuz, through which about 20% of the world’s oil supplies pass every day, has seen tanker traffic largely halted due to Iranian naval actions since fighting escalated in late February 2026. The International Energy Agency has coordinated emergency stock releases in more than 30 countries, easing but not eliminating the shortage.

These supply losses flow directly into the Fed’s preferred inflation gauge. The March 18 economic forecast summary revised the 2026 PCE inflation rate to 2.7%, up from the 2.4% forecast released in December. Core PCE also reached the same level. The Fed’s median interest rate cut is still one 25 basis point rate cut this year, but Chairman Jerome Powell made clear in a post-meeting press conference that officials need more time to assess whether second-round effects, wage-price spirals and unanchoring of expectations materialize.

Prediction markets and deck seat swapping

Gov. Stephen Millan was the only dissenting vote at the March 17-18 meeting, voting in favor of immediate cuts. The other 10 voting members retained.

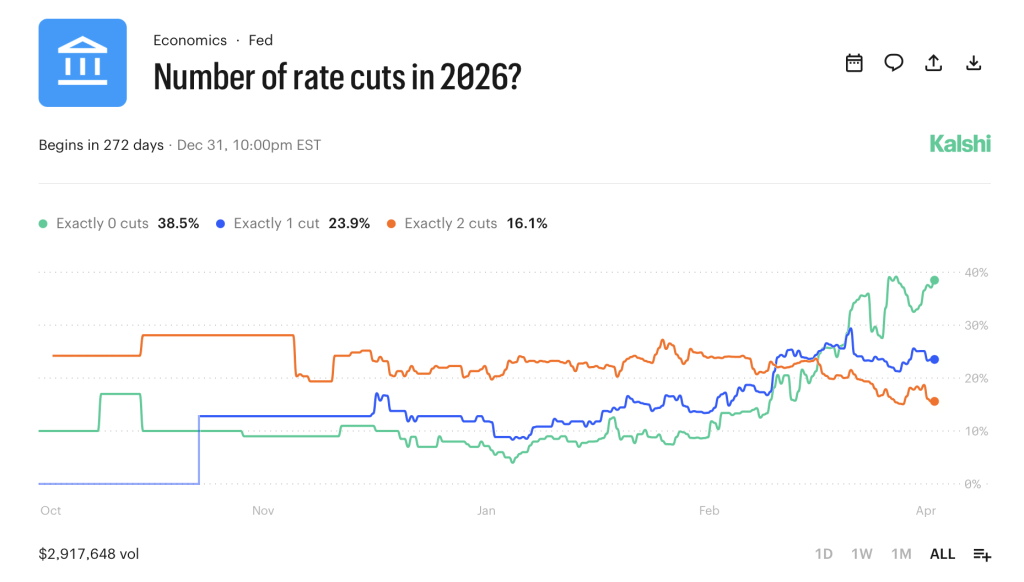

Prediction markets are more direct. Polymarket currently puts the probability of zero rate cuts in 2026 at 36%, up from 10% before the war. The odds of a single 25 basis point rate cut are 23%. Kalsi pegs the no-cut scenario at 38.5% and volume, reflecting real money conviction, at $2.9 million.

Regarding the June 17th FOMC meeting, CME FedWatch says there is a 96.7% probability that it will be held again. As of March 4, this figure remained at 66.8%, with 30.2% of traders still expecting a rate cut by June. That mitigation premium has almost completely disappeared.

Wall Street desks remain more optimistic than the futures market. For example, Citi still expects rate cuts to exceed 75 basis points this year. But City postponed its predictions by February. That division is important. Professional forecasters are considering scenarios where conflict escalates and oil retreats. Futures traders set the prices of the world as it exists today.

Powell juxtaposed the oil crisis with previous supply disruptions, the pandemic and tariffs, and said developments in the Middle East were “uncertain.” The Fed won’t act until it gets cleaner data. Future measures of inflation before and after the shock will attract close scrutiny, along with April’s jobs report. Still, the deck is being reshuffled, and Powell’s term as Federal Reserve Chairman ends on May 15, 2026.

Donald Trump has recommended Kevin Warsh as the next Fed chairman, but Powell’s term as Fed president ends on January 31, 2028. From that perspective, his position does not carry much weight. Mr. Powell holds one vote as one of seven governors until 2028, but he does not have the power to shape the outcome like the chairman. Historical precedent suggests that once an outgoing speaker becomes governor, he or she rarely maintains meaningful influence.

Meanwhile, as usual, American consumers are absorbing arithmetic. The national average gas price is approaching or exceeding $4 a gallon in countless states, an increase of about $1 since prewar days. The average 30-year home loan interest rate is around 6.38%. Borrowing costs remain high across the economy because the Fed has no room to ease without risking a second wave of inflation. It may arrive whether policymakers intend it or not.

The next FOMC decision will be made on April 29th. Unless a dramatic reversal in oil prices or a cease-fire is certain, the Fed is expected to do what the market has already priced in: do nothing.