The crypto IPO market is back, but the companies leading the charge are not the ones most exposed to token volatility.

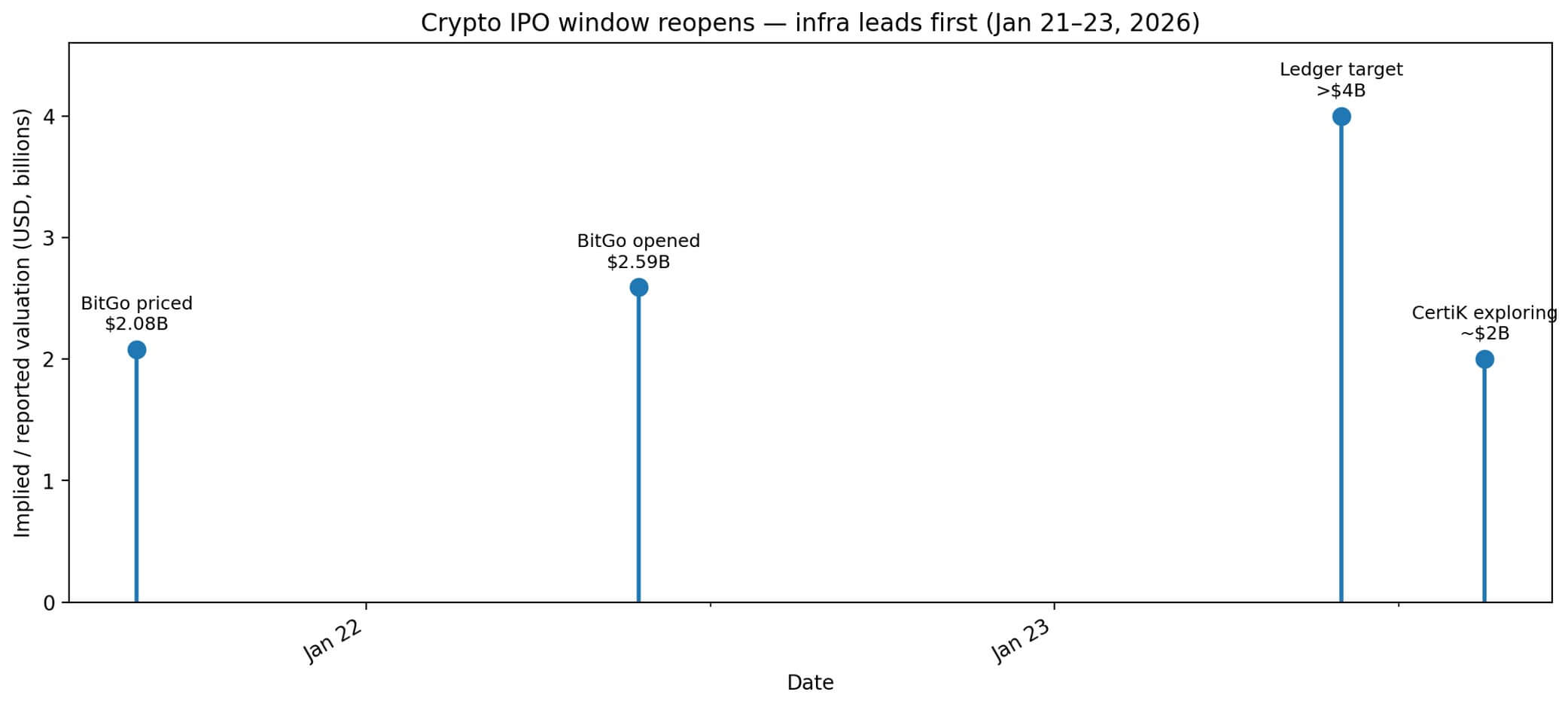

BitGo priced its initial public offering on January 21st at $18 per share, raising $212.8 million and valuing the custody platform at $2.08 billion. The stock opened the following day at $22.43, an increase of 24.6%, pushing the implied valuation to $2.59 billion.

Within 24 hours, two more security-focused companies signaled public market ambitions.

Hardware wallet maker Ledger is reportedly preparing to list in New York at a valuation of more than $4 billion, with Goldman Sachs, Jefferies and Barclays leading the process, according to the Financial Times.

CertiK, a blockchain security audit firm, confirmed to The Block that it is considering an IPO of approximately $2 billion.

The pattern is clear. Public markets reward regulated infrastructure narratives more than token-exposed speculation.

BitGo clearly positions itself as a profitable regulated digital asset infrastructure, highlighting its national charter approval and net profit of $35.3 million in the first nine months of 2025.

Ledger and CertiK are touting the trust layer’s role as wallet security and protocol auditing at a time when institutional demand for security infrastructure is growing faster than demand for circular trading platforms.

This is not just a reflexive bounce; a filtering mechanism is in place.

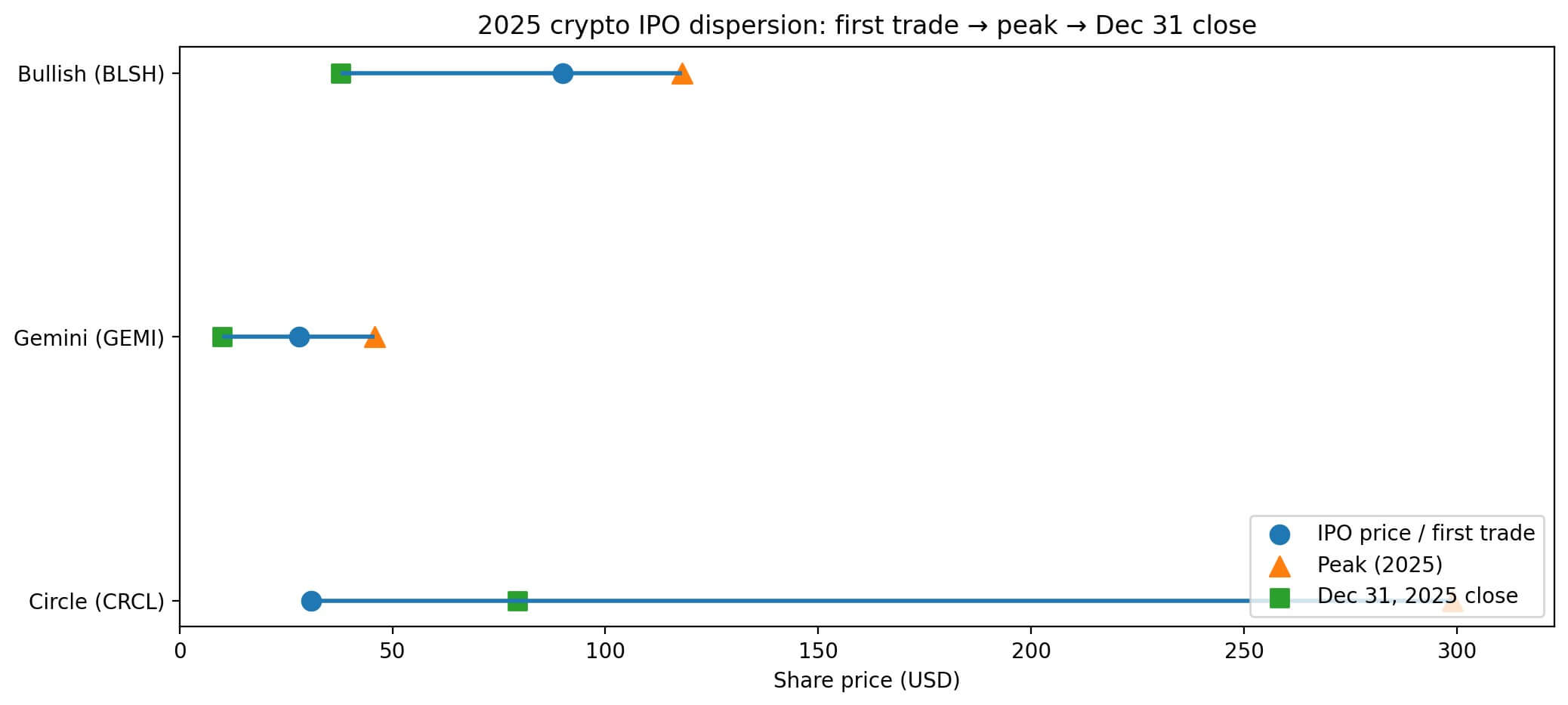

The IPO window opened in 2025, and Circle, Gemini, and Bullish were listed, but their performance diverged greatly.

Circle was priced at $31 and scaled to raise $1.05 billion. The bullish stock price has more than doubled since its debut, giving the exchange a value of about $13.16 billion. Gemini raised $425 million at a valuation of $3.33 billion.

However, by December 31st, Gemini had fallen about 64.5% from its all-time high, and Circle had rebounded sharply from its high near $300.

The market rewarded momentum first, then fundamentals. Companies now preparing to go public are betting that investors have learned their lesson.

Regulated Infrastructure Looks Not in Beta

BitGo’s debut tests the hypothesis that custody and compliance infrastructure has lower perceived risk than platforms whose returns move in tandem with token prices.

BitGo reported net income of $35.3 million for the first nine months of 2025 and received approval to transition to national charter status, a regulatory milestone that signals durability for institutional investors.

This national charter is important because it brings BitGo under federal banking supervision, reduces counterparty risk for customers, and creates a clearer path to serving regulated financial institutions.

It’s not a cosmetic. This is a structural moat that competitors operating under state-level trust charters or offshore jurisdictions cannot reproduce without years of regulatory engagement.

Ledger’s reported $4 billion valuation target leans toward the same logic. The FT points out that Ledger has generated triple-digit multi-million dollar revenues, and its undisclosed 2023 valuation was previously at $1.5 billion.

The company’s pitch focuses on secure storage infrastructure and institutional custody demands, positioning its hardware wallets as enterprise-grade security tools rather than consumer gadgets.

Security is becoming an investable area

CertiK’s IPO consideration shows that security is moving from a cost center to an investable category.

Chainalysis estimates that $17 billion will be stolen in cryptocurrency fraud and fraud in 2025. This number shows why security spending is structural rather than discretionary.

CertiK positions itself as the infrastructure for auditing smart contracts and blockchain protocols to reduce systemic risk for developers, exchanges, and DeFi platforms.

The company’s securities firm has reached a private valuation of $2 billion in 2022 and is considering going public at a similar valuation.

The sales pitch is simple and clear. As on-chain capital flows increase and regulatory oversight increases, security audits will become non-negotiable.

But CertiK also has reputational issues that investors will scrutinize.

The company’s audit also covered the protocols in which the exploit later occurred, raising questions about its rigor and accountability.

Public market oversight will force clearer disclosures about CertiK’s methodology, customer focus, and how it will address reputational risks should its audited protocols fail.

Ledger and CertiK represent different slices of the trust layer: wallet security and protocol security. Still, the companies believe that investor demand is focused on companies that reduce their attack surface, rather than those that maximize token exposure.

The FT directly linked rising security demands to data theft and hacking, noting that institutional investors view secure storage and auditing as non-negotiable infrastructure.

What will an IPO application reveal?

Over the next three to six months, as companies file S-1 documents and roadshow materials, we will get clearer answers about revenue quality, regulatory posture, and customer concentration.

While profitability and regulatory approval are already clear with BitGo’s debut, Ledger and CertiK will face even more difficult questions.

For Ledger, investors will be scrutinizing the distribution of consumer hardware sales and institutional custodial revenue. Consumer hardware is cyclical and margins are compressed. Institutional custody is repeated and has high profit margins.

This combination will determine whether Ledger is a hardware company with custody benefits or a custody platform that happens to sell devices. The difference in valuation between these two stories is billions of dollars.

In the case of CertiK, our investigation will focus on audit liability, customer retention, and how the company manages conflicts when audited protocols issue tokens or raise capital. Security auditors face unique tensions. The more protocols you audit, the more likely they are to be exploited, creating reputational risk.

CertiK must demonstrate that its audit process is rigorous enough to justify a premium price and that its customer base is diverse enough to withstand individual protocol failures.

Both companies are also likely to face questions about client losses and exposure to hacking by exploiting audited protocols.

Retail investors want to understand tail risks, not just average outcomes. S-1 filings require disclosures about loss history, insurance coverage, and how companies are preparing for potential liabilities.

Scenarios range from 3 to 6 months

The basic case is a selective window to ensure a profitable and regulated infrastructure.

The disparity in performance beyond 2025 will strengthen a fundamentals-driven market where companies with clear unit economics and regulatory clarity receive funding, while platforms with token exposure will face skepticism. BitGo’s debut confirms that hypothesis.

The bullish case is that risk-on sentiment returns and the pipeline expands beyond storage and safety. The debut of Circle, Bull, and Gemini in 2025 showed that IPO demand could quickly return once crypto market sentiment improves.

Exchanges, DeFi platforms, and token exposure businesses could follow the infrastructure leaders into the market if Bitcoin gains and macro conditions ease.

The bearish case is macro tightening and risk-off sentiment, forcing postponements or downward revisions to expectations. That window narrows quickly if BitGo’s stock price falls or if Ledger’s roadshow reveals weaker-than-expected institutional demand.

what to see

Key metrics are filing date, revenue disclosure, profitability timeline, and regulatory status.

BitGo’s S-1 has already revealed $35.3 million in net profits and state charter approval.

Ledger’s filing will show whether its triple-digit, multi-million dollar revenue is profitable, and how much of that revenue comes from recurring business and one-time hardware sales to institutional investors.

CertiK’s filings reveal customer concentration, audit failure rates and how the company is preparing for reputational risk.

Public markets are pricing regulated infrastructure as low-beta exposure to cryptocurrency growth. This is a bet that custody, security, and compliance tools can capture value regardless of token price fluctuations. Because institutional adoption relies on mitigating operational and security risks before allocating capital.

BitGo’s debut justifies that bet. Ledger and CertiK test whether security infrastructure carries the same premium as custody.

The IPO window is open, but fundamentals are being filtered. Companies that can demonstrate profitability, regulatory clarity, and recurring revenue from institutional customers are leading the way.

A token-exposed platform that depends on trading volume and speculative demand awaits. The next three to six months will determine whether that window expands or whether 2026 becomes the year that only pick-and-shovel companies go public.