The NIGHT token outperformed the broader cryptocurrency market on Monday, December 29, after Charles Hoskinson suggested it could help expand decentralized finance (DeFi) across the blockchain ecosystem, including XRP.

Cardano’s partner chain, Midnight, is a privacy-focused blockchain built for confidential transactions and private DeFi, with NIGHT serving as the native token. Hoskinson is the co-founder of Ethereum and the founder of Cardano.

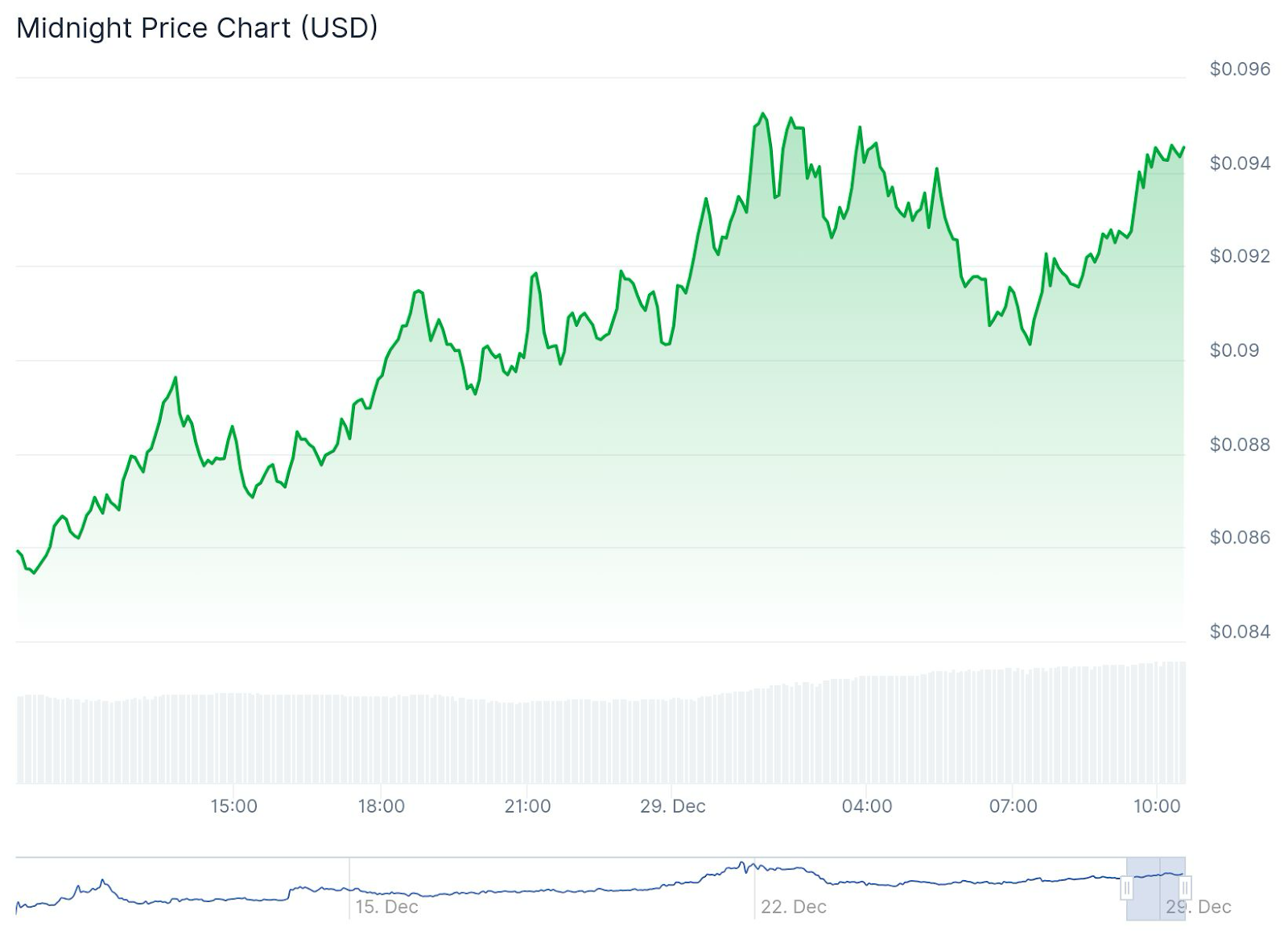

According to CoinGecko, NIGHT has risen over 11% in the past 24 hours. The rally came after Hoskinson said in a post on X that adding Midnight to the XRP ecosystem would “blow traditional banks out of the water.”

“Adding Midnight to Bitcoin will enable the world Satoshi envisioned. Adding Midnight to Cardano will significantly strengthen our DeFi ecosystem, increasing our MAUs, transactions, and TVL by 10x as we are the first to bring private DeFi to market at scale,” Hoskinson said in the same post.

NIGHT’s rise comes amid a broader market decline today, with BTC currently down 1% to $86,000. XRP also fell 0.6% in the past 24 hours to $1.85, while Cardano’s native token ADA also fell 3.4% to around $0.35.

Focus on privacy

NIGHT’s move comes amid a recent uptick in privacy-focused crypto assets and infrastructure. Tokens like Zcash have soared in recent months as traders migrated to assets that offer on-chain confidentiality.

Meanwhile, regulators and industry leaders have become increasingly vocal about confidentiality and how it is key to increasing the adoption of cryptocurrencies. Earlier this month, U.S. Securities and Exchange Commission (SEC) Commissioner Hester Peirce said during the SEC’s Cryptocurrency Roundtable that privacy should be treated as a normal part of financial activity, rather than a sign of wrongdoing.

“Protecting privacy should be the norm and not an indication of criminal intent,” Peirce said in his speech. “Governments should resist the temptation to coercively intervene to provide a regulatory beachhead or facilitate financial oversight.”

Meanwhile, the Roman Storm case earlier this year, in which Storm was found guilty of operating an unauthorized money transfer operation related to the Tornado Cash mixer, highlighted the legal risks facing privacy-focused crypto developers.