On March 31, Moody’s assigned a provisional Ba2 rating to Waverose Finance Project’s taxable revenue bonds of up to $100 million. The bond is secured by a loan to NH CleanSpark Borrower Trust 2026-1 with Bitcoin (BTC) as collateral.

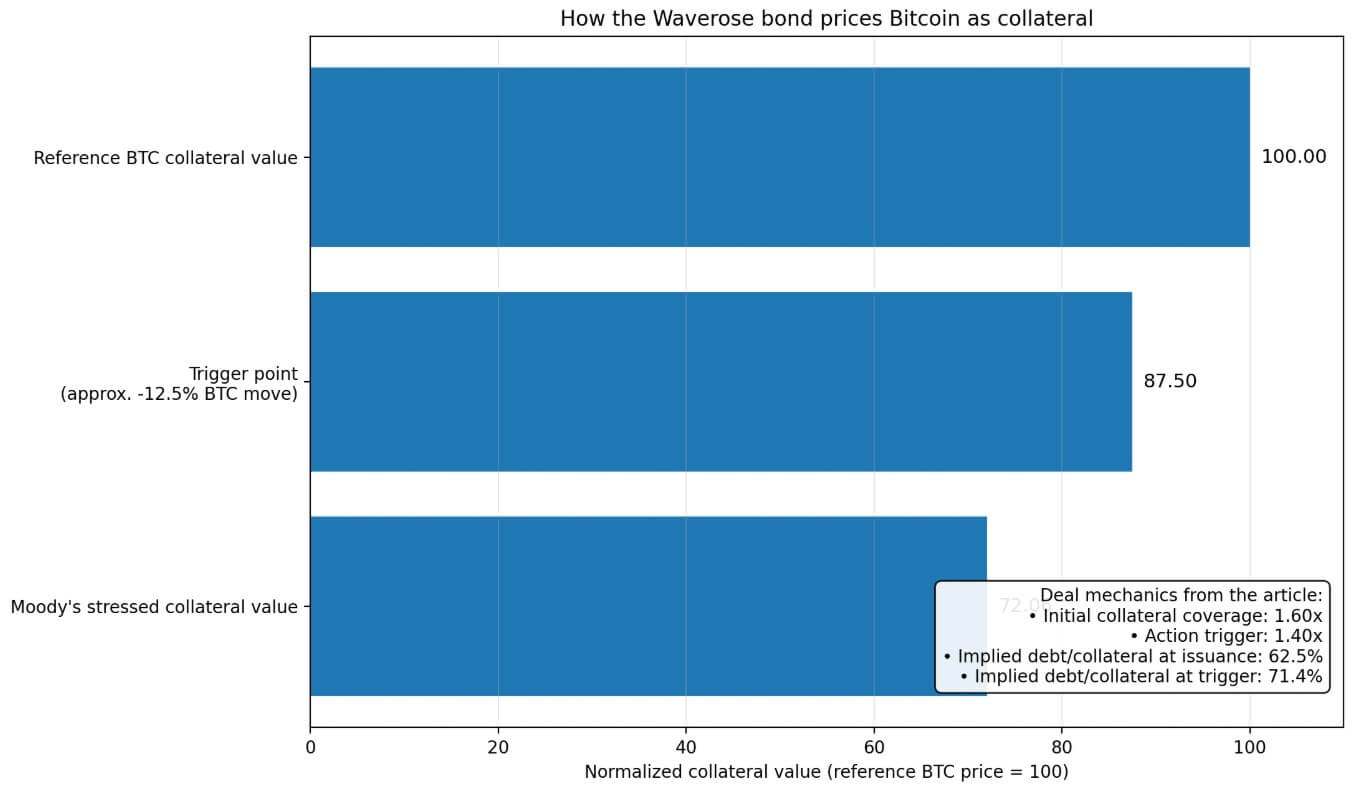

These numbers set the terms on which traditional finance agreed to work with Bitcoin. That means a credit of 72.06 cents per dollar of collateral value, a two-day exposure window that affects price movements, and an initial collateral coverage of 1.60x (which forces action when it drops to 1.40x).

Bitcoin has spent years validating its legitimacy as a store of value, corporate financial reserve, and ETF asset. New Hampshire’s agreement lists Bitcoin as collateral.

Collateral is where an asset gets credit utility, something a financial institution can borrow against an internal structure that credit markets can understand, price, and liquidate quickly if necessary. That’s the line Bitcoin just crossed.

Why this is important: This is the first time that Bitcoin has been officially translated into trust terms that the public market can understand. Currently, BTC is not held or traded, but instead is assigned a borrowing value, liquidation threshold, and stress price, turning it from an asset into available financial collateral. This change not only opens up new sources of liquidity for holders, but also introduces a system where price declines trigger automatic sales across multiple structures simultaneously.

Trust opening price

Waverose’s structure is a taxable conduit income bond.

New Hampshire’s role ends as a conduit, with bondholders assuming all risk of loss. This is institutional plumbing with limited resources.

This structure reveals two things. First, keep the risk isolated. If the collateral defaults, the bondholders absorb the loss. Second, it shows the exact conditions under which traditional finance decided that Bitcoin could enter the trust system.

If the initial collateralization ratio is 1.60x, the bond will start with debt equal to approximately 62.5% of the collateral value. A 1.40x trigger for automatic action to be triggered means approximately 71.4% debt.

This structure reaches a wire trip when BTC falls approximately 12.5% from its issue price. This is a move that Bitcoin performs on a daily basis.

Moody’s emphasized that the collateral value is 72.06% of the market value. Mapping Bitcoin’s April 1st price to the $68,000 zone, the stress zone reaches around $49,600.

Standard Chartered puts Bitcoin’s short-term bear market at $50,000, and the traditional financial firm has adjusted Bitcoin’s first public financial haircut almost exactly on a downside trajectory that one of the world’s largest banks believes is still within reach.

From ownership to pledge

New Hampshire arrived alongside two other recent movements in the same direction.

In February, S&P issued its first-ever rating on a structured finance transaction backed by Bitcoin. The transaction is Ledn Issuer Trust 2026-1, with a loan amount of approximately $199.1 million secured by 4,078.87 BTC, resulting in a fair market value of approximately $356.9 million and an opening LTV of approximately 55.8%.

In March, Better and Coinbase launched what they called the first crypto-backed mortgage. With this mortgage, the borrower pledges $250,000 in BTC for a $100,000 down payment, and the first lien remains backed by Fannie Mae.

Bitcoin received three credit wrappers in about six weeks, each with different haircuts, liquidation mechanisms, and regulatory constraints. Together, they describe the process by which Bitcoin enters credit markets through multiple doors at once, and those doors inch closer to normal household finances.

| structure | date | wrapper type | Collateral/pledge | Haircut / Rationale | who takes the risk | why is it important |

|---|---|---|---|---|---|---|

| Wave Rose / New Hampshire | March 31, 2026 | Taxable Conduit Revenue Bonds | Bitcoin pledged as collateral for bonds secured by loan to NH CleanSpark Borrower Trust 2026-1 | Moody’s emphasized collateral because 72.06% of market value; 1.60x Initial collateral range. Action triggered by 1.40x;The transition from implicit debt to collateral begins 62.5% and rise 71.4% When triggered | Bondholders absorb losses if the collateral fails. New Hampshire Public Funds Not Committed | Indicates the entry of Bitcoin Credit adjacent to public finance Not just as an owned asset, but as rated collateral |

| Ledn Publisher Trust 2026-1 | February 2026 | Structured Finance / ABS | almost $199.1 million loan secured by 4,078.87BTC Fair market value is approximately $356.9 million | About LTV of 55.8% At the start | Investors in structured finance transactions. Risks related to collateral, operations and clearing mechanisms | Indicating the entry of Bitcoin Rating Structured Finance |

| Better / Coinbase Mortgage Products | March 2026 | Compliant mortgage loan/down payment loan with cryptocurrency collateral | Borrower’s pledge $250,000 in BTC to get $100,000 The first lien continues to be backed by Fannie Mae while the loan is taken out as a down payment on the home. | An example is Advance payment rate 40% About promised BTC | The risks are in the crypto-backed loan structure, but the first mortgage remains individually conformed/fanny-collateralized | Push Bitcoin Collateral Something closer to household finances And mainstream mortgage plumbing |

The U.S. municipal market has $4.4 trillion in outstanding debt outstanding as of Q4 2025. Households hold 48% directly and about 21% through mutual funds.

Munis occupy a particular psychological slot in America’s savings culture, sitting where advisors park their money for clients looking for safety alongside tax efficiency.

Waverose bonds are placed in the tax conduit corner. Taxable municipal issuance was only about $33 billion in 2025, less than 6% of the total market. The transaction was valued at $100 million, representing approximately 0.0023% of the outstanding Muni market.

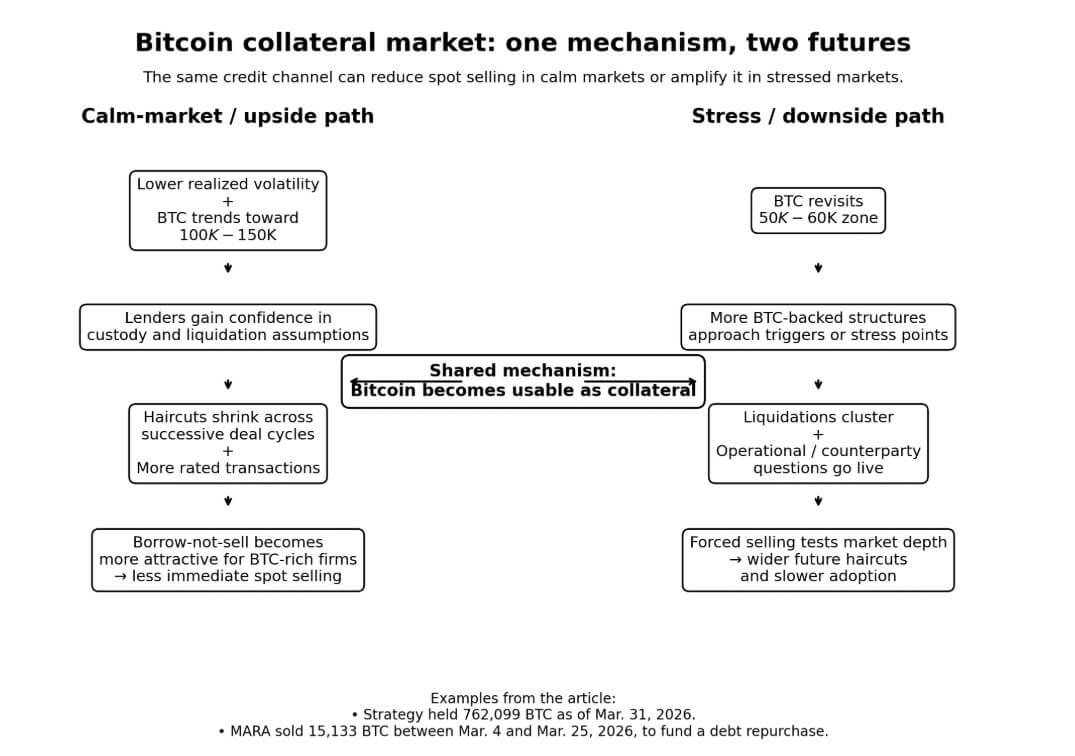

One mechanism, two possible futures

For Bitcoin holders and treasury-focused companies, collateral utility decreases in opposite directions as the price moves.

Strategy held 762,099 BTC as of March 31st. From March 4th to March 25th, MARA sold 15,133 BTC for approximately $1.1 billion to fund debt repurchases, an outright spot sale to cover debt on its balance sheet.

A functioning BTC collateral market sits between two postures: fully funded and fully liquidated, providing credit against reserves that allow holders to raise capital while maintaining their Bitcoin positions.

In March, Fidelity noted that public companies and ETFs together hold about 12% of Bitcoin’s circulating supply, and that 2025 was Bitcoin’s lowest volatility year on record, based on annualized realized volatility.

If that holds and Bitcoin trades towards the $100,000 to $150,000 range Bernstein predicted for late 2026, the collateral channel becomes truly attractive. BTC-rich companies hold larger reserves with lower realized volatility, lenders build confidence in their liquidation assumptions, and the haircuts required to access credit shrink over successive trading cycles.

Each rated transaction adds data to Bitcoin’s nearly empty track record as pledged collateral. Second trade, third trade, cluster and trust pricing starts to compress.

The bare case runs in the opposite direction on the same mechanism. Operational questions become real as Bitcoin revisits $50,000, close to Standard Chartered’s downside forecast and close to Moody’s stress zone from current prices.

Companies begin to wonder if the liquidation mechanism will work properly if all BTC-backed structures need to be exited at once.

S&P’s Ledn ABS rating work identified operational risk, counterparty risk, event risk, and liquidation mechanisms as core uncertainties of Bitcoin-backed credit. The report noted the market’s ability to absorb forced selling due to multiple structures firing triggers within the same price range.

Structures that reduce forced selling in calm markets may concentrate forced selling in turbulent markets. This is the inherent shape of collateralized credit, and Bitcoin’s volatility makes that shape more pronounced than with traditional collateralized assets.

The first version of Bitcoin-backed public finance is small-scale, speculative-grade, and built for the taxable conduit space. The architecture has constraints because those constraints are the only conditions on which the credit system is concerned.

What Moody’s announced on March 31st was the pricing schedule for Bitcoin to enter the credit market, or the conditions it would set for bond investors to accept Bitcoin as collateral.

Future deals will be negotiated based on that timeline, tightening haircuts if volatility falls, widening haircuts if it rises, testing various custody arrangements, and moving toward investment-grade boundaries.

Each iteration adds institutional memory to a market that currently has almost none.

It took years for Bitcoin to become available for institutional purchase through regulated channels. Their becoming a bankable entity follows the same logic of gradual and conditional growth, built on accumulated performance.

(Tag translation) Bitcoin