Cryptocurrency companies have spent years trying to gain direct access to the plumbing of the U.S. financial system. The Kraken ended up being the first to get it.

The decision could reshape the way digital asset companies move funds and interact with the traditional financial system, reducing their dependence on partner banks.

What actually is a Fed Master Account

The master account is essentially a gateway to the Federal Reserve’s payments infrastructure. Banks and certain regulated financial institutions use these accounts to store reserves with central banks and settle payments through systems such as Fedwire.

Instead of routing transactions through intermediary banks, financial institutions with master accounts can send and receive funds directly within the Fed’s network.

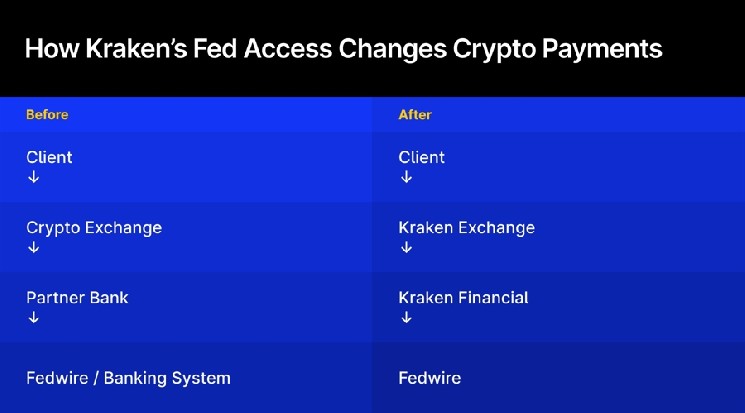

Until now, crypto companies typically relied on partner banks to move US dollars between exchanges, customers, and other financial institutions. This arrangement created operational risks. If a banking partner withdraws from crypto exposure, trading platforms could lose access to key payment channels almost overnight.

Using a master account, Kraken Financial can connect fiat currency flows directly to the Fed’s payment rails, potentially making dollar transfers faster and more predictable for institutional investors and professional traders.

Not full banking privileges

Despite the importance of approval, Kraken does not enjoy the same privileges as traditional commercial banks. The access given to Kraken Financial is similar to what policymakers have described as a “skinny” or limited master account model, where companies can use the Federal Reserve’s payment rails but not the full range of central bank services available to banks.

What the Kraken Gets and What It Doesn’t Get

In practice, this means the Fed is allowing access to infrastructure without extending the broader safety net that comes with full banking.

Why structure matters

The restricted access model reflects the Federal Reserve’s cautious approach to institutions operating under new or specialized charters.

Kraken Financial operates under the Wyoming Special Purpose Depository Institution (SPDI) framework, a type of bank charter designed specifically for digital asset companies. SPDI focuses primarily on storage and payment services rather than traditional lending.

Because these institutions operate differently than traditional banks, regulators have developed a risk hierarchy framework to determine what level of access to the Fed’s infrastructure is appropriate.

Granting restricted master accounts would allow the Fed to test how fintech and crypto companies interact with payment systems while maintaining tighter controls over liquidity and systemic risk.

(#Highlighted link#)

The long battle for access

Cryptocurrency companies have been seeking direct access to the Federal Reserve’s infrastructure for years. The industry argues that denying such access would force digital asset companies to rely on a small number of “crypto-friendly” banks, concentrating risk and making the sector vulnerable to sudden disruption.

These concerns were further intensified after the 2023 collapse of Signature Bank and Silvergate Bank, which served as major banking partners for crypto companies. Their failure disrupted major payment networks used by exchanges and institutional investors.

From an industry perspective, being able to connect directly to the Fed’s payment rails could reduce dependence on intermediary banks and stabilize the flow of fiat currency in and out of digital asset markets.

Why banks are concerned

Traditional banking groups have strongly opposed efforts by crypto companies to acquire master accounts. Industry groups argue that crypto companies do not operate under the same regulatory framework as commercial banks and may pose higher risks regarding anti-money laundering controls, operational resilience, and financial stability.

The Independent Community Bankers of America (ICBA) expressed similar concerns after Kraken’s approval. The group warned that giving virtual currency companies and other nonbank institutions direct access to Federal Reserve accounts could pose risks to the banking system.

“Granting non-bank entities and crypto institutions access to master accounts that have traditionally been limited to highly regulated, insured depository institutions poses risks to the banking system,” said ICBA President and CEO Rebecca Romero Rainey.

We are very concerned about Kraken Financial’s master account approval. Allowing nonbank entities access to master accounts that have traditionally been limited to highly regulated, insured depository institutions creates risks for consumers and the banking system. https://t.co/Wng93QV5iA

— Independent Community Bankers of America (@ICBA) March 4, 2026

Banking lobby groups have also questioned the transparency of the approval process and the safeguards in place in the Kraken case. Beyond compliance concerns, there is also a competition aspect.

If crypto companies gain direct access to central bank payments infrastructure, banks could lose some of their traditional role as intermediaries between digital asset platforms and the dollar-based financial system.

Wider regulatory changes

Kraken’s approval comes amid broader policy changes in the United States aimed at integrating parts of the cryptocurrency industry into the regulated financial system.

Recent moves include a proposal to give fintech companies limited access to the Federal Reserve’s payments system and approval for cryptocurrency companies to form a national trust bank focused on custodial and digital asset services.

The initiative suggests that regulators are looking for ways to connect crypto infrastructure to traditional finance without giving the industry full banking status.

What does that mean for the market?

For Kraken itself, the master account strengthens its infrastructure position. Direct access to the Fed’s payment rails could allow exchanges to offer faster fiat payments, reduce dependence on partner banks, and improve services for institutional clients such as trading houses and hedge funds.

Faster dollar settlements could also be particularly important for OTC desks, prime-style brokerage services, and liquidity providers operating in digital asset markets. More significant developments set a precedent for the broader industry.

If Kraken’s arrangement proves viable from a compliance and operational perspective, other crypto institutions with bank-style terms could pursue similar access. This could gradually reshape the way digital asset companies connect to dollar payment systems.

At the same time, the limited nature of this account highlights the vigilance of regulators. Cryptocurrency companies may gain access to some of the core infrastructure of the financial system, but they will not necessarily enjoy all the privileges enjoyed by traditional banks.

For now, Kraken’s master account represents more of a controlled experiment than a wholesale change in policy. But if the model takes hold, it could serve as a blueprint for how digital asset companies connect to the core infrastructure of the U.S. financial system.