With tensions in the Middle East rising and oil prices soaring above $100, the question for the Bitcoin network and miners is not whether the price of electricity will go up, but whether the price of Bitcoin will go down.

While the direct impact of oil price shocks on mining costs is likely to be limited, broader macroeconomic implications could weigh more heavily on the industry, according to a study of Bitcoin mining software and services company Luxor’s Hash Rate Index.

However, the impact of soaring oil prices on the Bitcoin network is not zero.

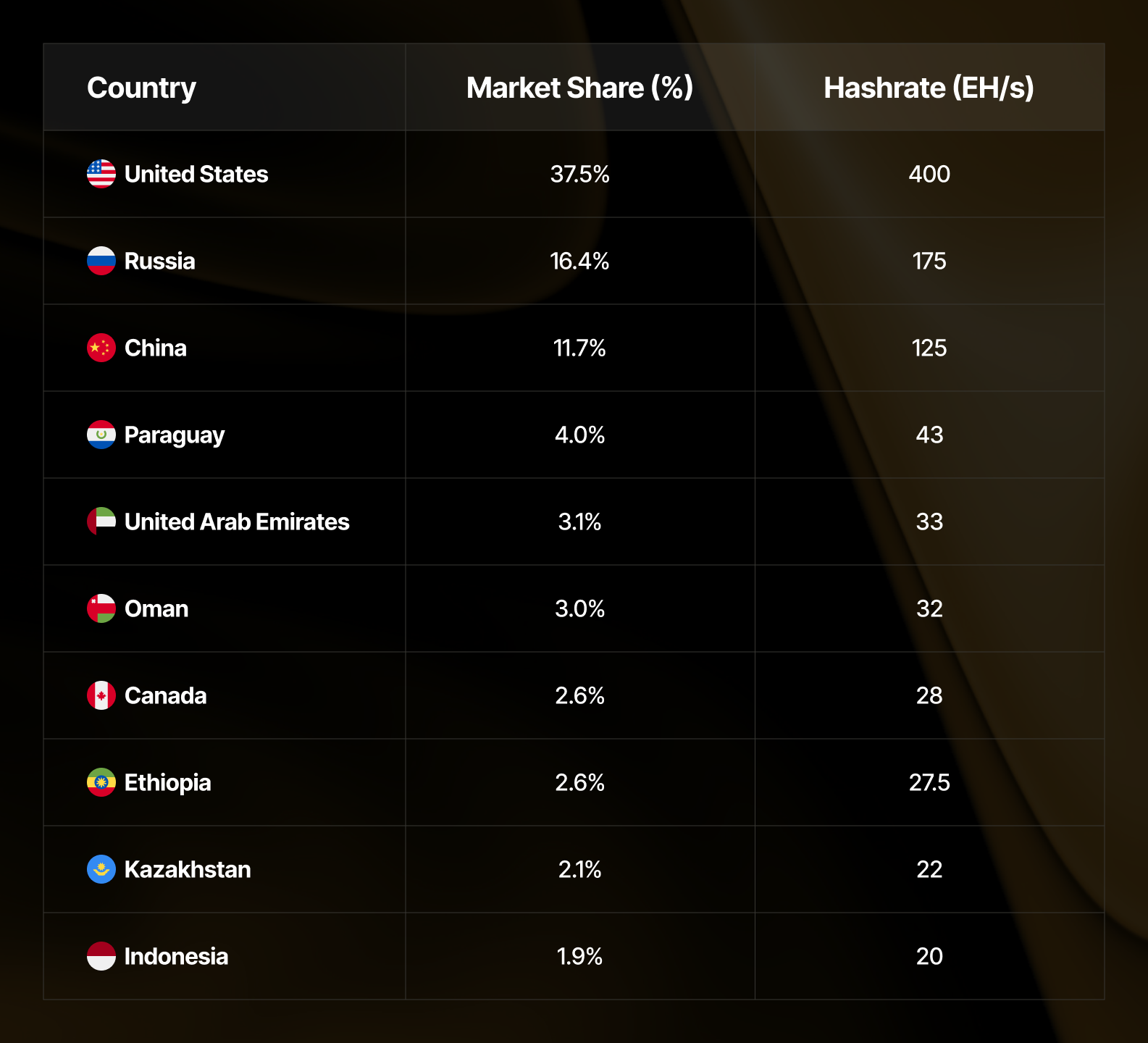

Luxor estimates that around 8-10% of the global Bitcoin hash rate is operated in the electricity market, and electricity prices are closely linked to oil prices. These operations are primarily concentrated in Gulf states such as the United Arab Emirates and Oman, with smaller contributions from Iran, Kuwait, Qatar, and Libya.

The “truly oil-exposed countries” are the Gulf states, Luxor wrote in a research report, adding that the UAE and Oman together account for about 6% of the network’s computing power, or hashrate.

“These power grids run primarily on natural gas derived from oil production, and electricity prices track crude oil more directly than in the United States or Russia,” the report said.

Meanwhile, Iran is estimated to hold an additional 0.8%, and other smaller contributors such as Kuwait, Qatar, and Libya bring the total exposure of the oil-sensitive hashrate to around 8-10% of the network.

Top countries supporting the Bitcoin network in Q1 (hashrate index)

The remaining approximately 90% of the network operates in regions where electricity prices are driven by natural gas, coal, hydropower, and nuclear energy. This means that fluctuations in oil prices have little direct impact on extraction costs.

Impact on mining

What does this mean for Bitcoin miners, who run power-hungry machines to secure the network and verify transactions?

Luxor argues that even if oil prices remain above $100 per barrel, the impact on the mining economy from higher power costs is likely to be limited to a small portion of its network. The biggest input cost for mining Bitcoin is electricity.

Rather, the greater risk for miners lies in how geopolitical shocks affect the price of Bitcoin. According to Luxor, periods of macro stress often trigger risk-off behavior in financial markets, which can put pressure on volatile assets such as Bitcoin.

Hash price, a measure of miner profitability, fell to an all-time low of $27.89 per petahash per day in February, according to recent data cited by the company. This is mainly due to the 23.8% drop in Bitcoin price over the same period.

Luxor concludes that for miners, profitability is much more sensitive to changes in Bitcoin prices than to changes in electricity costs.

Read more: Bitcoin hashrate drops 12%, worst drawdown since China mining ban: CryptoQuant