The two-week conditional ceasefire between the United States and Iran forced a rapid rewriting of Strait of Hormuz trade, but it did not fully restore the pre-war macro environment.

Oil plummeted from its panic highs, global stocks rose, and Bitcoin rallied along with it. This is a clear break from the pre-ceasefire view that markets had given up on restarting the economy in the short term.

What has changed is the primary direction of energy. What remains unresolved is the path to normalizing the flow of goods, insurance, shipping, and inflation.

JPMorgan, UBS and US government energy forecasters are still explaining delays in the repair process under the heading of a ceasefire. Their work can no longer be read as a viable argument against any reopening. He warns that reopening and normalization are two different things.

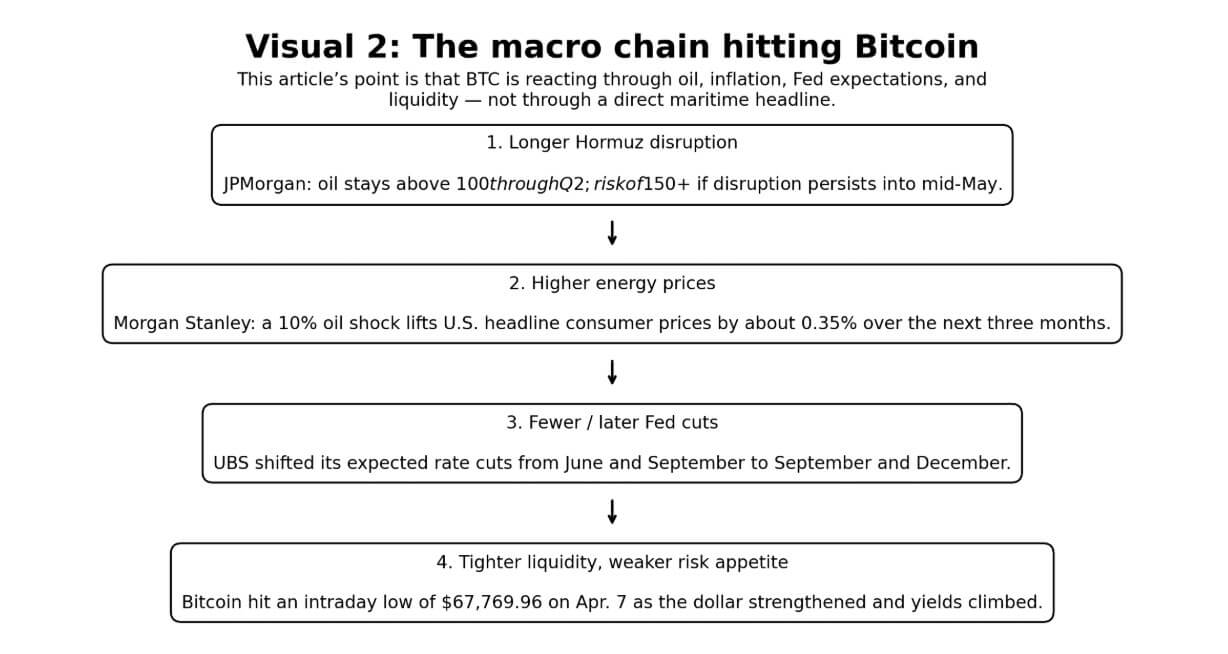

JPMorgan’s base case for oil prices remains elevated through the second quarter, and it warns that oil prices could rise above $150 if the turmoil escalates again or lasts until mid-May.

UBS expects the conflict to subside, but says it will take a significant amount of time for production to return to pre-conflict levels due to infrastructure damage.

The EIA says oil flows through the Strait of Hormuz will be fully restored once the conflict ends.

None of these three organizations talks about a complete recovery of the plumbing in the energy market, which is currently at the heart of the market. The ceasefire reduced immediate tail risks. Normal freight movement, normal inventory, or normal inflation pass-through is not yet guaranteed.

The Strait of Hormuz transported 20.9 million barrels per day in the first half of 2025, accounting for about 20% of global oil liquid consumption and a quarter of total seaborne oil trade. It also handled 11.4 billion cubic feet of LNG per day, representing more than 20% of global LNG trade.

US intelligence agencies assessed on April 3 that Iran demonstrated in the strait that control of global energy flows is a key card for the Iranian government.

While this assessment was more important pre-ceasefire than it is now as a market direction, it remains important as a structural reminder that formal détente does not automatically produce frictionless free navigation.

| institution/actor | Current timeline/base case | Major predictions/evaluation | What it means for oil | its impact on the market |

|---|---|---|---|---|

| JP Morgan | Although the ceasefire reduces immediate tail risks, disruption risks persist into the second quarter. Partial normalization remains base path | Oil prices may continue to rise into the second quarter and could rise above $150 again if the unrest continues into mid-May or the ceasefire fails. | Oil may not quickly return to pre-shock prices and may fall from panic highs | Reassurance has now returned, but inflation and pressure to cut interest rates could persist. |

| UBS | Conflict may subside in coming weeks, but recovery will last much longer | Due to infrastructure damage, it will take a significant amount of time to return production to pre-conflict levels. | Energy market loosens before normalizing | Risk assets will recover first, followed by macro normalization, if any. |

| EIA | Even after the conflict ends, complete recovery will take several months. | Flows, routes, and outputs are slowly normalized. Retail fuel pain remains | Oil and fuel prices likely to remain high even after nominal economic reopening | Consumer price pressures continue beyond ceasefire headlines |

| US intelligence agency | Iran still views chokepoint control as a strategic tool | Iran sees energy flow control as a core negotiation tool | Decreased confidence in smooth reopening | Markets maintain geopolitical risk premium even under bailouts |

| Background to the ceasefire | Risk of immediate escalation has been reduced, but durability has not yet been proven | Markets may price in reopening sooner than the transportation system normalizes | Crude oil will be the first to lose its panic premium. Physical pressure can last a long time | The rescue rebound in risk assets is justified, but complete macro clearness has not yet been confirmed. |

The crude oil spot market remains a place to watch whether the reopening normalizes. Although the ceasefire has softened the headlines, instant cargo prices, insurance terms and route frictions remain more informative than last month futures alone.

Earlier this week, North Sea Forties crude oil reached $146.09 a barrel, dated Brent reached $141.365, and some immediate cargoes traded above $150, while European jet fuel hit $226.40 and diesel $203.59. At the peak of the panic, North Sea Brent futures prices were near $110.

The gap between instant spot and headline futures screens remains a site of inflationary transmission.

Morgan Stanley Consumer Calculations show that a 10% rise in oil prices due to a supply shock would push up headline U.S. consumer prices by about 0.35% over the next three months, causing real consumption to begin to weaken and remain depressed for the next five to six months.

EIA’s April outlook calls for U.S. gasoline prices to average more than $3.70 in 2026, with diesel prices peaking above $5.80 and averaging $4.80 a year.

macro chain

Bitcoin trading is still driven by oil, then inflation, then Fed policy, and then risk appetite. The difference after the ceasefire is that the chains have loosened. Not broken.

Bitcoin hit an intraday low of $67,769.96 on April 7th, when the oil crisis, a strong dollar, and rising government bond yields weighed on the market’s overall risk appetite.

Since the ceasefire, BTC has rallied along with stocks as traders downplay the likelihood of the worst energy spiral looming. The move makes sense. The next question remains unsettled: whether the headline low oil prices will lead to a lasting easing of inflationary pressures and interest rate expectations.

Earlier this year, BTC crossed $70,000 as , and the same logic is playing out again. For now, the liquidity situation and the liquidity situation are still determining the price of energy.

UBS has raised its expectations for Fed rate cuts from June and September. Increased America’s potential. IMF chief Kristalina Georgieva said inflation forecasts would rise even if a quick solution was put in place.

Economists at the Dallas Fed in the Strait of Hormuz predicted that the average price of WTI would rise to $98 in the second quarter, depressing global real GDP growth by 2.9 percentage points annually in the quarter. The second quarter’s disruption will push WTI to $115 in the third quarter, and the third quarter’s disruption will push it to $132 by year-end.

Its modeling currently works best as a risk map for a failed ceasefire or incomplete normalization, rather than as an actual base case. The market has retreated from a pure closure scenario. A complete return to the pre-conflict macro situation is not yet factored in.

As a result, the question of rate cuts has changed. Traders are no longer asking whether the oil shock is still intensifying. They are asking whether this relief will last long enough to reopen the Fed room before the end of the year.

When gasoline averages above $3.70 and diesel averages above $4.80, spending hits every sector of the real economy and financial conditions tighten long before the Fed takes formal action.

Possible scenarios

The base case has changed. It is no longer a complete market capitulation to a short-term resumption of trading. It is a ceasefire relief rally, with incomplete normalization beneath it.

The path in between remains important for Bitcoin, as falling oil prices will only help if it continues to be reflected in lower inflation pressures, stable growth expectations, and a more reliable rate cut path.

The bearish case is now going through an extended period where the ceasefire fails or shipping only partially resumes and the spot market continues to price scarcity. If the disruption maintains JPMorgan’s mid-May baseline, JPMorgan will return to the forefront of the market.

According to Dallas Fed modeling, WTI reached $115 in the third quarter after two quarters of closure. Morgan Stanley warns that even with a nominal restart, oil markets could continue to trade at a higher risk premium if Iran maintains structural control over cargo flows.

In the case of Bitcoin, that setup still maps to the clearest short-term downside path. Oil prices continue to rise, inflation expectations rise further, the Fed remains cautious, and risk assets lose out in bailout bids.

During the last acute risk-off episode, option demand was concentrated around the $60,000 to $50,000 downside strike. If the configuration deteriorates toward the pre-ceasefire stress path, retesting the range is again likely.

| scenario | oil results | inflation effect | Fed involvement | Impact on BTC | Main conditions to be aware of |

|---|---|---|---|---|---|

| Bearish case: ceasefire failure or chaos lasting longer than mid-May | Oil re-anchoring at very high levels. $150 return as working risk benchmark | Inflation expectations rise again | The Fed will suspend policy even longer. Expectations for interest rate cuts fade again | This is the strongest downside case in the short term. Lower range retesting becomes more realistic | Will the turmoil continue until mid-May at JP Morgan, or will the ceasefire break down? |

| Bull case: ceasefire is maintained and navigation is fully normalized. | Brent plummets towards pre-shock levels | Inflation shock will ease faster | Moderation of expectations returns more clearly | BTC rebounds along with stocks and broader risk assets | whether free navigation is restored, insurance is in place, and cargo flows quickly normalize; |

| Intermediate case: resume without normalization | Oil prices start to fall dramatically, but there is still a significant risk premium | Inflation cools only slowly | Fed offers limited relief but remains cautious | BTC only partially improves. The top price remains suppressed by persistent macro pressure. | Will reopening actually normalize flows, inventory, and pricing? |

| sticky aftershock incident | Physical flows improve, but fuel and supply routes will take months to normalize | Consumer price pressures continue even after subdued headlines | Financial conditions will remain tough until the Fed changes policy | Even after the headlines subside, BTC can’t clear everything instantly | Will gasoline, diesel and supply chain stress continue into the second half? |

The bull market remains tied to Morgan Stanley’s view that Brent crude could fall toward $70 if oil flows truly return to free, as global oil appeared to be in oversupply before the conflict began.

In this setup, the inflation shock will reverse faster, Fed easing will be back on the horizon, and Bitcoin will recover along with stocks. That is the logic that current relief rallies are trying to price.

The conditions remain decisive: true freedom of navigation is a requirement.

If the ceasefire leaves physical cargo movements restricted by security risks, insurance frictions, congestion, or operational controls, it will create a separate oil market, leaving part of the risk premium embedded and Bitcoin’s upward path remaining shrouded in the same inflationary headwinds.

The distinction between reopening and normalization is where institutional research is currently focused.

The EIA says that even if the war ends, it will take many months for transport to fully recover as supply routes and production normalize. Morgan Stanley says that after an oil shock of this magnitude, real consumption will remain sluggish for five to six months.

The important question for Bitcoin traders is no longer whether the market believes it will reopen. The key will be whether the overhangs in oil and inflation cool down quickly enough to restore expectations for rate cuts before the cease-fire premium fades.

(Tag to translate) Bitcoin