Bitcoin’s recovery to around $71,000 has reignited the familiar bullish conversation around price, liquidity, and positioning. It also exposed some not-so-pleasant facts within the network itself.

The fee market is barely moving.

For a market that still treats on-chain congestion as a sign of organic demand, that divergence is more noteworthy than a rehash of macro tailwinds or ETF flow continuity.

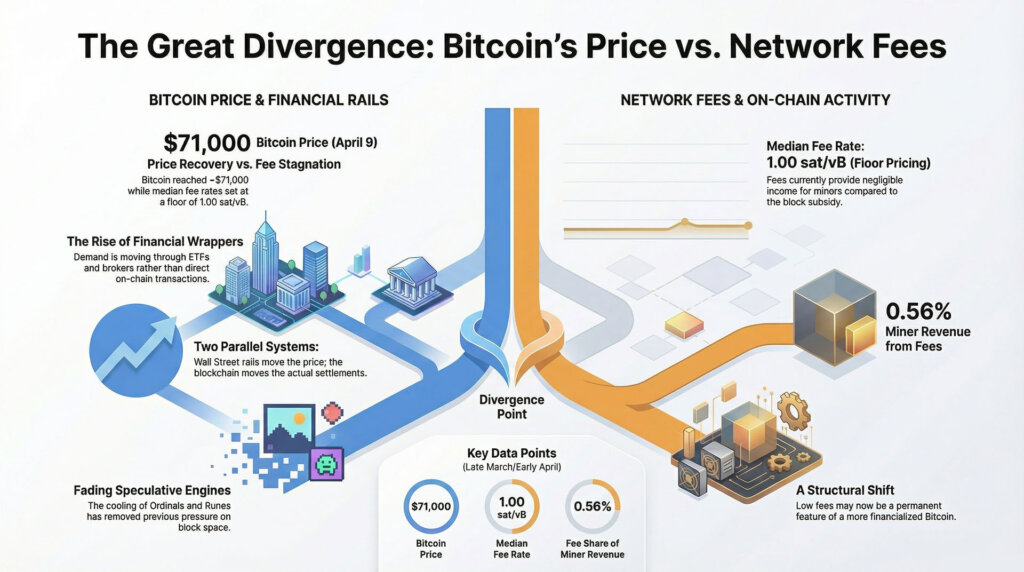

above crypto slate According to the Bitcoin price page, BTC last traded at $70,990 on April 9th, down 0.86% in 24 hours, up 6.11% in 7 days, and up 0.85% in 30 days.

Prices have clearly recovered from the lower end of the recent range, but the base tier still looks calm, cheap and uncrowded.

This disconnect tells us something important about where this movement is actually happening. Bitcoin demand is expressed more through financial wrappers, broker channels, and ETF rails than through users competing for block space on-chain.

Under that setup, the price movement could still persist. The signals sent are different.

A recent Bitcoin Blockspace report covering March 19th to March 26th found that the median fee rate started at 1.13Sat/vB and remained at 1.00Sat/vB for the rest of the week. In reality, that’s floor pricing.

Users were able to authenticate without paying for the missing space. The report counts the total fees across 1,028 blocks as just 18.03 BTC, or approximately 0.0175 BTC per block.

Even more surprising, these fees were only 0.56% of miner revenue for the week compared to the 3,212.5 BTC from subsidies.

Prices have recovered, but the fee market still looks half asleep

These numbers are unusually weak for a market trading around $71,000. Previous cycle logic had conditioned the market to expect Bitcoin price increases to coincide with crowded blocks, more competitive inclusion, and a fee market that would begin to rise without most people noticing.

That reflex still shapes how many crypto participants interpret demand. The current market is sending a different message.

Prices may recover even while on-chain urgency is subdued.

One reason the fee market seems so subdued is that Bitcoin has already lost one of the speculative demand engines that distorted the pricing of block space in earlier stages. Ordinal numbers and other inscriptions once caused tangible explosions of non-monetary demand, and the launch of runes temporarily caused the same on an even larger scale around the time of the 2024 halving.

That urge has faded considerably. The chain no longer deals with the traditional inscription-driven competition for block space. This means that today’s low-cost environment is not just about healthy efficiency and quiet user behavior.

This also reflects the absence of categories that previously inflated the number of transactions and weighed down fees.

This context helps explain why a BTC rally can coexist against the backdrop of such soft fees. Early in the cycle, ordinals, inscriptions, and later runes provided miners with an additional source of income and gave observers a reason to treat menpool stress as evidence of growing demand.

Now, that support appears to be much weaker. The speculative traffic that once crowded the chain has cooled, leaving Bitcoin to rely on organic payment demand or price-driven capital flows to do the heavy lifting.

In that sense, it’s also about what has already left the building.

Part of that dynamic comes from the fact that the pipes that carry demand have changed. Buyers using spot ETFs, broker products, or treasury vehicles can push capital into Bitcoin exposure without creating the same base layer footprint that users move coins directly on-chain.

This distinction is becoming more important as access to Bitcoin becomes more financialized. Pharcyde’s daily ETF flow data shows inflows of $471.4 million on April 6, followed by outflows of $159.1 million on April 7 and $124.5 million on April 8.

Although day-to-day fluctuations were relatively modest, the broader point is that flows through these wrappers remain an active transmission channel for demand. The Spot Bitcoin ETF recorded net inflows of $1.3 billion for the month, its first positive turn since October.

That is the mechanism behind the current divergence. Bitcoin demand is split between two systems.

One system drives prices across funds, advisor platforms, and broker access. The other system moves transactions through the blockchain itself.

The first system appears to be more active than the second system at this time. As a result, the fee market remains dormant even though the asset itself has regained its altitude.

The result is a rebound that looks bullish on screen, although the pricing of block space on the network itself remains subdued. This combination has a different meaning than a full chain revival.

This suggests that while direct pressure on Bitcoin’s payment layer remains limited, the recovery is spreading broadly through financial rails. For those who still treat menpool stress as a simple proxy for demand, the current setup is a reminder that the market structure around Bitcoin is changing faster than many of the instincts people still use to interpret it.

Glassnode’s April 1 Weekly Market Note said Bitcoin is in the $60,000 to $70,000 range, arguing that while spot demand is showing early signs of absorption, it still lacks the confidence needed for a sustained breakout. Glassnode also warned of dense overhead supply between $80,000 and $126,000.

This range framework fits well with the current divergence. Bitcoin has rallied, but the fee market has not repriced to indicate widespread urgency, widespread payment demand, or a sudden scramble for base layer access.

Low fees indicate where demand is reaching and miners are not yet receiving rewards

Another report, citing Glassnode data on March fee activity, said the 30-day simple moving average of daily Bitcoin transaction fees has fallen to 2.5 BTC per day in March 2026. The article states that this is the lowest level since March 2011.

The exact historical framework requires caution until directly checking the underlying major charts, but the directional message is consistent with the broader evidence. Fee conditions have become significantly stricter and remain challenging even as BTC regains momentum.

This compression creates an important gap between price strength and network monetization. Users get a more friendly chain. Miners receive little incremental revenue from transactional demand.

After the halving, subsidies now account for a greater proportion of the revenue mix than they did when they played an even larger role. The Blockspace report from March 19th to March 26th clearly quantified this issue, with fees contributing to just 0.56% of miner revenue that week.

For miners, the network’s internal revenue base remains largely unchanged, with rallies that do not trigger fee responses still contributing to price increases.

The difference becomes easier to understand when you think of Bitcoin as both an asset and a network, and each side expresses demand in different ways. On the asset side, you will benefit from ETF adoption, access to advisors, financial accumulation, and improved risk appetite.

The network side benefits from real users, money transfers, payments, and transactions competing for limited capacity. These two layers can reinforce each other.

Other times, we pull away for meaningful stretches. That’s where the market is now.

There are also practical points to the current setup. A calm mempool does not automatically turn into a weak Bitcoin.

This suggests that the rebound has less evidence of a return to on-chain intensity than the price alone suggests. Base layer fee responses would indicate that funding needs spill over into actual settlement disputes.

Without that response, another interpretation moves closer to the center. The interpretation is that Wall Street circulation is doing more direct lifting than users transacting natively on-chain.

This external collision gives explanatory power to the current divergence. Bitcoin is increasingly integrated into mainstream financial plumbing.

Morgan Stanley just launched a low-fee spot Bitcoin ETF, and Charles Schwab is preparing for direct spot trading of Bitcoin and Ethereum by mid-2026. The access channels surrounding Bitcoin continue to expand.

As the width widens, price can move along the rails long before the menpool signals a similar demand pulse.

The next test will be whether fee markets, miner revenue mix, and price strength will spill over into actual demand for payments.

The question at hand is whether the current divergence is temporary or structural. There are credible arguments on both sides, and the range of plausible outcomes should narrow in the coming weeks.

The first pass is a continuation of the current pattern. ETF and broker demand continues to support prices. Bitcoin remains near the high end of its recent range, with fee rates remaining near the low end.

This would strengthen the view that this rebound is driven primarily by wrapper-driven flows rather than a widespread recovery in native transactional demand. It would also strengthen the idea that prices can recover through distribution and access to capital while the chain’s own fee market remains calm.

The second path is to catch up in block space demand. Once the price recovery begins to spill over into actual trading competition, the market should start to see rising fee estimates, deepening backlogs, sustained pressure on menpools, and an increasing proportion of fees in miner revenue.

That change will change the interpretation of the rally. This suggests that this movement extends from exposure to use, which would give recovery a different kind of durability.

In the third pass, the current divergence looks more like a warning than a curiosity. If ETF flows reverse again, prices return to the lower half of Glassnode’s recent range, and fee conditions remain weak, the market will have a stronger case for treating this pullback as a positioning move that never developed into widespread trading demand.

In this configuration, mempool’s quietness no longer seems like a coincidence, but starts to look diagnostic.

The fourth path is closer to miner economics than price direction. If miners continue to operate in a post-halving environment and fees remain this suppressed, attention will shift to how the network is monetized.

CoinShares’ Q1 2026 Mining Report states that the final quarter of 2025 will be the toughest quarter for miners since the halving in 2024, with sharp price declines and near-record hash rates compressing margins. If prices remain low for an extended period of time, the pressure will become even more concentrated.

Higher prices will help, but broader fee contributions will help even more.

That’s why the fee market deserves to be placed closer to the center of the current Bitcoin discussion. A move back toward $71,000 makes sense.

There are also unanswered questions. Where exactly is demand materializing?

The most likely answer at the moment is that demand in financial products is materializing faster than in the block space of Bitcoin itself.

This has cautious and important implications for how this market should be understood. This rebound is gaining momentum through the channels Bitcoin has spent years trying to enter: funds, advisors, brokers, and mainstream portfolio plumbing.

Blockchain itself has not yet shown similar urgency in pricing access. For those who view Bitcoin as both a financial asset and a network, that gap is a signal.

The market rose further. The chain hardly flinches.

The next piece of evidence will come from whether that tranquility is finally broken, or whether Bitcoin’s most powerful demand engine lives on one layer removed from Bitcoin itself.

(Tag translation) Bitcoin