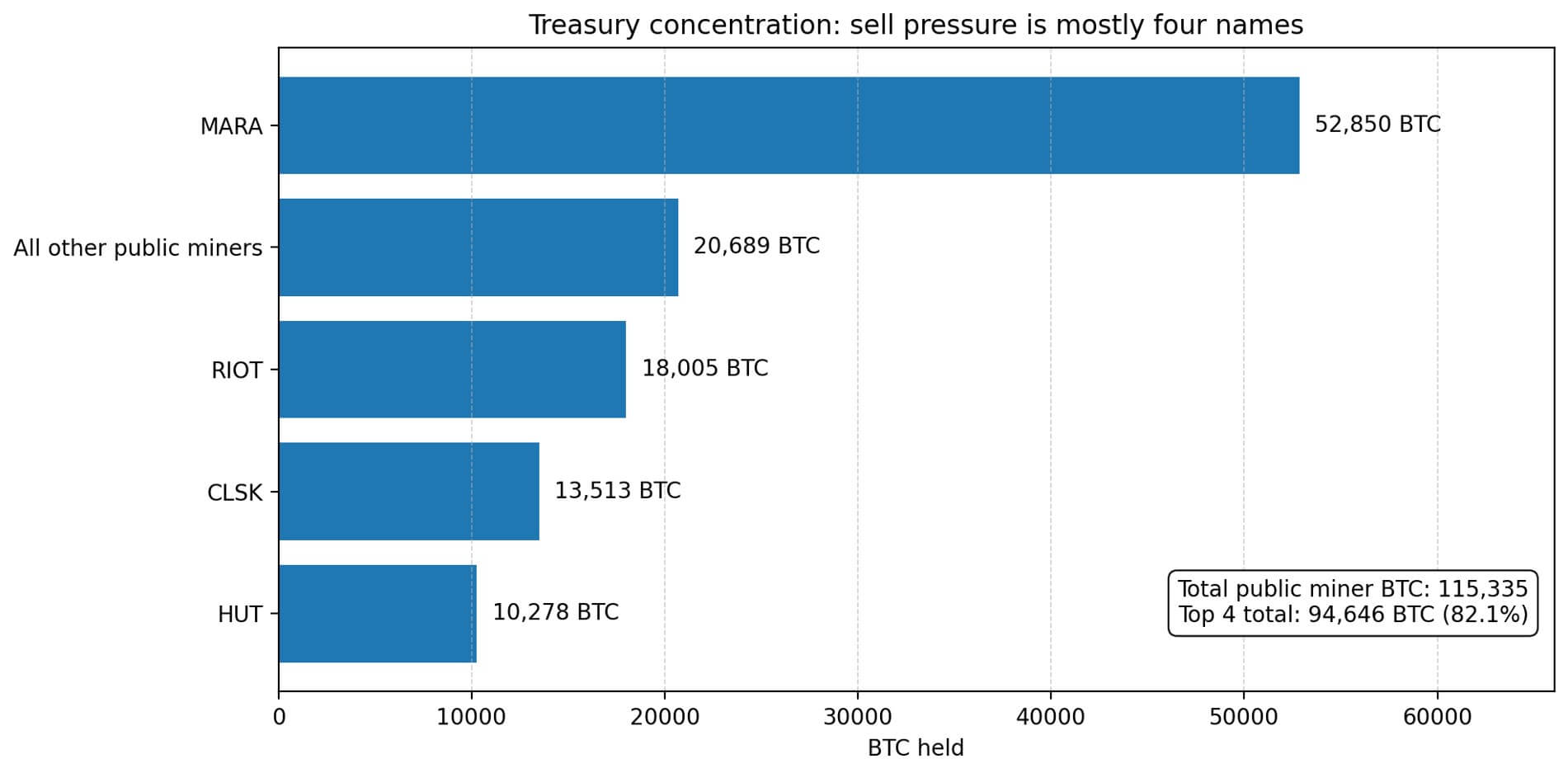

Public Bitcoin miners have a total of 115,335 people $BTC As of February 20, its treasury, worth about $7.4 billion at recent prices, has fallen 4.44% month-on-month, marking the first sustained contraction since miners began stockpiling the coin as a balance sheet asset.

This decline was no accident. Riot platform sales 1,818 $BTC Sold in December 2025 for a net profit of $161.6 million. Bitdeer sold $189.8 and liquidated its entire treasury. $BTC Mining and dumping 943.1 $BTC Funded from reserves to fund the transformation of the AI infrastructure, backed by $300 million in convertible notes.

This pattern suggests that miners’ finances are shifting from strategic reserves to working capital, and timing is critical.

The market suggests a hash price of around $28.73 per petahash per day over the next six months, a level that would make older mining fleets uneconomical and force operators to choose between selling Bitcoin, diluting equity, or raising expensive debt.

This setting compresses the minor margin in multiple directions. Block subsidy will be reduced to 3.125 due to Bitcoin halving in April 2024 $BTCthe number of coins issued per day decreased to about 450 coins. $BTC. CoinShares states that fees are “critically less than 1%” of a miner’s total revenue, so transaction fees are now effectively zero to miners’ revenue.

The mining difficulty increased by about 14.73% on February 19th to about 144.40 Tehash, while the hash price fell below $30 per Petahash per day.

VanEck’s mid-February 2026 analysis flagged the Antminer S19 XP as uneconomical above approximately $0.07 per kilowatt-hour under current conditions.

Riot’s Q3 2025 metrics demonstrate this tightness. The company’s cost to mine one Bitcoin was approximately $46,000 excluding depreciation, but $89,000 including capital equipment writedowns.

With Bitcoin trading in the mid-$60,000 range for parts of early 2026, the gap between all-in cost and spot price has narrowed to the point where a treasury sale becomes a reasonable form of liquidity management.

Government bond as new issue date

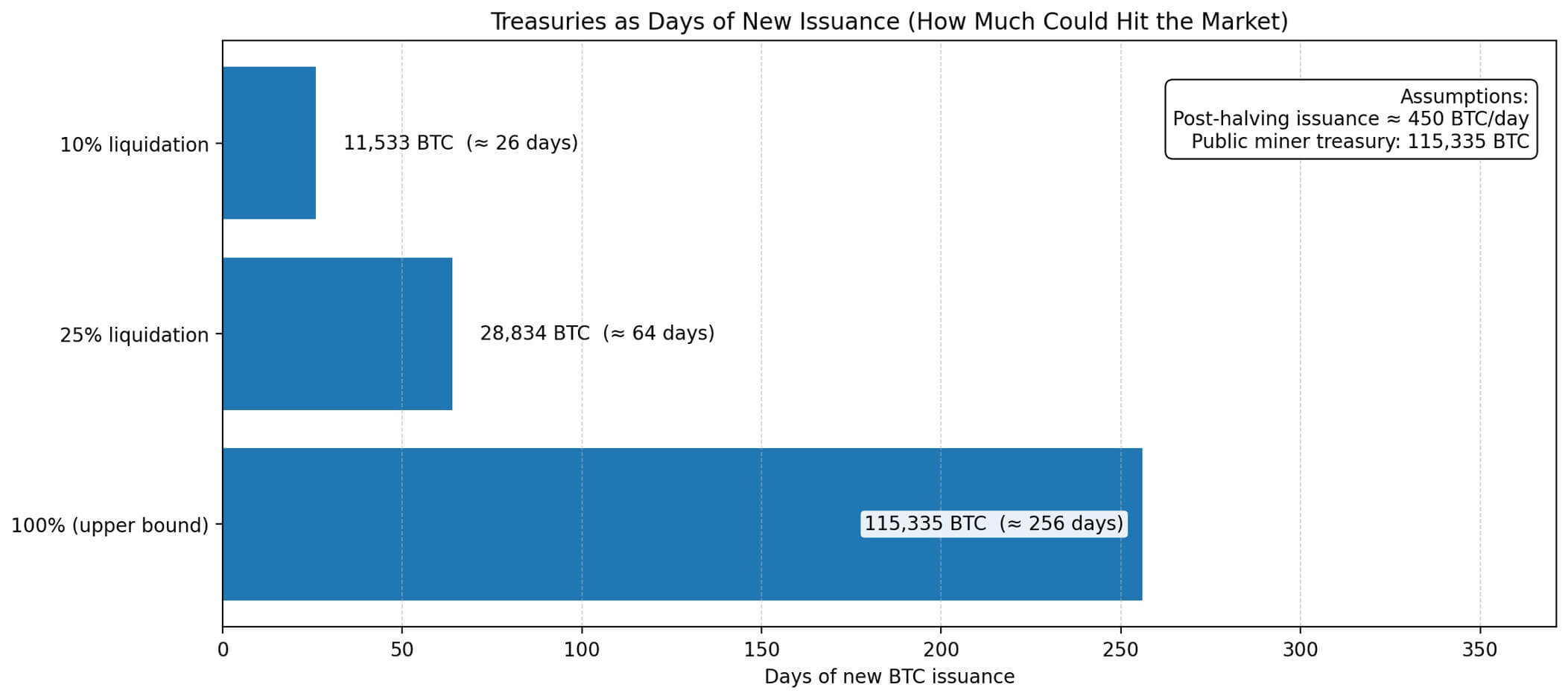

Around 450 $BTC The number of new tickets issued per day is 115,335 $BTC The amount held by public miners is equivalent to approximately 256 days of new supply.

Approximately 11,533 people will be released if 10% is cleared. $BTCequivalent to a 26-day minor issue. A 25% drawdown would be 28,834. $BTCor 64 days’ supply.

Visible inventory pools are important because they appear on audited balance sheets and are subject to quarterly disclosure requirements.

Unlike decentralized mining operations, public miners report their holdings and sales on SEC filings, making the Treasury Department the most transparent marginal source.

Concentration in the Ministry of Finance amplifies that power relationship. Marathon Digital holds 52,850 $BTCRiot Platform 18,005 $BTCClean Spark 13,513 $BTCHut 8 Mining 10,278 $BTC.

The fact that these four companies control the majority of disclosed reserves means that selling pressure will depend on how these companies finance their operations if hash prices remain depressed.

Bitdeer’s trajectory represents an extreme case. The company announced $300 million in convertibles for data center expansion, AI cloud infrastructure, and mining hardware while zeroing out its Bitcoin assets.

This pivot reconfigures Bitcoin holdings as fuel for capital investment, and other miners may follow suit if hash prices remain near current levels.

Futures markets are pricing in sustained stress

Luxor’s HashPrice futures market provides quasi-forecasts derived from market participants that hedge future profitability.

As of February 16, Forward Curve estimates the average hash rate over the next six months to be $28.73 per petahash per day. This pricing suggests that the market does not expect a quick return to profitability.

CoinShares suggested that if aggressive capacity expansion continues, the global hash rate could reach 1.5 zettahashes per second by mid-2026. If the hashrate increases without a proportional increase in the price of Bitcoin, the hash price will be further compressed.

The difficulty adjustment mechanism introduces timing risks. As the difficulty increases, the lag hashrate increases rapidly. This means that miners experience a temporary increase in profitability as the hashrate decreases, but after a few weeks, that gain disappears as the difficulty adjusts upward.

In our February 22 analysis, we framed the recent difficulty fluctuations as an environment of “higher difficulty, lower hash prices, and lower fees” that arrived just when miners needed relief. The mismatch between when earnings improve and when difficulties readjust creates cash flow instability and prompts operators to preemptively sell bonds.

Selective liquidation and complete withdrawal

Riot’s December 2025 sale offers one playbook.

The company sold 1,818 units. $BTC Shareholding amount decreased to $18,005 at $161.6 million $BTC while retaining the bulk of the Treasury. This approach demonstrates confidence that Bitcoin’s long-term trajectory justifies holding most reserves, even if short-term liquidity needs require partial monetization.

Riot’s cost structure, mining costs approximately $46,000 per mine $BTC Excluding depreciation, this suggests that the company could generate positive cash flow if Bitcoin rises above that threshold.

Bitdeer represents the opposite end of the spectrum. The company liquidated all its Bitcoin assets and turned the reserves into capital for AI and data center expansion. This move reframes mining as one revenue stream within a diversified infrastructure business.

Bitdeer’s $300 million convertible note funding shows the company is betting it can generate higher returns by putting money into AI cloud services than by holding Bitcoin.

Similar financial losses could occur if other miners conclude that AI infrastructure or power monetization offers higher risk-adjusted returns.

of $BTC Runway calculation

The real question is not whether miners will sell, but which miners will have to sell and how much.

Simplified liquidity analysis allows miners to$BTC This is the number of months that cash, undrawn lines of credit, and convertible debt issuance can be used to cover operating costs, interest, and capital commitments before Bitcoin needs to be liquidated.

Miners with a robust liquidity cushion can wait out a low hashrate environment, while operators with thin cash buffers face Treasury monetization pressure.

Offsets complicate the image. Hosting revenue from third-party miners, HPC contracts, power reduction payments, and equipment sales can generate cash flow independent of Bitcoin mining.

Hedging strategies using futures or options allow you to fix futures prices. Miners with diverse revenue streams face different funding pressures than pure Bitcoin miners who rely solely on block rewards and treasury valuations.

Selling pressure will not be applied uniformly and will be concentrated among operators with the shortest runway and fewest alternative sources of financing.

Markets are already showing stress

Glassnode’s Puell Multiple, a metric that compares daily miner revenue to a 365-day moving average, was 0.673 as of February 23rd.

A reading below 1.0 indicates that a miner’s revenue is below the one-year average, a situation that has historically preceded industry consolidation or forced asset sales.

VanEck’s analysis that the S19 XP threshold is uneconomical above about $0.07 per kilowatt-hour is important because electricity prices are not uniform across the industry.

Miners operating in areas that provide cheap hydropower or stranded gas can enjoy benefits that persist even when hash prices fall. Operators in high-cost regions face a choice between relocating, upgrading to more efficient hardware, or shutting down.

Government bonds become a funding variable

The shift from the HODL narrative to a working capital tool reshapes how the market should interpret miners’ balance sheets.

Public miners built their vaults at a time when hashrate supported profitable operations, and the price of Bitcoin rose faster than returns from alternative investments. That environment is reversed.

The hash price forward curve shows persistent weakness, with little contribution from transaction fees and equipment obsolescence accelerating as difficulty increases.

Visible inventory pool is 115,335 pieces $BTC The total across public miners equates to 256 days of new supply at current issuance rates, making even a small percentage of liquidations meaningful in daily market conditions.

Riot and Bitdeer demonstrated a variety of responses: selective treasury sales to preserve optionality and complete liquidations to diversify capital.

The difference lies in access to capital, diversification of returns, and management’s view of Bitcoin’s risk-adjusted returns. As long as forward hash price expectations remain around $28.73 per day petahash and older fleets become uneconomical above $0.07 per kilowatt-hour, miners’ treasury will act as a funding variable rather than a HODL signal.

The market’s job is to track which miners sell how much, and whether those sales represent tactical liquidity management or systematic risk aversion.