The Bitcoin mining industry is undergoing the most fundamental transformation in its history, and the clearest sign isn’t an adjustment to hashrate or difficulty. It’s a balance sheet.

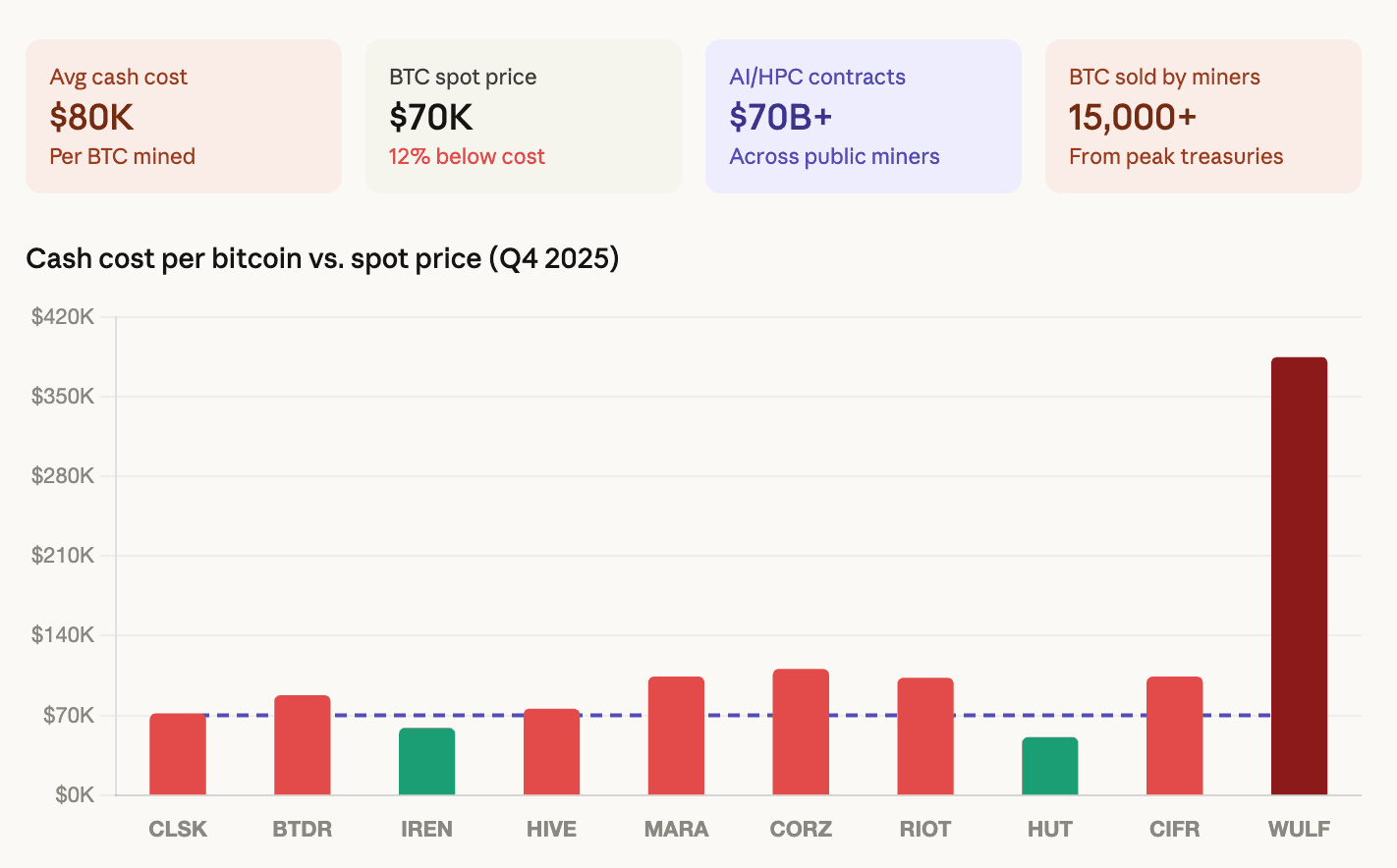

CoinShares’ Q1 2026 Mining Report released this week revealed that the weighted average cash cost to produce one Bitcoin among publicly traded miners rose to approximately $79,995 in Q4 2025.

Bitcoin is trading in the $68,000 to $70,000 range, and a CoinDesk report last week estimated losses of $19,000 per Bitcoin. $BTC mined.

These numbers are not sustainable and the industry knows it. The response has been a massive pivot to artificial intelligence infrastructure that is reshaping what these companies actually look like.

According to a report from CoinShares, more than $70 billion in AI and high-performance computing contracts have now been announced across the public mining sector. CoreWeave’s expansion deal with Core Scientific alone is worth $10.2 billion over 12 years. TeraWulf’s HPC contract revenue is $12.8 billion. Hut 8 signs a $7 billion, 15-year lease for AI infrastructure at its River Bend campus. Cipher Digital has a multi-billion dollar deal with Google-backed Fluidstack.

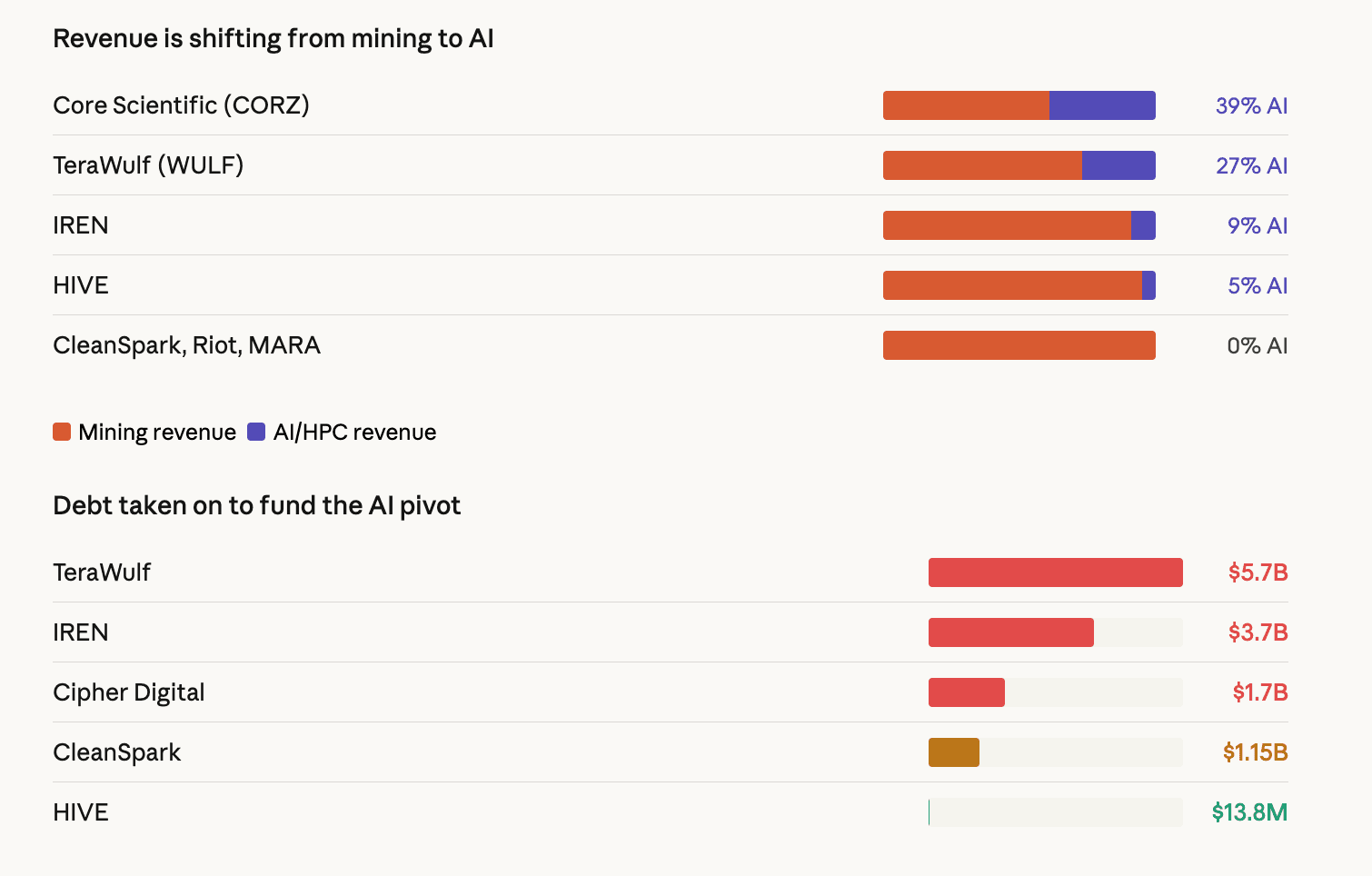

Publicly traded miners could earn up to 70% of their revenue from AI by the end of 2026, up from around 30% today. Core Scientific’s AI colocation revenue already accounts for 39% of its total. TeraWulf is 27%. IREN is 9% and rapidly expanding with up to 200 MW of liquid-cooled GPU capacity under construction.

This means that these mining companies are becoming data center operators who still mine Bitcoin on the side.

Economics explains why. According to CoinShares, the cost difference between roughly $700,000 to $1 million per megawatt for Bitcoin mining infrastructure and $8 million to $15 million per megawatt for AI infrastructure is significant, but AI structurally offers higher and more stable returns.

Hash prices, a metric that determines miner revenue per unit of computing power, hit a post-halving all-time low of about $28 to $30 per petahash per day in early March.

At this level, miners running mid-generation hardware need access to less than $0.05 per kilowatt-hour of electricity to maintain cash profits. AI infrastructure contracts, on the other hand, promise returns of 85% or more with multi-year revenue visibility.

Financial structure

The report explains that the transition is being funded in two ways, both of which are reflected in the data.

First, debt. The sector’s total leverage has fundamentally changed. IREN currently holds $3.7 billion worth of convertible notes across five series. TeraWulf’s total debt is $5.7 billion, split between its computing subsidiary’s convertible debt and senior secured debt.

Cipher Digital issued $1.7 billion in senior secured notes in November, and its quarterly interest expense soared from $3.2 million in the first nine months to $33.4 million in the fourth quarter alone. These are not mine-scale debts. These are infrastructure-scale bets that AI revenues will materialize quickly enough to meet obligations.

The second is the sale of Bitcoin. Listed miners collectively cut profits $BTC Ministry of Finance with over 15,000 people $BTC From peak level. Core Scientific sells approximately 1,900 units $BTC It was valued at $175 million in January and plans to liquidate substantially all of its remaining holdings in the first quarter of 2026. Bitdeer cut its finances to zero in February. Riot platform sales 1,818 $BTC worth $162 million in December.

Even Marathon is the largest public holder with 53,822 people $BTCquietly expanded its policy to authorize the sale of its entire balance sheet reserves in a March 10-K filing, partially driven by pressure on its $350 million Bitcoin-backed credit facility, which saw its loan-to-value ratio rise to 87% as prices fell toward $68,000.

The miners who sell Bitcoin to fund AI construction are the same companies whose mining operations ensure the security of the Bitcoin network. That creates tension at the heart of the transition. If mining is unprofitable and AI is profitable, a rational economic decision is to reallocate capital away from mining. But when enough miners do it, the network’s security budget shrinks.

Hashrate data already reflects this. The network peaked at around 1,160 exahashes per second in early October 2025, but has since experienced three consecutive negative difficulty adjustments, dropping to around 920 EH/s. This is the first time this has happened since July 2022.

Valuation markets are already pricing in a tipping point. Miners with secure HPC contracts are currently trading at 12.3x next 12-month sales. Pure miners trade at 5.9x. The market is paying more than twice as much for exposure to AI, which strengthens the incentive to pivot further.

Meanwhile, the geographical situation is changing along with the economy. The US, China and Russia currently control about 68% of the world’s hashrate. The US gained about 2 percentage points in market share in the fourth quarter alone.

But emerging markets are also making inroads. Paraguay and Ethiopia have joined the world’s top 10 mining countries, propelled by HIVE’s 300 MW operation in Paraguay and Bitdia’s 40 MW facility in Ethiopia.

Hashrate prediction and estimation

CoinShares expects the network hash rate to reach 1.8 zetahashes by the end of 2026 and 2 zetahashes by the end of March 2027, one month later than previously predicted.

However, that prediction depends on whether Bitcoin recovers to $100,000 by the end of the year. If the price stays below $80,000, CoinShares expects the hash price to continue to fall and the hash rate to decline further as more miners exit.

A sustained move below $70,000 could trigger a larger capitulation and, paradoxically, lower difficulty could benefit survivors.

Next-generation hardware offers a potential lifeline. Bitmain’s S23 series and Bitdeer’s proprietary SEALMINER A3 both operate at less than 10 joules per terahash and are expected to operate at scale until early 2026. These machines will roughly halve the energy cost per Bitcoin compared to the current mid-generation fleet. But deploying them requires capital, and many miners are investing in AI instead.

The Bitcoin mining industry entered this cycle as a group of companies securing networks and accumulating Bitcoin. They are withdrawing from the company as a group of companies that builds AI data centers and sells Bitcoin as funding.

Whether this is a temporary response to unfavorable economic conditions or a permanent structural change depends on one variable: the price of Bitcoin. If it returns to $100,000, mining margins will recover and the AI pivot will slow down. If it stays below $70,000, the transition will accelerate and the mining sector that has existed for the past decade will continue to disappear into something else entirely.