Bitcoin miners are starting to show the tension often seen near market washouts, but a key part of a normal reset is still missing. The largest operators are still selling enough BTC to maintain fresh supply to the market.

Bitcoin miners are moving towards the classic washout point, but the market is still in a sell-off phase

Bitcoin miners are closer to exhaustion than they were a few weeks ago, and the familiar bear market milestones are back on the table.

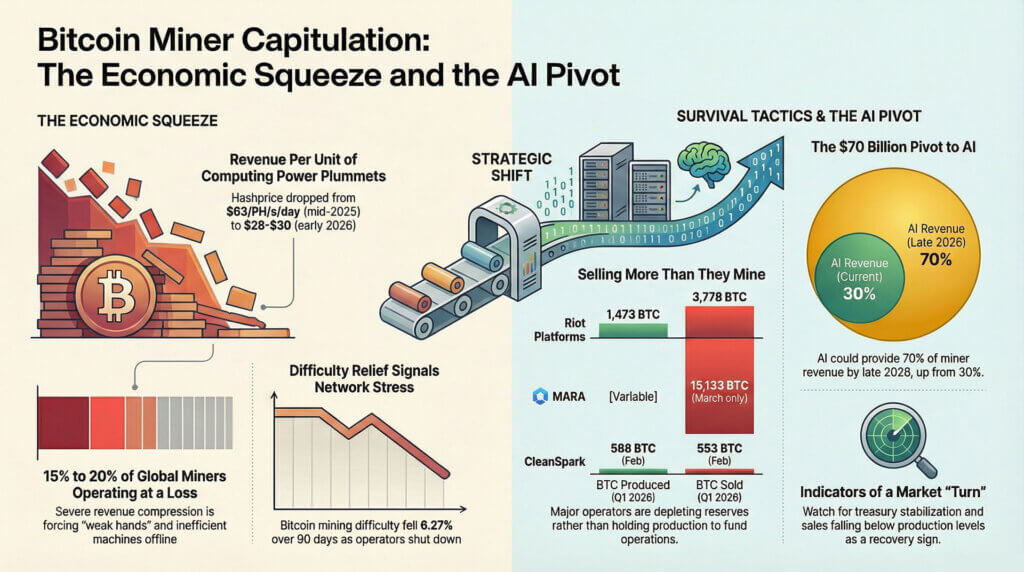

Pressures within the mining business are extremely high. In its Q1 2026 mining report, CoinShares shows that hash prices have fallen from around $63 per PH/sec/day in July 2025 to around $28-$30 per PH/sec/day in early March 2026, significantly compressing miner revenues and forcing a large portion of the world’s fleet into unprofitability.

CoinShares estimates that around 15% to 20% of the world’s miners are operating in the red at their revenue levels, making the current cycle a clear economic trigger rather than a vague sentiment narrative.

Why this is important: Miners are one of the most important stable sources of Bitcoin. If they are forced to sell more of what they mine or draw down reserves, they could continue to weigh on prices even if conditions start to improve.

That pressure is starting to show up in the network landscape. According to CoinWarz’s Bitcoin difficulty chart, difficulty has decreased by 4.19% in the past 30 days and 6.27% in the past 90 days, with a further correction expected on April 18, 2026.

A decrease in difficulty usually indicates that weaker operators are forced out, machines are taken offline, and the strongest miners can get more room. This kind of reset often appears near the end of the minor surrender phase, which is why the current setup is getting so much attention.

Surrender begins with stress. A more significant change occurs when miners stop selling large amounts of government bonds to fund operations, debt repayments, and expansion. This second step is more significant for Bitcoin because it changes the flow of coins that enter the market every day.

Financially stable miners can keep more of the BTC they produce. Pressured miners send their coins to the spot supply.

The latest public minor update indicates that this second step has not been widely adopted. Riot Platforms produced 1,473 BTC in the first quarter of 2026 and sold 3,778 BTC during the same period, ending the quarter with 15,680 BTC on its balance sheet.

This number reflects the tension within the market. Stress on the network has eased enough to fuel bottom-call chatter, but one of the industry’s largest operators still sold far more Bitcoin than it mined in the quarter.

MARA sold 15,133 BTC from March 4th to March 25th. This move is related to bond buybacks totaling approximately $1 billion. CleanSpark produced 568 BTC in February and sold 553.02 BTC, almost all of its monthly production.

This moment demands precise words. Miners are moving toward a historic bear market milestone because economic conditions are tough enough to exclude the weak, and difficulties are starting to ease.

However, the accumulation phase has not clearly resumed. A real change in miner behavior will manifest as financial stabilization, a decline in sales relative to production, and a pattern in which large operators begin to retain more of the Bitcoins they mine.

This series of signals will visibly tighten the supply side of the market. Current data shows the sector is closer to the end of the forced selloff than it was earlier this year, and there is plenty of evidence that the forced selloff remains active.

Balance sheet stress drives miner action to maintain a stable supply of Bitcoin in circulation.

The sharpest way to understand miner sales is to strip away the jargon and follow the cash demands. Mining companies face electricity costs, salaries, hosting costs, equipment financing, and fiat debt maturities.

Although they earn Bitcoin, many of their obligations are paid in dollars. When the return per unit of computing power collapses, Treasury sales become the financing mechanism.

This dynamic has turned recent miner activity into a pressure point on Bitcoin’s market structure.

Riot’s Q1 numbers made that pressure visible in a way that on-chain abstractions can’t match. Selling 3,778 BTC while producing 1,473 BTC shows that the company was relying on existing reserves and not just current production.

MARA’s March sale made the same point from a different angle. The company used large BTC sales to help manage its debt, but it was a reminder that miners are part of the crypto business and are also operators of capital-intensive industries.

CleanSpark’s February update showed a real-world production version of the same, with nearly all of its monthly production sold. These disclosures pinpoint where the tensions are and frame the current market more clearly than general references to minor stresses.

The broader reserves picture also fits that interpretation. In February, igcurrencynews reported that while approximately 1.801 million BTC was stored in miner-related wallets, the dollar value of these reserves had fallen by more than 20% in about two months to approximately $133 billion.

This decline did not occur in isolation. The decline in Bitcoin prices from its peak in 2025, weak fee income, and still-intense competition within the network have all combined to deplete the cushion that miners typically rely on in tougher times.

For Bitcoin itself, this brings into focus one of the market’s most important supply channels. Miners produce new coins every day.

In healthier stages, operators can afford to retain some of their output, so some of that output remains unmarketable. During the stress phase, newly minted coins and old bonds are sold to meet real obligations.

This trend could weigh on prices even as sentiment improves and other bullish stories gain momentum.

The current price background makes the setup particularly sensitive. According to Bitcoin price data from igcurrencynews, BTC is trading at $69,900, up 4.38% in 24 hours, 3.63% in 7 days, and 2.81% in 30 days, but is still 44.61% below its all-time high of $126,198 on October 6, 2025.

That puts Bitcoin in an interesting position. There is enough upside movement in the market to revive bottom calls and enough distance from the peak to keep miners financially burdened.

Bounces within this type of structure often reveal who was selling because they wanted to sell and who had to sell.

Difficulty easing, ETF demand, and AI pivots will determine whether miner accumulation returns or the cycle changes shape.

Those differences will shape the path forward. As Treasury depletion slows and public miners start reporting less revenue than they produce, the market will get evidence that balance sheet stress is finally fading.

If major carriers continue to monetize their reserves during periods of strong prices, the easing phase could be prolonged and weigh on price increases. A few upcoming production updates from listed miners would be of real significance as they would be direct proof of whether corporate behavior is changing or if there is still room for execution in the sales cycle.

Three forces are currently at the heart of what’s next: easing hardship, external demand for Bitcoin, and changing business models for large-scale miners. Each influences whether a sector can move from survival mode to accumulation mode.

The first force is difficult. Lower difficulty gives surviving miners a larger share of network rewards, easing immediate revenue pressure.

Therefore, the expected April 18 correction on CoinWarz has become very significant. Deeper cuts could give weaker managers less room to recover than stronger, better-capitalized mining companies and further concentrate production in the hands of companies that are better able to choose when to sell.

If this happens, the market will likely be close to resuming full-scale accumulation. Shallow adjustments and quick rebounds in competition will likely keep pressure on the margins.

The second force is external demand, specifically demand from the US Spot Bitcoin ETF. The Farside ETF’s flow data shows positive net inflows of $69.4 million on March 30 and $117.5 million on March 31, followed by $173.7 million in outflows on April 1 and a smaller inflow of $9 million on April 2.

This pattern captures the current market mood. Demand exists, but it has not yet settled into a strong, uninterrupted absorption phase.

ETF buyers can offset miner selling if flows are consistently positive. When the flow is disrupted, there is less protection from fresh supply and they exit the market.

In the long run, the third force may prove to be the most important. CoinShares says publicly traded miners could derive 70% of their revenue from AI by the end of 2026, up from around 30% today, as power access and data center infrastructure become more valuable to high-performance computing customers.

With more than $70 billion of GPU colocation and cloud-related deals announced through 2025 and early 2026, mining companies have entered the infrastructure business tied to larger capital cycles. That changes the incentives.

Miners with attractive AI hosting opportunities may choose to reduce debt, secure expansion funding, or reallocate power from their Bitcoin stockpiles.

This is where the old strategies start to blur. The historic Miner Surrender milestone still provides useful context, as business remains cyclical and forced sales still leave their mark on Treasury actions, hardships and reserve withdrawals.

But the next stage may not look like a simple return to old patterns. As the economics of mining improve, some operators may stop actively selling BTC.

Other companies may continue to sell as their strategic focus shifts to AI-related revenue. Traditional accumulation signals may arrive later than many expect and may appear in a narrower segment of the industry rather than the entire minor cohort.

This leaves Bitcoin with a clear live marker. Stay tuned to see if the big miners will have less revenue than mining in future updates.

Watch to see if the difficulty continues to drop enough to restore healthy margins. Watch to see if ETF flows consolidate into a more stable absorption channel.

It will be interesting to see if AI infrastructure becomes a preferred use of minor capital for the largest utilities. These signals will reveal whether the sector is finally coming out of its capitulation phase and rebuilding its treasury, or whether the current cycle is shifting to a different form, one in which miners remain important to the supply side of Bitcoin, but the business incentives extend far beyond the mining itself.

At this point, the evidence supports a clear middle ground. Bitcoin miners are moving towards the classic washout milestone, as economic conditions become so tough that they are forced to exit, triggering an easing of hardship.

The accumulation reboot that usually gives real power to that milestone has yet to emerge for the largest companies in the sector. Until Treasury sales visibly slow down, those producing new Bitcoin will still be part of the pressure on the market, even as the conditions for a deeper reset begin to form.

(Tag translation) Bitcoin