On March 31, 2026, Wall Street recorded its best trading day in nearly a year. The Dow Jones Industrial Average rose more than 1,100 points, the S&P 500 rose 2.9%, its best single-day performance since last May, and the Nasdaq rose 3.8%.

The mood, as one market general cheerfully dubbed it “Hormuz hope,” was a rally based on the possibility that the war between the United States and Iran and its strain on global oil supplies might finally be coming to an end.

President Trump has expressed openness to suspending military operations, and Iran’s president said Iran has the “necessary will to end the war” if security conditions are met.

But beneath these headlines, traders in the more complex products of financial markets (options, futures, hedges) did not buy the news. While on the surface the market may have appeared to be finally stabilizing with upside potential, the underlying positioning remained uncertain.

To understand why, you need to understand two simple concepts: what “open interest” means and what it indicates when open interest shrinks. Open interest is the total amount of bets that remain active in derivatives markets, futures, and options contracts that have not yet been settled or closed. When open interest increases, more traders put money into the market and express confidence in where the market is heading. When it falls, they close their positions, cut their losses and exit.

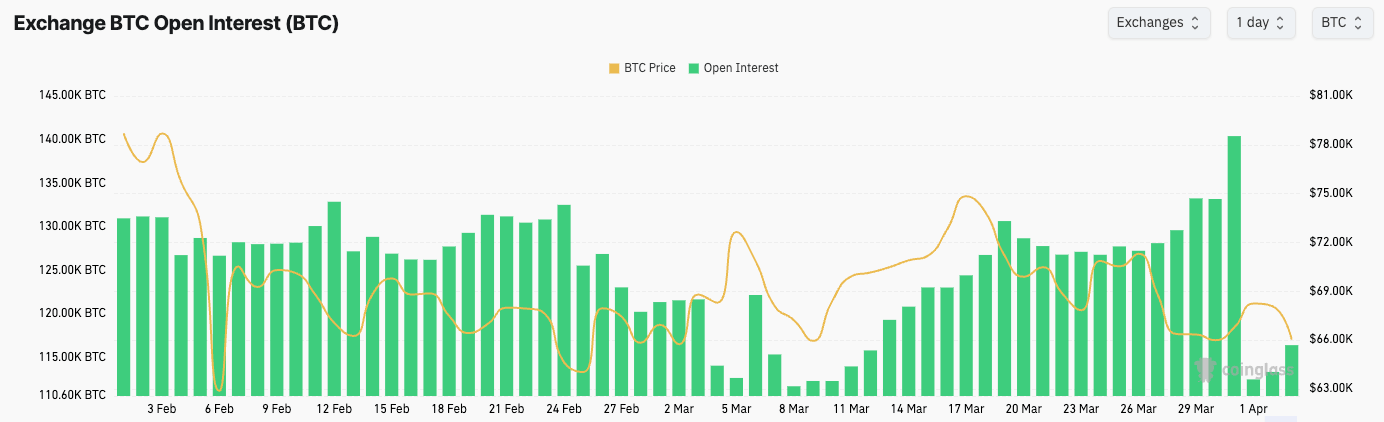

Bitcoin’s $46 billion derivatives problem

Bitcoin trades 24 hours a day on hundreds of exchanges around the world, essentially serving as a living barometer of global risk appetite, but that barometer is currently showing murky numbers.

Total open interest in Bitcoin derivatives reached approximately 703,940 Bitcoins with a notional value of approximately $46.85 billion, indicating that the market remains highly leveraged after the major stress. If hopes for peace are indeed returning, confident rerisk traders will appear to be buying aggressively. As such, the 4.41% one-day pullback in open interest seen on April 1st is more cautious than certain.

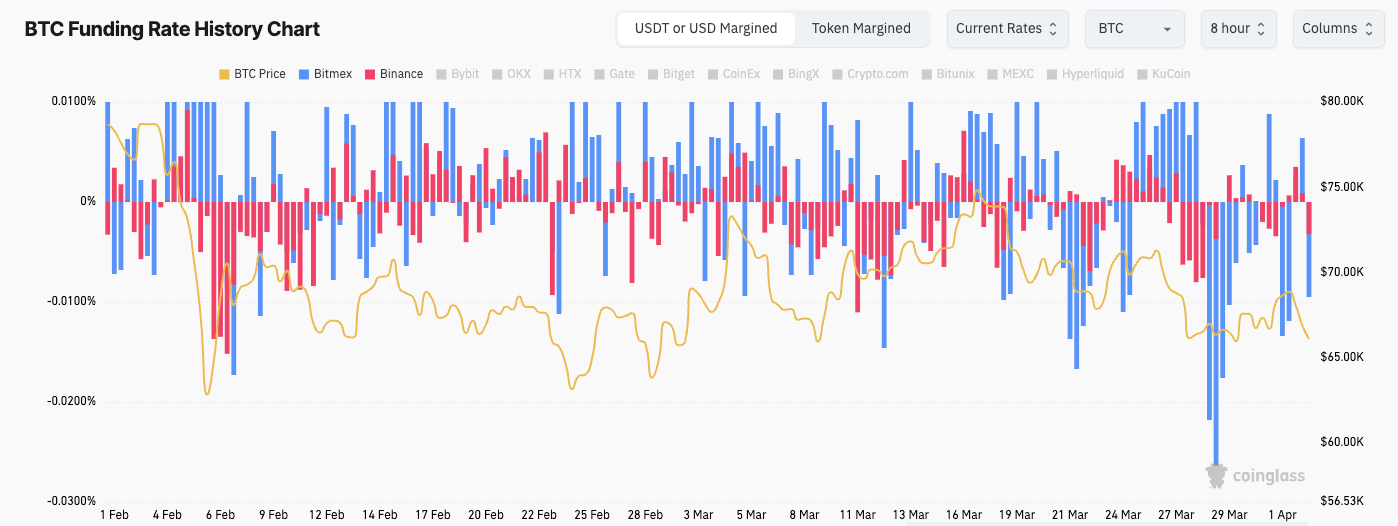

The funding rate, the fee that traders who hold bullish positions must pay to maintain them, has been only marginally positive, punctuated by repeated negative declines. As funding rates spike, bullish sentiment pushes open interest to unsustainable heights, indicating that the number of buyers significantly outnumbers sellers. Bitcoin funding has been slow over the past two weeks, moving from flat to barely positive, indicating a lack of appetite for new risks.

What makes it difficult to ignore this as noise is the significant increase in institutional presence in Bitcoin derivatives. Of the $46 billion in open interest, more than $7 billion is held on CME. CME is the same regulated exchange where pension funds and sophisticated asset managers do most of their hedging. The increasing open interest of institutional investors has established Bitcoin as a mainstream financial product. This means that this decline reflects decisions made in boardrooms and trading desks, far beyond retail market speculation.

The ratio of options to Bitcoin futures has also changed. Earlier this year, options, which act like insurance contracts and provide a cushion against sudden price changes, held a much larger share of the Bitcoin derivatives market, but that share has since fallen to about 65%, a sharp drop from last month’s highs of nearly 90%.

As options exposure shrinks and futures dominate, the market becomes more directional, less isolated, and more manageable until something quickly goes wrong. The data shows that special sensitivity is concentrated in the $66,000-$67,000 price range, and there appears to be a concentration of large positions in this zone, where a return to that range could quickly make things unstable.

Oil options tell the same story.

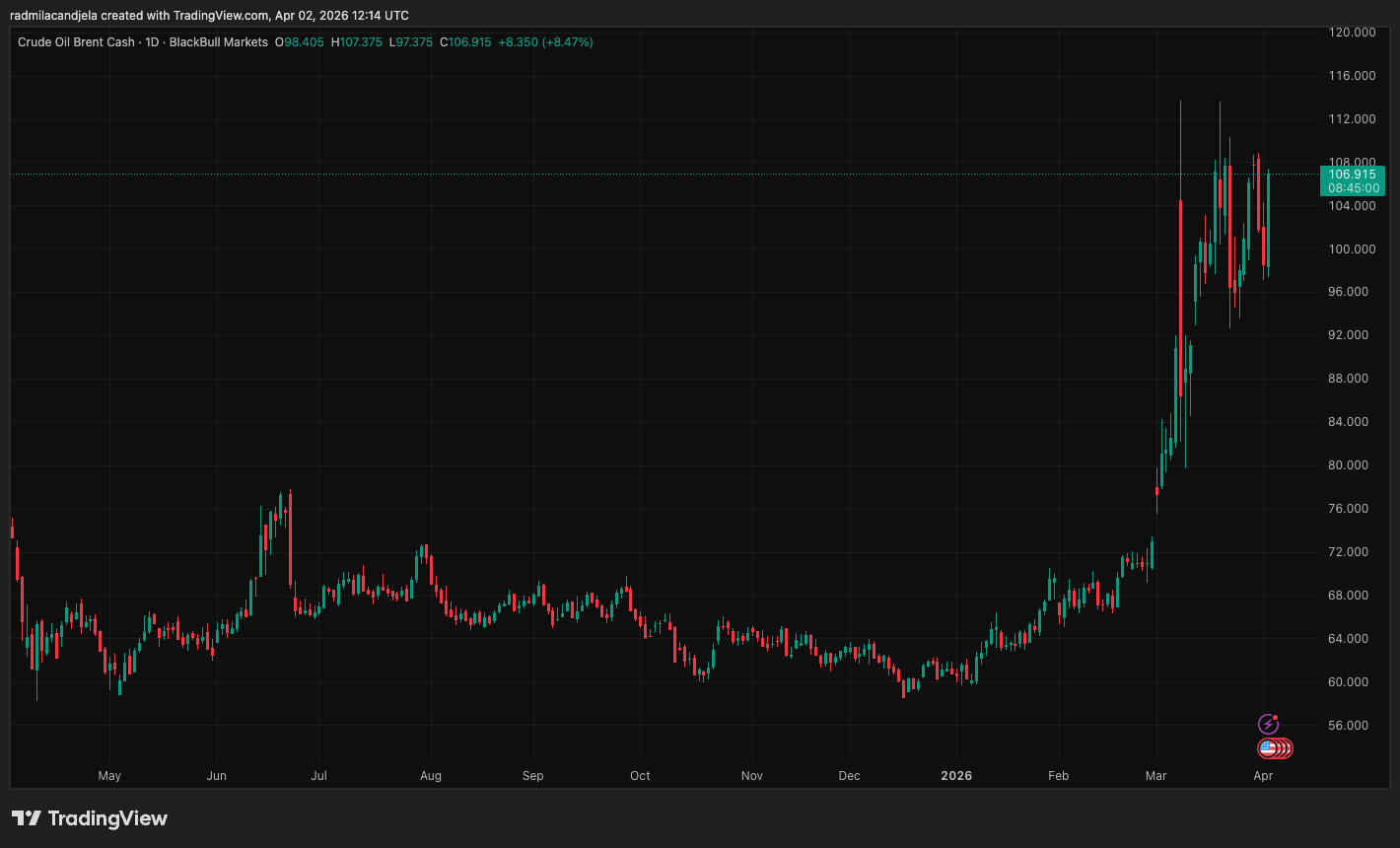

The Strait of Hormuz is a 34-mile chokepoint through which about 20% of the world’s daily oil consumption flows, but commercial traffic has been reduced to a trickle since the conflict began. Rystad Energy said it disrupted the flow of about 17.8 million barrels of oil and fuel per day, with a total of nearly 500 million barrels of liquids lost to date.

When Brent crude oil prices briefly fell below $100 a barrel on April 1, retreating from highs of more than $112 a few days earlier, markets took it as confirmation that the worst was over.

However, uncertainty in the options market remains fairly low. Holding of Brent call options, a bet that oil will hit $150 a barrel by the end of April, has increased tenfold in the last month, and open interest in these contracts now stands at nearly 29,000 lots (equivalent to 1,000 barrels of oil each). This is a clear sign that the market foresees the tail risks of this conflict.

The largest concentration of open interest remains in $100 call options, and such positioning reflects the market still hedging against further upside shocks rather than celebrating all liquidations.

deVere CEO Nigel Green explained the underlying concerns:

“The North Sea Brent price of $115 is being treated as a spike. The data tells a different story. Prices are up nearly 60% in a single month, options markets are actively pricing in a $150 oil scenario, and up to 20% of global supply is disrupted through the Strait of Hormuz. These are not conditions associated with short-lived shocks.”

This view finds unpleasant resonance in the diplomatic record itself. President Trump said Iran had called for a ceasefire. Iran’s Foreign Ministry called the claims “false and baseless.” As the two governments offered conflicting explanations for the same negotiations with the same sticking points, the market rallied towards the more optimistic side, but hedges continued to price in both.

The result is a simple but significant gap. Stock markets are welcoming an unconfirmed ceasefire framework, Bitcoin open interest is shrinking at a time when it should be rebuilding, and oil options are still pricing in a meaningful possibility of an energy rally.

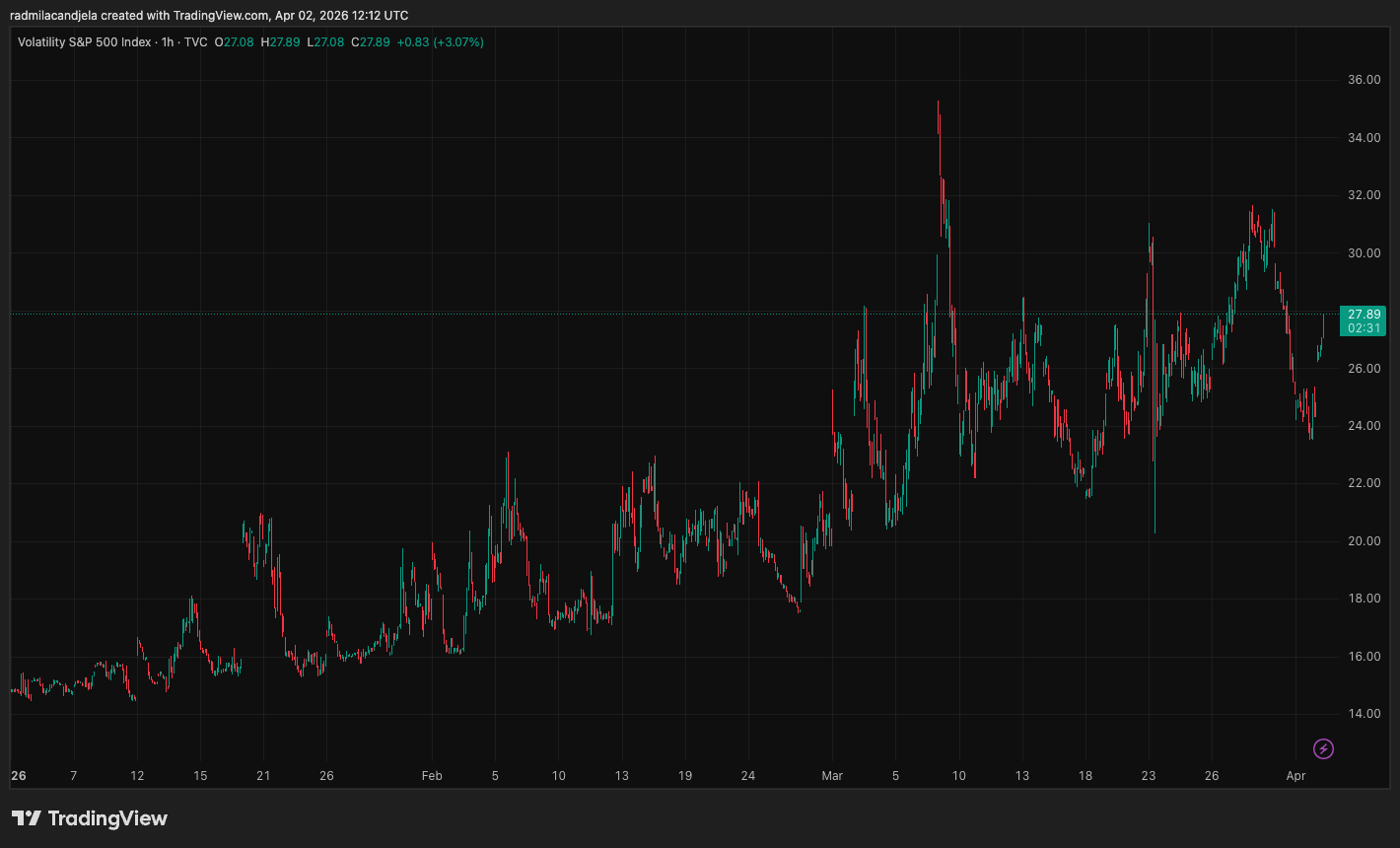

Wall Street’s own fear index, the VIX index, fell, but remained at a level of 24.54, indicating heightened anxiety. Markets are generally good at pricing in the future they want, but the underlying derivatives tend to price in the future they fear, and right now these two futures look quite different.

The rally has quieted the headlines without any sort of positioning, and once the ceasefire is lifted, Bitcoin and oil are likely to be the first to emerge.

(Tag translation) Bitcoin