Bitcoin mining remains the backbone of the crypto economy. In the Asia-Pacific region (APAC) region, abundant hydroelectric power, gas reserves, and excess electricity create opportunities and friction.

The region faces high power costs and fragmented rules while offering the possibility of a “green hash.” For global investors, APAC Bitcoin Miners are currently at the heart of the debate over energy use, transparency and capital access.

Overview of APAC Bitcoin Mining

Latest updates – In July 2025, Bitdeer expanded Bhutan’s hydroelectric mining capacity to over 1,200MW, positioning the country as a renewable mining hub. Marathon Digital and Zero Two have begun operation of 200mW immersion-cooled sites in Abu Dhabi, demonstrating how advanced cooling and flare gas integration is maintained in extreme climates. Meanwhile, Australia’s IRIS energy reports 50EH/s, indicating how APAC miners scale with their Western peers.

Background context – Cambridge Bitcoin Mining Map shows that after China’s 2021 crackdown, Bitcoin mining will shift across the Asia-Pacific economy, with underground activities continuing in China. Energy data issued by Asia-Pacific Economic Cooperation, pWith an increase in renewable renewable penetration, Bitcoin mining creates conditions that match the decarbonisation goals, if supported by policy.

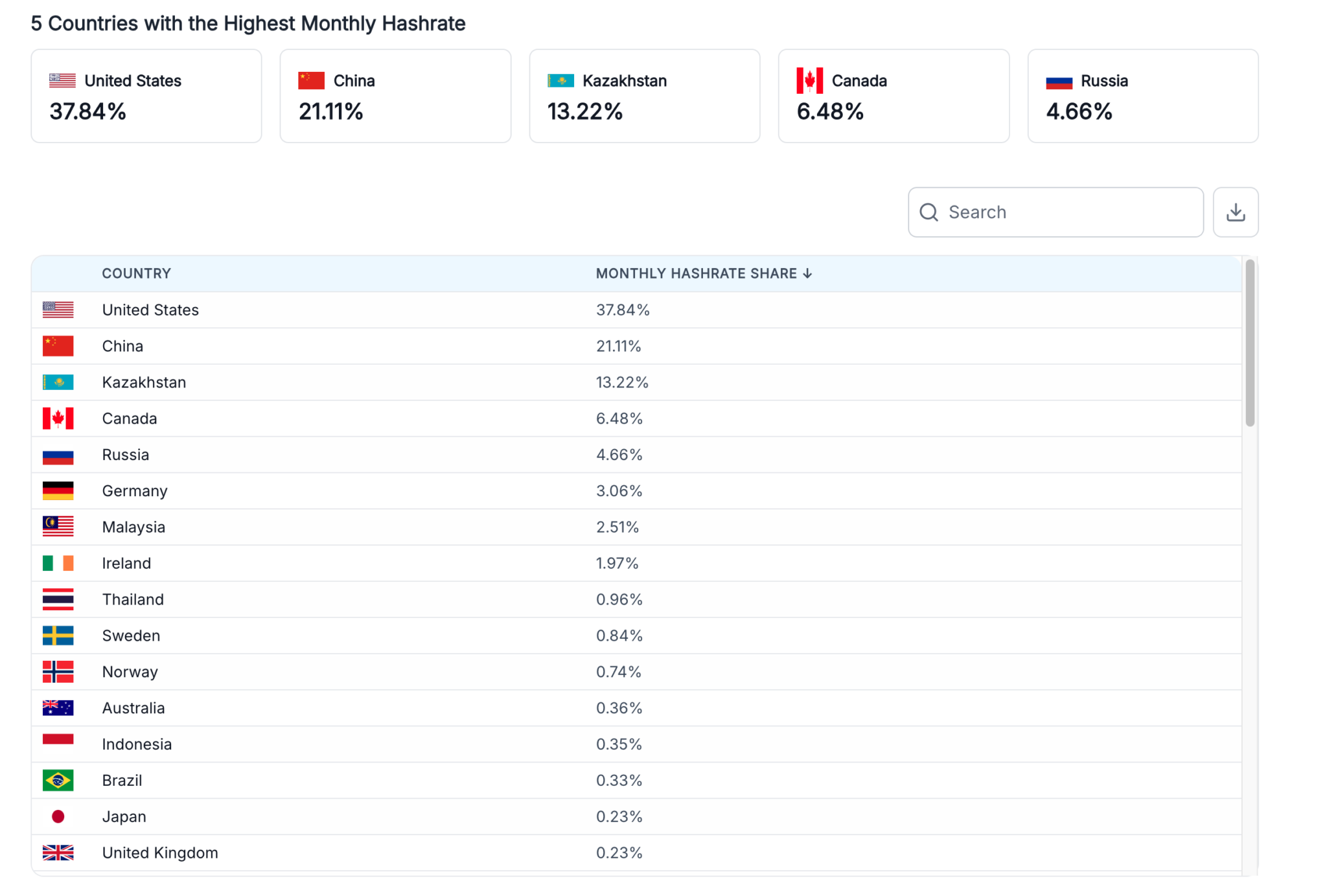

Bitcoin mining by the government 2025. Source: World Population Review

Deep analysis – China remains opaque. Despite the ban, seasonal hydropower in Sichuan and underground clusters continues. Cambridge Digital Mining Industry Report 2025 warns of underreporting activities in China, complicating global hash power and focused risk assessments.

In fact, despite the 2021 ban on crypto mining, the country still accounts for more than 21% of the world’s hashrate. This sustainability is driven by local underground hydroelectric power projects such as Sichuan, dispersed small farms avoiding detection, and local utilities that quietly sell surplus electricity. Beijing maintains a paper ban, but in reality it appears to withstand Shadow Bitcoin mining.

High electricity prices in Japan limit domestic farms. However, companies such as SBI Crypto and GMO operate overseas on renewable sites. Domestic, SoftBank’s 300MW data center in Hokkaido shows how AI infrastructure overlaps with mining-scale energy loads. PTS has signed a contract to supply telecom grade hashrates over three years in the Japanese corporate segment, demonstrating stable demand for stable capacity.

South Korea is investigating the integration of its electricity system. A May 2025 ARXIV survey suggests that monetizing surplus electricity from Bitcoin mining could help Kepco reduce debt while reducing grid losses. This model reconstructs mining as a grid balancing tool rather than a burden.

Asian Green Hash: Hydroelectric, Flare Gas, Renewable Expansion

Bhutan’s hydropower expansion with BitDeer shows how Asia can brand Bitcoin mining to attract environmentally sustainable and ESG-oriented capital. Abu Dhabi’s immersion cooling sites demonstrate how flare gas and advanced infrastructure redefine the efficiency of hot climates. Australia’s IRIS Energy combines renewable mining with AI computing to position itself across the digital and energy markets, demonstrating a hybrid model. These cases demonstrate that Asia-Pacific Bitcoin mining is becoming more flexible, diverse and sustainability-driven growth.

Behind scene – APAC Miners balances local politics with global scrutiny. Japan and South Korea focus on energy integration rather than pure scale. Bhutan sells sustainability, but China’s hidden activities raise concerns about transparency. The United Arab Emirates and Australia will leverage energy mix to reduce institutional capital and marginal costs.

Wideer impact – Institutional investors demand high disclosure standards. While US listed miners gain trust in SEC filing and market liquidity, APAC companies must bridge fragmented frameworks. However, if Asian miners provide ESG-supported transparency, capital flows could diversify more evenly between the East and West.

I’m looking forward to it – By 2026, more APAC miners could approach it on par with their Western peers if they combine efficiency with reliable disclosure. Competitiveness relies on rapid upgrades to next-generation ASICS, integration with renewable grids, and establishing regional reporting standards that reduce perceived risks for global investors.

Policy Costs and Local Risks

Data Breakdown–The CCAF 2025 report highlights increased hardware efficiency and geographical restructuring of mining capabilities. Local iThe Ntergovernmental Forum energy outlook shows how regional energy trajectories can resharp the cost base and carbon profile of Bitcoin mining.

Possible risks –

- Japan: High power costs cap local capacity.

- China: Underground activities undermine transparency and risk assessment.

- Korea: Grid integration relies on political and regulatory support.

- Bhutan and the United Arab Emirates: Climate change can affect hydrology and flare gas uptime.

- Supply Chain: ASIC production remains exposed to tariffs and geopolitics.

Expert opinion –

“The most important risk for Asian miners remains unregulated and unpredictable. Without long-term clarity, capital costs will rise and global investors will be hesitant.”

– Alternative Finance Centre in Cambridge, Digital Mining Report 2025

“The Abu Dhabi facility demonstrates how the integration of immersion cooling and flare gas redefines mining economics in a challenging climate.”

– Marathon Digital Holdings, Press Release

“By monetizing excess electricity through mining, utilities can improve financial health while stabilizing the power network.”

– ARXIV research, Korean Bitcoin Mining and Grid Efficiency (May 2025)

Despite the first appearance of Chinese underground activities in beincrypto, post-APAC Bitcoin mining will be green.