Ethereum Institutional announced its formation on July 1, consolidating a year of foundation go-to-market efforts into a group pitching Ethereum to banks and asset managers for tokenization and stablecoins.

Ethlabs was built by five former senior researchers at the Ethereum Foundation (EF) and surfaced a few days ago with the aim of speeding up payments and ETH money litigation. Bitmine, Sharplink and Joe Lubin are funding both efforts.

The timing coincides with the foundation’s own organizational dismantling, with at least eight senior executives resigning in five months, with Xiaowei Wang stepping down as EF co-executive director on June 18, joining Tomasz Stanczak, who resigned earlier.

The Foundation’s own March 2026 mandate has already redefined its role as a self-sovereign, censorship-resistant, custodian of open source code, privacy, and security, without claiming to be the parent or ultimate authority of Ethereum.

This leaves room for outside groups to take over the commercial half of the job, intentionally or not.

Ethlabs absorbed the technical and asset value aspects, focusing on the infrastructure readiness, ETH as a financial product, and discussions about how financial institutions can comfortably hold and build on-chain.

Ethereum Institutional has absorbed the sales side through relationship building, forums, and pitch decks that convert interest into investment funds.

The Foundation wasn’t built to perform either function well, so both were moved outside of EF. A neutral standards body cannot double as an advocacy body or corporate sales team for ETH without diluting the credibility that served it as a standards body in the first place.

The Foundation will hold the legitimacy and long-term protocol value, Ethlabs will hold the ETH value capture and technical preparation, and the Ethereum Institutional will hold the distribution to enterprises.

| function | old center | emerging center | strategic meaning |

|---|---|---|---|

| Values, neutrality, and protocol legitimacy | Ethereum Foundation | Still Ethereum Foundation | EF maintains a trusted neutral layer for Ethereum. |

| Capturing ETH value and preparing infrastructure | Ethereum Foundation researchers | S-Lab | Technical and financial work will be transferred to a Treasury-supported research and development node. |

| Institutional sales and corporate recruitment | EF go-to-market efforts | ethereum institution | Corporate distribution will move to dedicated non-profit organizations established for banks, asset management companies and listed companies. |

| A story of wealth accumulation and open markets | Crypto Native Holders and ETF Flows | ETH treasury companies such as Bitmine and Sharplink | If ETH demand increases, companies funding new stacks will also directly benefit. |

Ethereum Institutional says its team already has more than 500 institutional relationships across Tier 1 banks, asset managers, sovereign institutions, custodians, and market infrastructure providers.

Its institutional Ethereum Forum attracts more than 150 senior executives and total assets under management of approximately $250 trillion. This scale is an argument for building an independent organization rather than performing the work as a side project within EF.

Delegating corporate distribution and ETH advocacy to an outside group resolves the enforcement disconnect, but also means that the company with the largest ETH balance sheet funds the loudest voice promoting Ethereum to Wall Street.

Convenience and independence are mutually exclusive, and Ethereum chose convenience.

Ethereum’s Wall Street Machine is being rebuilt by the ETH treasury needed to operate

Bitmine currently holds 5.7 million ETH, which is 4.7% of its total supply, including cash and securities, and has a balance sheet of $9.8 billion. Sharplink holds 886,725 ETH and added to its position on June 28th by purchasing 10,000 ETH at an average price of $1,611.

Together, the two companies hold approximately 6.59 million ETH, which is approximately 5.46% of the 120.7 million ETH supply listed by Bitmine itself. At current prices, its shares are worth nearly $10.6 billion, compared to Bitmine’s $6.55 billion market cap and Sharplink’s market cap of more than $1 billion.

A successful split would directly benefit both companies, as better infrastructure and cleaner institutional sales will increase demand for ETH, and both companies hold enough ETH to change their balance sheets by hundreds of millions of dollars with a moderate price movement.

Joe Rubin, who supports both nonprofits and co-founders of Ethereum itself, sits at the center of that coalition. This arrangement is a noteworthy structure because Bitmine and Sharplink have a direct financial impact on its success.

PeerDAS is already operational and will increase the data availability capacity of Layer 2 networks by approximately 10x. Meanwhile, Glamsterdam, planned for the second half of 2026, targets base layer scaling, parallel transaction processing, and larger block payloads.

A June 2026 academic paper measured the results so far and found that mainnet and layer 2 transaction throughput has doubled. The median mainnet price dropped from over $2 to less than $0.02, and the median layer 2 price fell more than 95% to about $0.0015.

Mainnet throughput will remain below 100 transactions per second until 2034, layer 2 networks will not overtake Solana’s throughput until March 2029, and median prices will be lower by October 2026.

The institutional case for Ethereum relies almost entirely on Layer 2 execution and standardization work, the technical position that Ethlabs exists to manage.

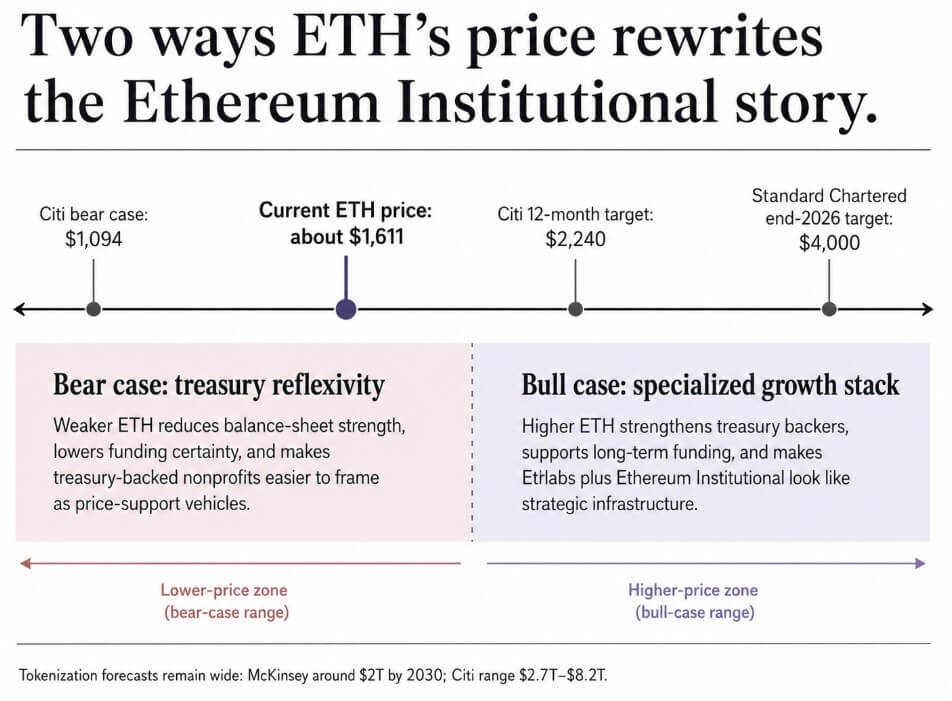

Two ways the price of ETH could rewrite this

The bullish case is based on the scale that already exists, as Ethereum has around $157 billion of stablecoin value on its network, which is more than half of the world’s stablecoin supply, and DeFi deposits are around $37.2 billion, more than 62% of the total blockchain-based DeFi value.

RWA.xyz ranks Ethereum as the top tokenized real-world asset network, with approximately $15.8 billion in distributed asset value and $31.52 billion across all tracked networks.

Citi projects that the broader tokenization market will grow from around $17 billion today to $5.5 trillion by 2030, with a range of $2.7 trillion to $8.2 trillion. If Ethlabs meets demand and maintains the infrastructure, and Ethereum Institutional converts relationships into deployed capital, the Treasury companies funding both will start to resemble early stewards.

Ethereum will become the default payment method for regulated digital assets, and balance sheets will benefit accordingly.

The bear case starts with price. Citing thin ETF demand and negative flows, Citi lowered its 12-month ETH target from $3,175 to $2,240, setting a bearish scenario at $1,094 versus ETH’s current price of around $1,611.

Standard Chartered strongly disagrees, sticking to its $4,000 target by the end of 2026, but the disagreement itself shows how volatile short-term litigation can be.

If ETH weakens and Treasury stock continues to trade at a discount to its underlying assets, Bitmine and Sharplink’s ability to continue underwriting the two nonprofits will shrink along with their balance sheets.

Ethlabs and Ethereum Institutional will likely continue to operate. However, funding certainty will be reduced and both groups will have a harder time deflecting claims that they exist to support the price of ETH rather than building true institutional infrastructure.

Regulatory tailwinds do not guarantee a bull market, they help it. The GENIUS Act of 2025 provided the first federal framework for stablecoins in the United States. Consortium in partnership with Visa, Mastercard, and Coinbase After that framework existed, we launched Open USD, a competing stablecoin.

Such regulatory moves will benefit all chains competing for institutional payments volume.

McKinsey’s more conservative tokenization forecast of around $2 trillion by 2030 versus Citi’s much larger scope is a reminder that real disagreements are baked into even the bullish case.

Ethereum solved its post-foundation problems by creating two new organizations. Both are funded by companies that stand to gain the most from ETH’s rise, and both hold jobs that a neutral administrator would never fill.

This deal could yield exactly what it promises: better infrastructure, access to cleaner institutions, and a chain that earns its place as the default payment layer for tokenized finance.

It could also mean that Ethereum’s expansion machine is now running on the same balance sheet as the one it should be expanding.

Both are true at the same time, and where the price of ETH is in a year’s time will determine which one will prevail.