Strategy, the Bitcoin financial and enterprise software company formerly known as MicroStrategy, has spent years turning the public markets into a funding engine for Bitcoin purchases. This model has helped make the company the world’s largest corporate holder of digital assets.

Currently, the securities used to drive that strategy are under stress.

The pressure is centered on STRC, Strategy Inc.’s floating-rate Series A perpetual stretch preferred stock, a primary financing vehicle designed to trade near its stated value of $100.

Instead, STRC fell to an all-time low of nearly $71 on Friday before recovering to about $75, about 25% below par, raising questions about whether the company will be able to continue raising capital on favorable terms.

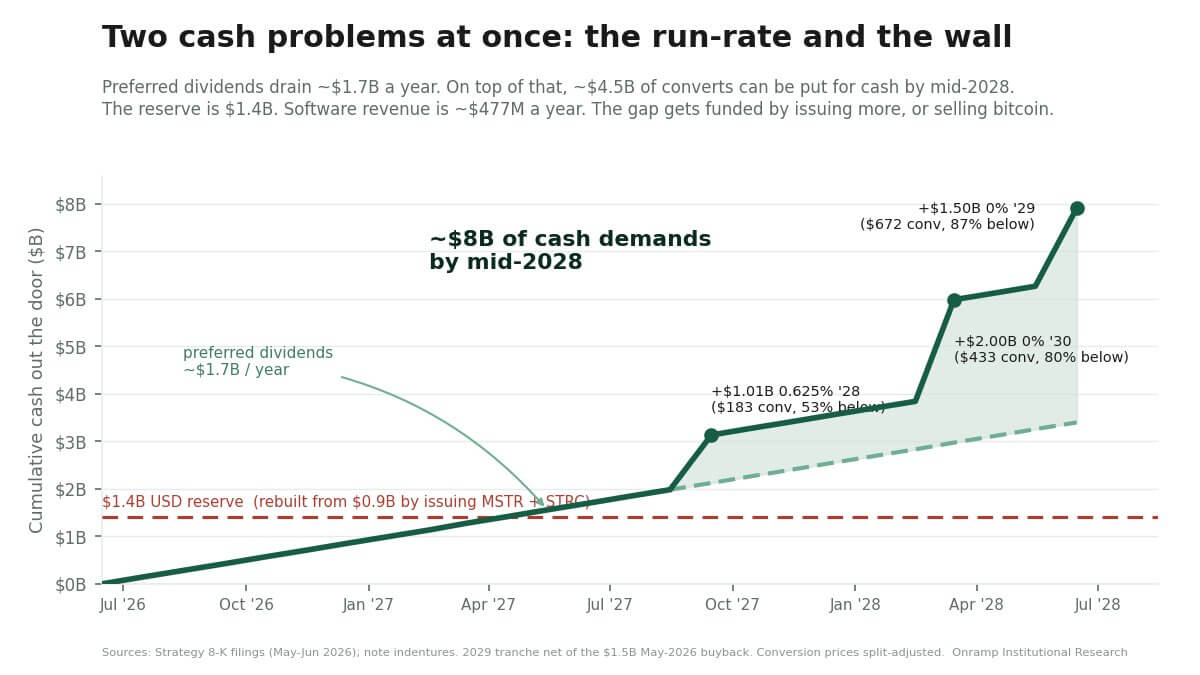

The decline comes as some market participants face an $8 billion funding barrier and strategy over the next two years, including preferred dividend debt and convertible debt that shareholders can return to the company as cash before final maturity.

This burden shifted investors’ attention from the size of Strategy’s Bitcoin holdings to the balance sheet built around it.

Strategy loses Bitcoin premium

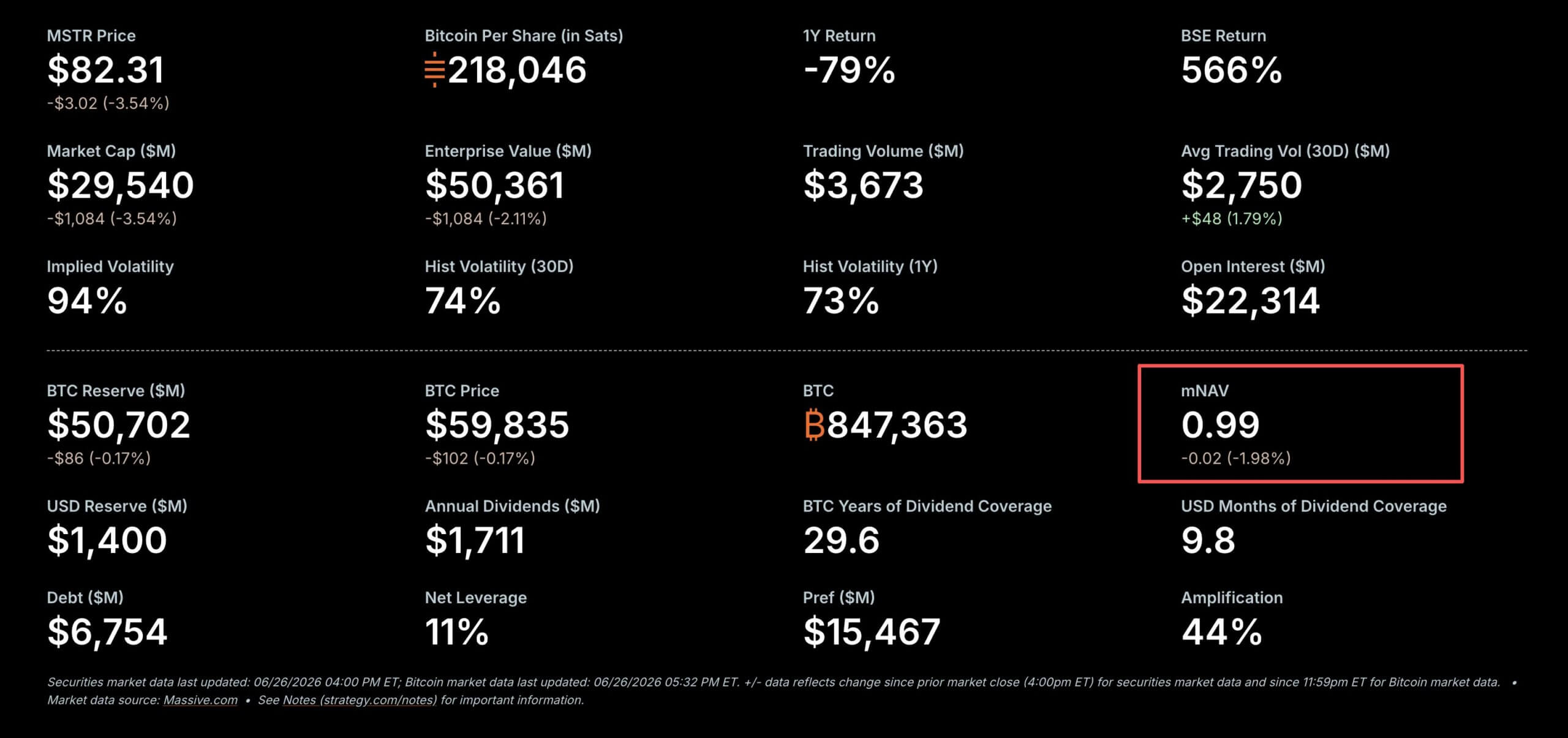

The shift became evident on Friday, when Strategy’s enterprise market-to-net asset value fell below 1, temporarily erasing the premium that had long separated the company from other corporate Bitcoin holders.

This metric is important because it looks beyond the spot value of Bitcoin in Strategy. It incorporates the company’s debt, cash, and preferred stock, giving a complete picture of how the entire structure Saylor has built around its assets is valued in the public market.

Therefore, if it is below parity, this suggests that investors are not paying extra for Strategy’s ability to accumulate Bitcoin through public market lending. Instead, they discount the complexity and cost of claims sitting in the company’s treasury.

This marks a reversal from the deals that defined Strategy’s rise. For years, the company was able to sell stocks and other securities at high valuations and use the proceeds to buy more Bitcoin.

This premium created a powerful loop in which higher market value helped fund more purchases, and more purchases strengthened the company’s position as a leading publicly traded Bitcoin agency.

But when common and preferred stocks fall at the same time, it becomes difficult to stay in the same loop.

In fact, Strategy’s common stock fell to a two-year low of $82 on Friday. Meanwhile, Bitcoin was also struggling below $60,000.

Bitcoin trends are no longer the only concern for shareholders. The question is whether Strategy can continue to access the capital markets without deepening dilution, increasing cash costs or putting pressure on its stock holdings.

Strategy faces $8 billion funds test

Meanwhile, the strategy debate is increasingly moving away from Bitcoin alone and toward the simpler question of how much cash companies will need if market conditions remain hostile.

Glenn Cameron, global head of institutions at Orrump Bitcoin, estimates that Strategy could face around $8 billion in potential cash needs over the next two years.

He said the pressure is coming from two places. One is a preferred stock stack that will be used to finance the Bitcoin purchase, and the other is a convertible note that may have to be paid back in cash if common stock prices continue to decline.

Preferred stocks already generate large run rates. Prime Minister Cameron pegged Strategy’s annual preferred dividend liability at nearly $1.7 billion, with STRC alone accounting for about $1.2 billion. This estimate is based on approximately 104.9 million STRC shares and an annualized interest rate of 11.5% on the stated value of $100 of preferred stock.

As STRC trades further below par, that distortion increases. Preferred stock is structured with a variable dividend rate that aims to keep the security close to its stated price of $100.

However, higher interest rates also increase the cost of keeping the product attractive to investors, especially if the market demands higher yields to hold junior strategy exposure.

At about $75, STRC’s effective yield has risen to about 15%, indicating that investors are looking for much higher compensation than the stated dividend rate indicates.

This does not mean that Strategy is facing an immediate liquidity event, but it does indicate that the preferred lender has moved from a cheap funding tool to a more expensive part of the capital structure.

The second pressure point is convertible debt. Prime Minister Cameron has identified around $4.5 billion worth of notes that holders could potentially return to the Strategy as cash between September 2027 and June 2028.

Potential repayment dates include approximately $1.01 billion on September 15, 2027, approximately $2 billion on March 1, 2028, and approximately $1.5 billion on June 1, 2028.

These notes become more significant if Strategy’s common stock trades well below its conversion price. If the stock remains underfunded, holders have less reason to convert to stock and more reason to seek repayment in cash if conditions permit.

This is how the funding barrier approaches the $8 billion figure. Preferred dividends are carried out behind the scenes, combined with convertible bonds that may require intensive cash.

Strategy holds approximately $1.4 billion in cash to meet this potential demand. The company has rebuilt some of that buffer after drawing down it earlier, but it did so by selling securities in a weak market. This helped maintain liquidity, but also increased the risk of further dilution.

Therefore, companies’ choices are becoming increasingly constrained. Possible options include selling common stock, issuing preferred stock, refinancing debt, delaying Bitcoin purchases, or selling some of your Bitcoin holdings.

However, none of these options are free of cost.

Issuing common stock dilutes the value of existing holders. As the number of preferred shares increases, the dividend burden increases. When strategy securities are under pressure, refinancing depends on investor appetite.

At the same time, a delay in Bitcoin purchases would weaken the accumulation story that has defined the company. Selling Bitcoin would be the most radical departure from a strategy built around indefinite accumulation.

STRC trades like “junk credit” as bears target $60

While STRC’s decline has been compared to past crypto failures, the stress in Strategy’s preferred stock is occurring through a different mechanism.

Blockchain intelligence firm Arkham Intelligence disagrees with the comparison between STRC and Terra’s LUNA, arguing that Strategic preferred stock does not function like an algorithmic stablecoin. There is no automatic peg defense mechanism, and falling below the $100 threshold will not itself trigger a liquidation event.

This distinction is important because STRC is a perpetual preferred security and not a redeemable token. It is below Strategy’s debt in its capital stack, has no set maturity date, and does not require the company to repurchase it at par on a set schedule. Dividends are cumulative, but cash payments are subject to board approval and the company’s ability to raise capital.

These features make Strategy more flexible than cryptocurrency structures built around forced redemptions and collateral liquidations. It also explains why STRC can trade well below par without causing an immediate mechanical collapse.

The market is sounding another warning. STRC is no longer valued as a security that naturally reverts to its stated amount of $100. Investors are treating this like a yield-bearing claim to the strategy’s ability to continue paying dividends, preserve cash, and raise capital while Bitcoin remains under pressure.

This has brought STRC closer to expressions that emphasize corporate credit rather than cryptocurrency-native leverage. Preferred stock, priced approximately 25% below par, reflects a higher required return for investors who take on exposure to one of the company’s junior debt obligations.

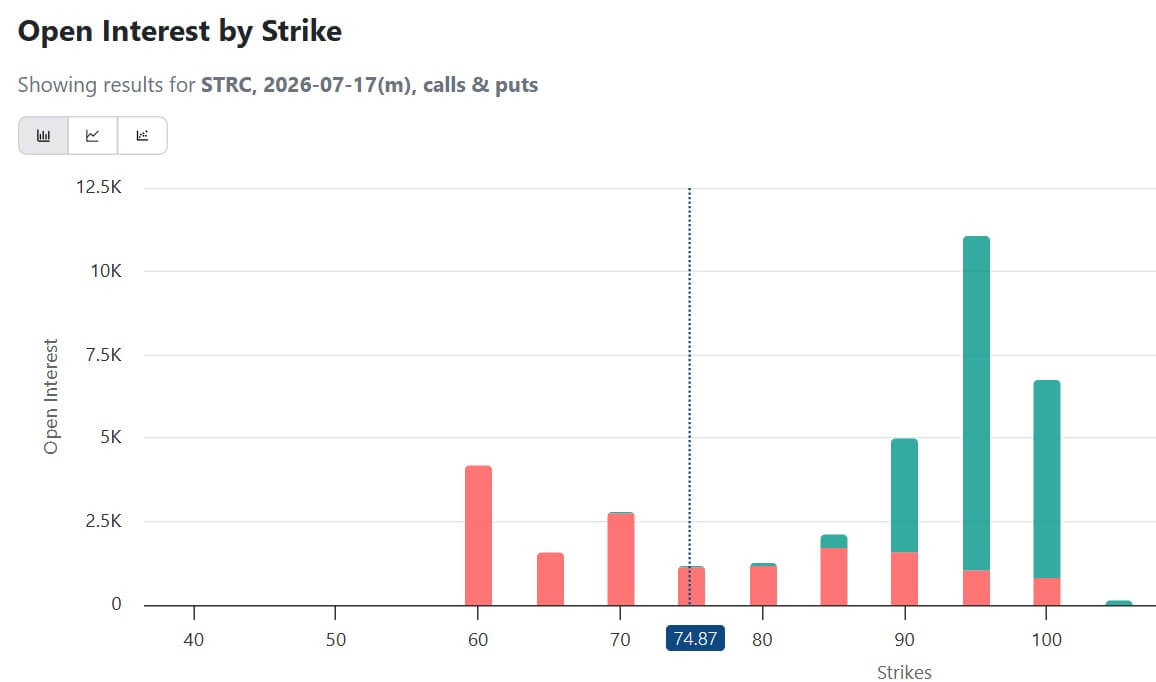

Notably, that pressure is now showing up in the options market as well. Traders have been building bearish positions around STRC, with outstanding open interest on the July 17 contract with a strike price of $60.

This positioning suggests that some investors are bracing for further declines if confidence in preferred stocks continues to decline.

Strategy’s Bitcoin model comes under criticism

The tensions across Strategy’s securities have exposed the company to harsher criticism from across the digital asset industry.

Ripple CEO Brad Garlinghouse discussed Saylor’s fundraising strategy in an interview with CNBC on Friday, arguing that the company’s reliance on preferred stock and other capital market tools is diverting attention from what ultimately brings value to digital assets.

According to him:

“Financial engineering does not drive long-term value. The long-term value of digital assets will be driven by utility.”

While Garlinghouse remains bullish on Bitcoin, he pointed to the decline in STRC as evidence that the strategy’s model is under pressure. He added:

“Michael Saylor on the team wasn’t focused on the right things, and that hurt the entire market.”

These comments highlight the widening philosophical divide in cryptocurrencies. Saylor’s approach is built around Bitcoin’s scarcity, public market access, and repeated accumulation. Garlinghouse’s critique reflects a utility-first perspective on digital assets, with an emphasis on payments, settlements, and tokenized financial infrastructure.

That disagreement has been going on for years. But what has changed is that the market is giving critics new evidence.

As long as Bitcoin rose and Strategy’s securities traded at a premium, the company’s model appeared to be self-reinforcing. It could sell securities and buy more Bitcoin, potentially capitalizing on investor enthusiasm to fund the next round of accumulation. The same structure appears more vulnerable due to lower STRC, lower MSTR, and smaller corporate mNAV.

However, Michael Saylor dismissed these concerns, saying:

“Volatility tests any capital structure. Our strategy remains focused on Bitcoin, disciplined capital allocation, credit quality, and long-term value creation.”

The next test will be whether the strategy can restore confidence without weakening what has made it one of the most important Bitcoin agents in the public markets.

(Tag translation) Bitcoin