Over the past six weeks, investors withdrew about $5.94 billion from U.S. spot Bitcoin ETFs, marking the longest streak of uninterrupted weekly outflows since these funds began operations in 2024. Galaxy Research said the worst 30-day period was the $6.35 billion loss through June 20.

Bitcoin has fallen in parallel with these redemptions, falling to a 21-month low near $58,000 after Thursday’s heavy inflation, before stabilizing around $59,000, about 53% below the record set last October at $126,080.

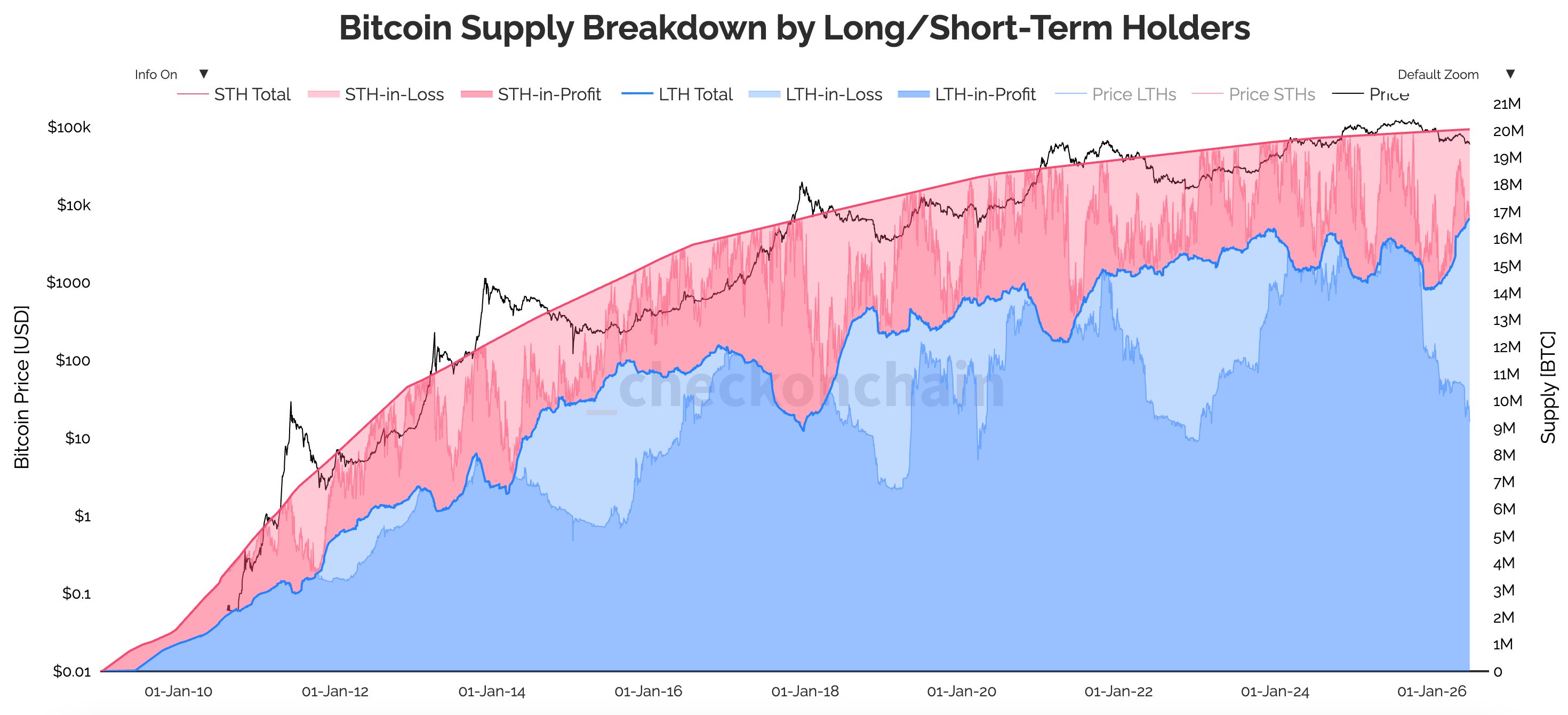

Despite the huge outflow, the focus is not on the sales themselves, but on who is actually doing the selling. While the ETF crowd is headed for the exits, those who have held Bitcoin for years remain largely unfazed. Long-term holders, those who have held for more than 155 days, own 16.64 million BTC, nearly 83% of all Bitcoin in circulation.

So while supply has been steadily building up from those who have experienced such drawdowns in the past, the selling is coming almost entirely from allocators showing up through brokerage accounts. This will be the first real capitulation for ETF holders. Because this is the first time that the rapper who ultimately brought Wall Street to Bitcoin has shown that he has lost his nerve.

Exiting the $6 billion ETF and who will actually exit?

If you look at the remaining money, you will see that it paces almost as much as the total. The first week of June was particularly dire, with $1.72 billion in outflows, but that fell to just $226.8 million in the week ending June 18, slowing by nearly 87% in a matter of weeks.

Jeff Coe, chief analyst at CoinEx, said the slowdown is a sign that the wave of selling is draining rather than strengthening, and that the worst pressures are probably already behind the market.

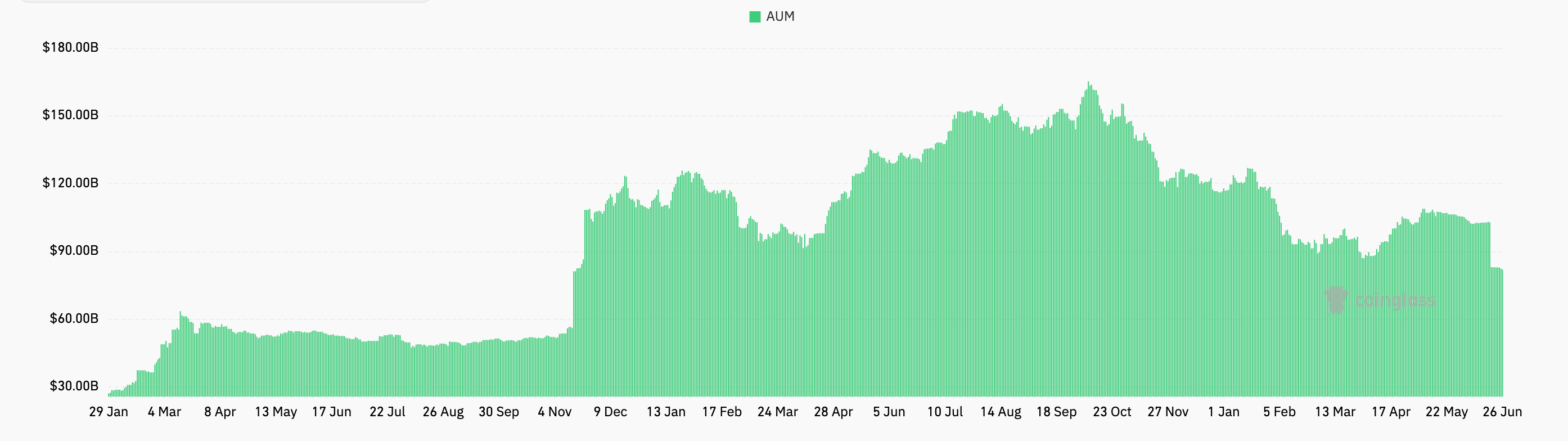

The damage to the product itself is still significant. Total assets under management fell from more than $104 billion to about $80 billion during the period, and cumulative net inflows since its inception fell from a peak of nearly $63 billion last October to about $53.4 billion now.

In other words, a year’s worth of accumulated capital is gone in a matter of weeks.

If you ask what is actually withdrawing funds, the answer seems more akin to regular portfolio management than any grandiose position on Bitcoin itself.

Deutsche Bank’s Marion Labour explains that Bitcoin is currently a risky asset for institutional investors, with ETF allocators and corporate treasuries being the marginal buyers. So when these desks decide to de-risk across the board, Bitcoin gets de-risked like everything else, and these days the de-risking of Bitcoin gets tougher.

AI is a big part of the competition here, with US tech giants planning to spend more than $700 billion on AI infrastructure in 2026. SpaceX’s IPO and attracting private companies like OpenAI and Anthropic have also become magnets for much of the speculative money that once flowed into cryptocurrencies.

If you look at where these sellers actually bought, this looks like a real capitulation. According to VanEck’s on-chain work, realized losses reached $714 million, an increase of 78% month-over-month, and the realized profit-to-loss ratio plummeted from 1.11 to 0.27, with the majority of these sellers buying between $55,000 and $68,000. This means they are locking in losses near the lower end of their range.

igcurrencynews flagged an earlier version of this same setup in May, when new redemptions exposed BTC to some of the busiest trading on Wall Street. Strategy also took part in the trimming, selling 32 BTC to cover dividend costs in its first net sale since 2022, but to be fair, the company has still amassed a large amount of net worth.

Putting all this together means that the coin will move from the newest, wobbliest hands to the most stable hands. This is more or less how the ownership base tends to reset near the end of the drawdown.

Why the price keeps falling despite the strongest hands holding

You would think that in a market where long-term holders own a record share of supply, there would be fewer Bitcoins available for sale, and that’s the case. However, it is still not possible to put the price at the lower limit. The reason is that demand and supply are separate forces. At the moment, demand is the deciding factor.

Bitcoin only trades at what buyers are willing to pay, and currently those buyers are silent. With spot volume down, on-chain activity cooling, and ETF trading volumes down to levels last seen during the early consolidation stages, float reduction can certainly stabilize prices, but without corresponding new demand, it cannot drive prices up on its own.

Creations that managed Bitcoin until 2025 are no longer flowing into the fund. This is a concern igcurrencynews raised in March when it asked who would buy Bitcoin following five consecutive weeks of ETF outflows. This demand began to crack in May, as ETF flows absorbed the first real macro shock in seven weeks.

But the remaining $6 billion is still a single digit compared to the $53 billion these funds have set aside. In the crypto slate We have previously argued that headline leakage amounts tend to overstate the actual amount of physical Bitcoin. to change hands.

Flows for long-term holders are 10 times higher than ETF flows, and these holders are still accumulating net worth amidst the weakness, so by that measure the overall decline appears to be more cyclical than structural. BlackRock has its own take on this argument, treating much of its redemption activity as product rotation within client portfolios rather than as people leaving assets.

However, in the short term, the situation still appears to be difficult. While May’s inflation numbers were in the spotlight on Thursday, with headline PCE rising to 4.1% year-on-year, the highest since 2023, Bitcoin’s reaction was immediate, with Bitcoin falling towards $58,000 and with it more than $1.2 billion in leveraged long positions across the crypto market.

Another $469 million left the fund on Wednesday alone, the largest single-day outflow since early June and the seventh consecutive week of negative outflows. On top of that, $10.6 billion of Deribit option expirations were liquidated on Friday, removing about 80% of the open interest from funds and traders flocking to $60,000 puts and $80,000 calls, all of which positioned them at the top of the level Bitcoin is trying to defend.

And with Fed Kevin Warsh already withdrawing his easing language and revising his year-end inflation forecast upwards, the market is currently pricing in a 77% chance of a December rate hike, so the macro backdrop is barely covered.

Therefore, the gap will only deepen. Allocators who came looking for clean, regulated, and convenient exposure are finding out the hard way that the convenience didn’t actually remove the volatility, and are quickly coming back at a loss. Holders who have seen this same sequence play out several times are already doing what they always do on the lows and waiting until it’s over.

Wall Street finally owned Bitcoin, but the first real lesson it taught them was measuring how much Bitcoin these new owners could carry through proper drawdowns. For a significant portion of them, the honest answer turned out to be significantly less than the amount they signed up for.

(Tag to translate) Bitcoin