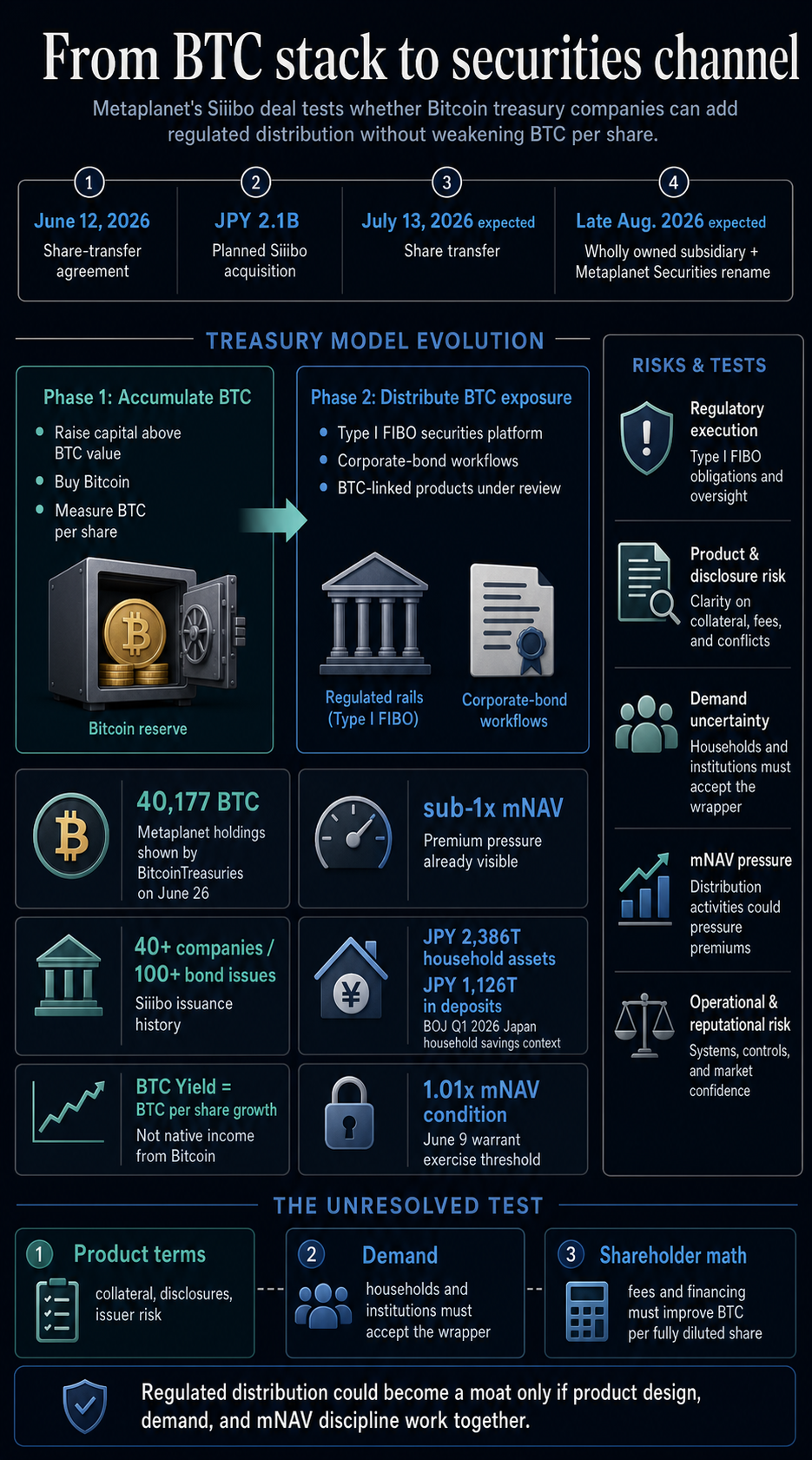

Metaplanet’s Siiibo contract transforms Bitcoin government bond trading from a matter of balance sheet accumulation to a test of regulated distribution.

The Japanese listed company has agreed to acquire Siiibo Securities, a regulated corporate bond platform, giving Japan’s largest Bitcoin-listed treasury firm a path to structuring and distributing securities as mNAV, dilution and BTC per share calculations come under pressure.

The broader issue has moved from simply copying Treasury’s strategy to building a licensed channel that can package Bitcoin exposure while preserving the BTC per share claims that made the trade attractive in the first place.

According to Metaplanet’s June 12 disclosure, the company has entered into a stock transfer agreement to acquire Siiibo for 2.1 billion yen, and after completing the necessary procedures, the stock transfer is scheduled to take place on July 13, with the company scheduled to become a wholly owned subsidiary in late August.

According to the company, Siiibo will be renamed Metaplanet Securities after its closure.

Bitcoin Treasuries’ Metaplanet profile viewed on June 26th showed that the company held 40,177 BTC, while the underlying and diluted mNAV numbers remained below 1x.

In this context, the Siiibo deal is a test of whether treasury companies can build their businesses around Bitcoin exposure, rather than relying primarily on recurring equity-linked loans.

Regulated rails and Bitcoin per share

Siiibo provides Metaplanet with a securities platform with regulatory records and operating history. Japan’s Financial Services Agency lists Siiibo Securities as a financial instruments business operator, and Metaplanet describes the company as a registered first-class financial instruments business operator that operates an online platform focused on corporate bonds.

According to Metaplanet documents, Siiibo has supported over 100 corporate bond issuances, underwritings, and solicitations for over 40 companies.

This record has operational value because this acquisition provides more than legal status. This enables issuance workflows, compliance processes, issuer relationships, and distribution experiences for investors.

The company’s supplementary materials clearly indicate that direction. Metaplanet said the acquisition is centered around “bringing yield to Japan” and that it intends to explore digital financial products such as income-oriented BTC-related products, private placement bond products, products incorporating Bitcoin-related assets, and security tokens through the Siiibo channel.

These are product concepts that are still under consideration rather than launched products, but they represent the strategic shape of this movement.

For Bitcoin treasury companies, the difference is important. Passive financial models rely on access to capital and the market’s willingness to value a company above BTC.

The brokerage platform creates fees, distributions, product design, and direct access possibilities for investors who want Bitcoin-related exposure in a regulated wrapper.

The yield language also requires an accurate denominator. On its about page, Metaplanet states that BTC yield is a key performance metric, defining it as Bitcoin per share growth.

This metric measures balance sheet growth rather than income paid by Bitcoin itself.

If Metaplanet ultimately offers a yield-style Bitcoin product, its income will need to be derived from a disclosed structure around BTC, such as credit spreads, loan collateral, option premiums, issuer risk, tokenized security arrangements, or another defined mechanism.

Bitcoin itself does not generate native coupons.

MetaPlanet’s June 9 warrant disclosure shows why that distinction is central to the model. The company has revised the minimum exercise conditions for the 27th stock acquisition rights so that they can only be exercised if mNAV is 1.01 times or more.

Metaplanet said this condition is aimed at avoiding exercises that are unlikely to increase the value of each Bitcoin share and could cause dilution.

This is the same pressure that all finance companies face when the low premiums wear off. Issuance may increase if the stock trades at a significant premium to BTC value.

If the premium compresses or disappears, the same funding tool could dilute existing rights on the Bitcoin stack.

Product businesses may add a second engine, but should be judged on the same denominator: fully diluted BTC per share before fees, debt, first-class claims, and operating costs.

Japan’s savings market changes course

Metaplanet’s strategy diverges from the strategy’s capital markets model by adding a licensed Japanese securities platform and fixed income product ambitions.

While the strategy remains the reference point for the scale version of Bitcoin accumulation by public companies, Metaplanet’s Siiibo move is more domestic and distribution-driven.

It is built around regulated securities distribution, corporate bonds, and a savings market with an unusually large cash base.

According to the Bank of Japan’s Flow of Funds Data Report for the first quarter of 2026, the financial assets held by households as of the end of March were 2,386 trillion yen, of which 1,126 trillion yen was held in currency and deposits.

This large number of deposits explains why companies are seeking regulatory compliance for Bitcoin-related products denominated in yen or distributed in Japan.

A large savings pool indicates a ready market rather than a confirmed demand.

The final product terms will determine whether the proposal is more of an issuer risk product with straight exposure, structured credit, leveraged yield, tokenized claims, or Bitcoin branding.

This is where Treasury transactions become more complex. Publicly traded companies can hold Bitcoin in a way that is traceable to their shareholders.

While regulated product platforms may expand access and potentially generate fee income, they also introduce product-level risks, disclosure obligations, questions regarding suitability for distribution, and potential liabilities separate from the BTC reserves themselves.

The broader Bitcoin treasury sector of public companies has also grown large enough for these questions to become important across multiple issuers.

BitcoinTreasuries tracks approximately 199 public companies holding approximately 1.264 million BTC, and capital structure and valuation discipline is not a single company issue.

With recent reports on the financial company’s shareholder cost and Strategic’s financing pivot, the discussion has already moved beyond the headline accumulation to questions of financing terms, dilution, senior debt, and whether fully diluted BTC per share will actually improve.

The acquisition of Metaplanet is a new version of the same argument. If a treasury company needs Bitcoin-related business operations, the quality of those businesses will be as important as the size of the Bitcoin pile.

Product design shapes results

Metaplanet’s Siiibo move suggests the Bitcoin treasury company is testing the transition from an accumulation vehicle to a financial products company.

That advantage will come from licensing, distribution, trust, publisher relationships, product design, as well as having BTC on public balance sheets early on.

This could be a positive for Metaplanet if the company uses Siiibo to build a transparent, affordable product that generates revenue while supporting a BTC per share strategy.

Additionally, new risks could arise if the yield language draws investors into structures where returns depend on leverage, credit exposure, collateral conditions, or issuer obligations that are more difficult to understand than spot exposure to Bitcoin.

The next check is specific. The planned stock transfer date of July 13th and the conversion into a subsidiary in late August will determine whether the platform acquisition will be completed as planned.

Product filings, term sheets, collateral rules, risk disclosures, distribution limits, and customer demand will indicate whether Metaplanet Securities will become a real operating engine.

For the broader finance sector, the lessons are bigger than one Japanese deal.

If mNAV premiums are high, the model looks simple. Just issue shares, buy Bitcoin, and repeat. As premiums compress, businesses need stronger answers.

Metaplanet seeks to provide an answer through licensing distribution and yield-style product design.

The outcome will depend on whether these regulated channels actually improve the economics of ownership for shareholders.

Securities distributions could be the next moat for Bitcoin treasury companies if they can generate lasting fees, disciplined product demand, and increased BTC per share.

If complexity increases around volatile reserve assets, markets may treat the move as another form of leverage with a regulatory guise.

(Tag translation) Bitcoin