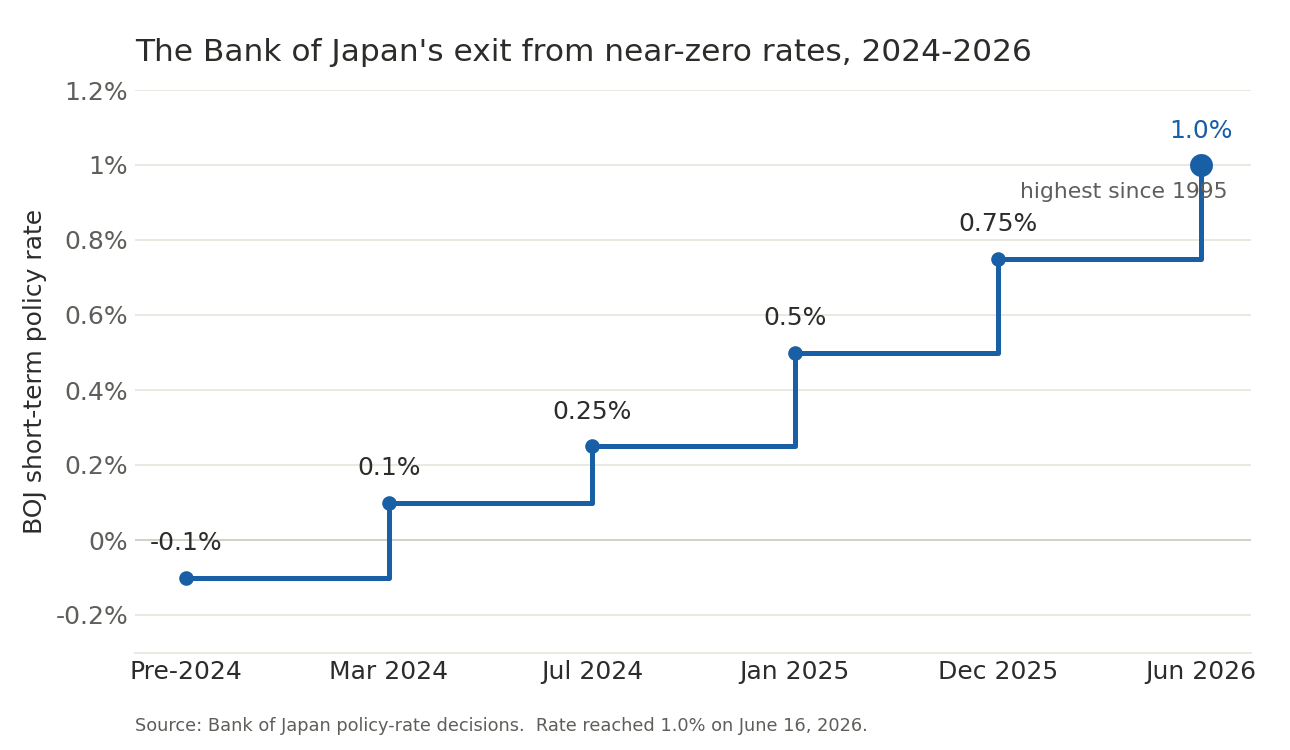

The Bank of Japan raised its benchmark interest rate to 1% on June 16, the highest level the country has seen since September 1995 and the furthest point in a normalization campaign that has slowly dismantled three decades of nearly free money.

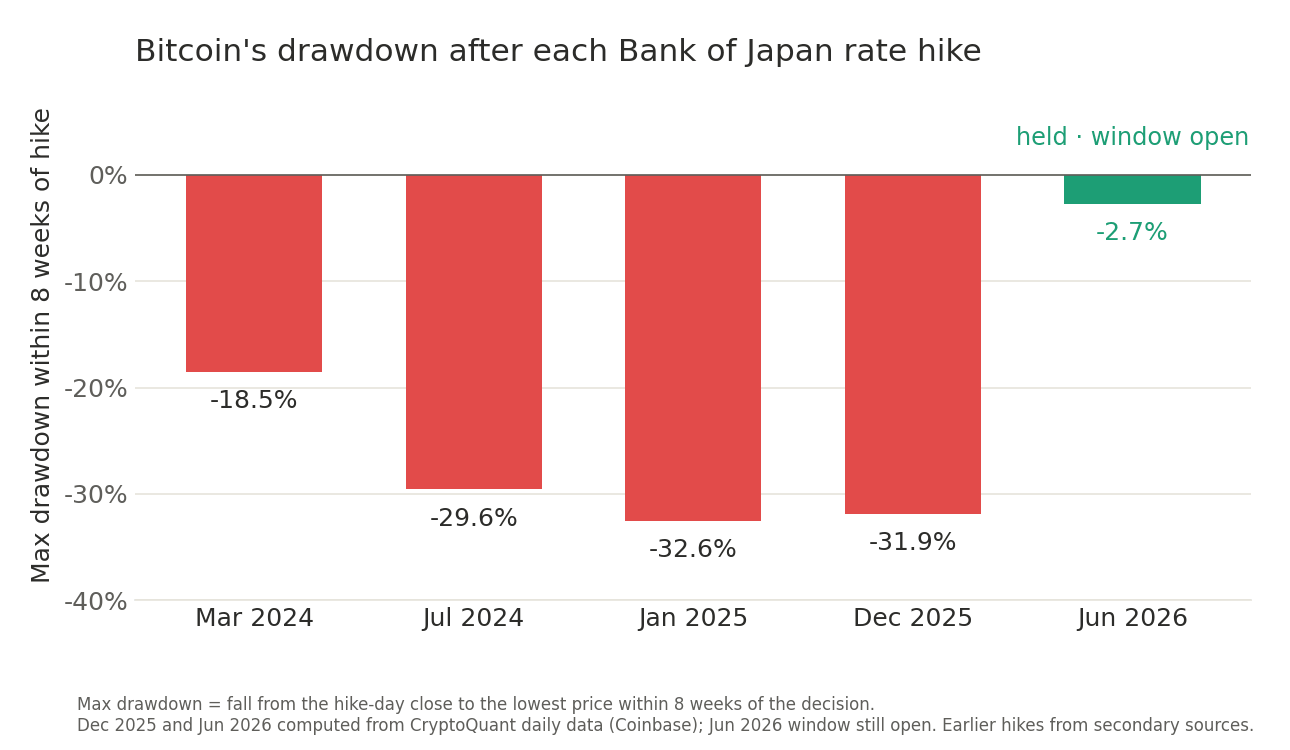

In making this decision, the track record was pointing in a certain direction. Since March 2024, each rate hike by Governor Kazuo Ueda has been accompanied by a drawdown of 18% to 33% for Bitcoin, and in August 2024, when the rate hike was abrupt, the price rose from about $64,000 to $49,000 within 48 hours, erasing about $600 billion in virtual currency market value.

This time, the pattern broke, with Bitcoin briefly falling in Asian trading before recovering to around $66,000, near its pre-announcement level.

Japan’s monetary policy has reached Bitcoin through one of the most powerful financing channels in global finance, and the quarter-point rally to a 31-year high is unlike anything that has happened to cryptocurrencies before. The rate hike was carried out without the usual disruption due to how the Bank of Japan packaged it, but the calm left much bigger questions about the direction Japan’s exit from a cheap currency will ultimately take.

Why the Bank of Japan’s interest rate decisions are reflected in virtual currency examinations around the world

For most of the modern crypto era, Japan was the cheapest source of capital on the planet. Investors borrowed yen at interest rates fixed near zero, exchanged the proceeds for dollars or other high-yield assets, and pocketed the difference. This is a structure known as a yen carry trade.

The borrowed funds were invested in U.S. stocks, emerging market bonds, and virtual currencies, and macro funds that used the same leverage to short the yen often held long positions in Bitcoin at the same time.

When Japan’s interest rates rise, its trade collapses. Currencies tend to strengthen as the cost of borrowing in yen increases, and funds with leveraged positions may be forced to simultaneously reduce all exposures they hold.

Bitcoin trades around the clock and sits on a leveraged book that needs to be funded quickly, so it will almost always absorb that sell-off first. We saw it in August 2024, when one sudden price increase wiped out a large portion of the crypto market in two days, setting off a chain reaction that led to over $1 billion in liquidations.

Energy costs and a weaker yen are driving the Bank of Japan’s decision to act now, with Japan’s producer price index rising 6.3% in May from a year earlier, the fastest pace in more than three years, due to oil costs related to the U.S.-Iran conflict. The headline inflation rate in April was 1.4%, falling below the central bank’s target of 2% for the fourth consecutive month, although it was controlled by government policies such as abolishing the gasoline tax and making public high school tuition free.

The Bank of Japan is raising interest rates as inflation remains below target. This shows how concerned policymakers are about energy prices spilling over into daily necessities and about the yen’s decline toward the 160 yen to the dollar level that previously prompted intervention. The increase was approved by a 7-1 majority at the board meeting, with Ueda absent due to hospitalization and Vice Governor Shinichi Uchida attending the press conference.

Market positions ahead of the meeting heightened risk on both sides, as speculative short yen positions had grown to about 115,000 contracts, the highest level since November 2017, and a rise in the yen could force a painful unwinding of risk assets across the board.

The opposite view was also supported, as data from the Bank for International Settlements showed that yen-denominated foreign currency credit contracted by 4.9% during 2025, and the carry complex underpinning global leverage was smaller than when it exploded in 2024, softening the impact of forced withdrawals.

Why Bitcoin rose this time and why the next rally will be a real test

Bitcoin was put on hold due to one feature buried in the announcement. Along with the interest rate hike, the Bank of Japan temporarily suspended the reduction in its purchases of government bonds and pledged to purchase about 2 trillion yen of government bonds every month starting in April 2027, a move seen by markets as an effort to limit upward pressure on long-term yields even as short-term policy tightens.

Japan’s long-term interest rates are a real pressure point for global leverage, and capping them blunted what would have been a purely hawkish policy decision. In any case, the rate hike is almost fully priced in, with market odds of over 90% in the days leading up to it, and the risk of an energy shock has been somewhat averted due to the subsidence in the US-Iranian conflict.

After this decision, the Nikkei Stock Average rose 0.46% and the yen rose only slightly against the dollar to 160.22 yen, both of which are consistent with the market reading that the package is being restrained.

Japan’s weight in cryptocurrencies is due to much more regulation and funding than actual trading volume. The country operates one of the oldest licensing regimes for crypto exchanges, with around 16 licensed facilities including bitFlyer, Coincheck, Bitbank, GMO Coin and BTCBOX, serving as a large and experienced retail base.

IMARC valued the country’s cryptocurrency exchange market at approximately $3.66 billion in 2025, and projected it to reach approximately $28.07 billion by 2034, with a compound growth rate of over 25%. Tokyo continues to strengthen its regulatory framework, and on June 11, Japan’s lower house passed a bill that would treat digital assets more like securities. Japan views Bitcoin primarily as a highly regulated yen-linked nexus within a much larger global liquidity system.

The effects of continued tightening will be felt far beyond Tokyo. If the Bank of Japan continues to raise interest rates, leverage from yen funds will become less attractive and the pool of borrowed money flowing into risk assets will shrink.

Rising yields in Japan could pull capital back home and force global investors to rethink their bond allocations, and stress in bond markets tends to spill over into stocks and cryptocurrencies. Japan’s normalization also becomes a second gauge of global liquidity for crypto traders, in addition to the Federal Reserve, which still gets most of the attention.

The real risk is cumulative, and while a single 1% price increase could leave Bitcoin intact, a series of price increases could reshape the cheap money context that allowed the expansion of risk assets in the first place.

Bitcoin’s lull on June 16 was due to a dovish bond market rally that was well anticipated by traders and failed to rein in the market’s risk appetite.

The more stringent test results came within a day, and they came from Washington. On June 17, the Fed kept interest rates unchanged at 3.75% from 3.5%, but Kevin Warsh used his first meeting as chairman to remove any easing bias from his statement, raising the year-end dot plot median to 3.8%, with 9 of 18 officials now expecting at least one rate hike in 2026, and PCE inflation expectations raised to 3.6%.

Bitcoin saw this as a real threat, and even though the stock price rose with the signing of the US-Iranian peace deal, it fell towards $64,000 by June 18th, with the Spot Bitcoin and Ether ETFs losing a combined $111 million on the day of the decision.

The carry trade stress test passed with flying colors, and the tightening that was warned about came from the other side of the Pacific anyway. Japan’s era of near-free money won’t disappear in one afternoon, but every step away from it redraws the liquidity map on which Bitcoin is traded internally.

(Tag translation) Bitcoin