$1.78 trillion asset management firm Franklin Templeton is pushing cryptocurrencies deeper into its traditional investment portfolio with a new proposal that would automatically direct stock dividends toward exposure to Bitcoin.

On June 18, the asset manager filed documents with the U.S. Securities and Exchange Commission (SEC) to launch two exchange-traded funds that will hold U.S. stocks while allocating corporate dividends to digital asset investments.

The proposed funds, Franklin US Equity Bitcoin DRIP Index ETF and Franklin US Innovation Bitcoin DRIP Index ETF, would combine one of Wall Street’s most established practices, dividend reinvestment, with exposure to the world’s largest cryptocurrency.

This structure allows investors to base themselves primarily on large-cap U.S. stocks while slowly accumulating Bitcoin-related assets using the income generated from those companies. This design avoids the need for investors to make direct upfront payments into cryptocurrencies and instead builds positions over time through a rules-based mechanism.

The filing reflects how major financial institutions are considering more complex portfolio products beyond standard spot Bitcoin funds.

After the first wave of U.S. spot Bitcoin ETFs solved fundamental access issues, issuers are now experimenting with strategies that wrap the asset within an income, options, and allocation framework familiar to financial advisors and brokerage investors.

Notably, Franklin is already active in the digital asset market through the Franklin Bitcoin ETF, which trades under the ticker EZBC. The fund has attracted about $330 million in cumulative net inflows and manages about $360 million in assets, giving the firm a foothold in a category dominated by larger rivals.

The new filing suggests Franklin is exploring a more professional lane. Rather than competing solely with Bitcoin spot wrappers, the company is offering products that appeal to investors who are used to stock ETFs but aren’t willing to buy Bitcoin directly.

Dividends become the entry point for Bitcoin

The two proposed ETFs function as passive index trackers built around the VettaFi benchmark.

The Franklin US Stock Bitcoin DRIP Index ETF seeks to mirror the VettaFi US Large Cap 500 Bitcoin DRIP Index. The company’s stock portfolio will be tied to the 500 largest U.S. companies by market capitalization.

The Franklin US Innovation Bitcoin DRIP Index ETF tracks the VettaFi US Innovation 100 Bitcoin DRIP Index, which tracks the 100 largest non-financial companies listed on the Nasdaq Stock Market.

Both funds will invest at least 80% of their net assets in the securities that make up their respective indexes and Bitcoin-related products that correspond to each index’s crypto asset allocation. At launch, each index starts with a 95% allocation to stocks and 5% allocation to Bitcoin.

It features a reinvestment mechanism. If the underlying stock distributes regular or special dividends, those dividends will be automatically reinvested into Bitcoin-related assets at the market open following the ex-dividend date.

This allows the company’s income to fund its crypto exposure. The selling point for investors is not simply the price increase from Bitcoin, but the automatic accumulation from the dividend stream of US companies.

Franklin built restrictions into the design to prevent Bitcoin from overtaking its equity base. Upon quarterly review, if the Bitcoin allocation exceeds 5%, it will be reduced to 4.5%. If the allocation remains below 5%, there will be no downward adjustment.

The index also includes an emergency limit. If Bitcoin exposure exceeds 20% due to a sharp rally during the scheduled review, the allocation will be reduced to 4.5% by the close of trading two business days after the threshold is breached.

The capital portion, on the other hand, has its own concentration limits. The cap for individual stocks is 20%, but the total weight of companies with more than 5% cannot exceed 40%. These rules are designed to ensure that the fund does not become overly dependent on a few megacap stocks or on Bitcoin itself.

Mr. Franklin did not disclose the fund’s ticker, listing exchange, fees or expense ratio. The prospectus also states that the securities may not be sold until the registration statement becomes effective.

Franklin Advisory Services LLC will act as investment manager and Franklin Templeton Institutional LLC will act as sub-adviser. Listed portfolio managers are Dina Ting, Hailey Harris, Joe Diederich, and Basit Amin.

Franklin gives himself several routes to crypto exposure

The SEC filing gives Franklin flexibility in how the fund acquires Bitcoin exposure.

The Fund may use exchange-traded products backed by Bitcoin, including products sponsored by affiliates of Franklin.

You may also invest through other investment companies that offer Bitcoin exposure, futures contracts, options, depositary receipts representing ownership of Bitcoin, or investments held through wholly owned subsidiaries in the Cayman Islands.

This subsidiary is central to the proposal’s tax structure. Each Fund may invest up to 25% of its total assets through a Cayman-based entity designed to help income or gains from certain Bitcoin-related investments qualify as “good income” under the U.S. Internal Revenue Code.

Maintaining regulated investment company status is important to the expected tax savings from ETF products. Franklin said it intends to limit its investments in subsidiaries to stay within diversification requirements at the end of each quarter.

This structure also introduces vulnerabilities. The filing warns that future Internal Revenue Service guidance, Congressional legislation or changes in tax treatment could disrupt the strategy.

If that happens, the fund may need to change its investment approach. Depending on the circumstances, the board may approve a change in strategy or liquidation.

The tax section shows the complexity behind what seems like a simple consumer idea. The headline pitch is easy to understand. Stocks generate dividends, and those dividends increase your exposure to Bitcoin.

Implementation requires a hierarchical structure that includes ETPs, derivatives, index rules, and offshore subsidiaries.

Risk follows Bitcoin into wrapper

Franklin’s prospectus makes clear that placing Bitcoin in an equity ETF structure does not eliminate the asset’s volatility.

The filing explains that Bitcoin’s history is limited compared to stocks, bonds, and monetary products. It also characterizes digital asset markets as highly speculative and warns that regulatory changes, declining trust, technology failures, network disruptions, or competition from other digital assets could cause the price of Bitcoin to plummet.

The document also raises concerns about market structure. Many digital asset exchanges operate with less oversight than traditional stock exchanges, creating risks related to manipulation, fraud, theft, and restrictions on investor avenues.

Concentration of Bitcoin ownership is also an emerging concern. A significant amount of Bitcoin is held by a relatively small number of large holders, often referred to as whales. Large sales or transfers by these investors can have a significant impact on market prices.

Custody increases the risk even more. Digital assets rely on private keys and specialized security systems, making them vulnerable to hacking, malware, operational failures, and loss. Franklin also warned that bankruptcy resolution for digital assets can still be uncertain, and legal complexities could increase if a custodian or service provider goes bankrupt.

The Fund will face additional risks from the instruments used to track Bitcoin exposure. Spot Bitcoin ETPs are not registered under the Investment Company Act of 1940 and do not offer the same protections as traditional registered funds. Futures, options, and swaps are subject to leverage, counterparty exposure, tracking errors, and possible losses in excess of your initial investment.

These disclosures are important because the proposed product is designed to make Bitcoin feel more accessible to traditional investors. Familiar wrappers do not change the fundamental risk profile of digital assets.

Bitcoin ETF race shifts from access to design

Franklin’s filing comes as the Bitcoin ETF market enters a more complex phase, with issuers looking to build new products around an asset class that has already moved quickly into mainstream portfolios.

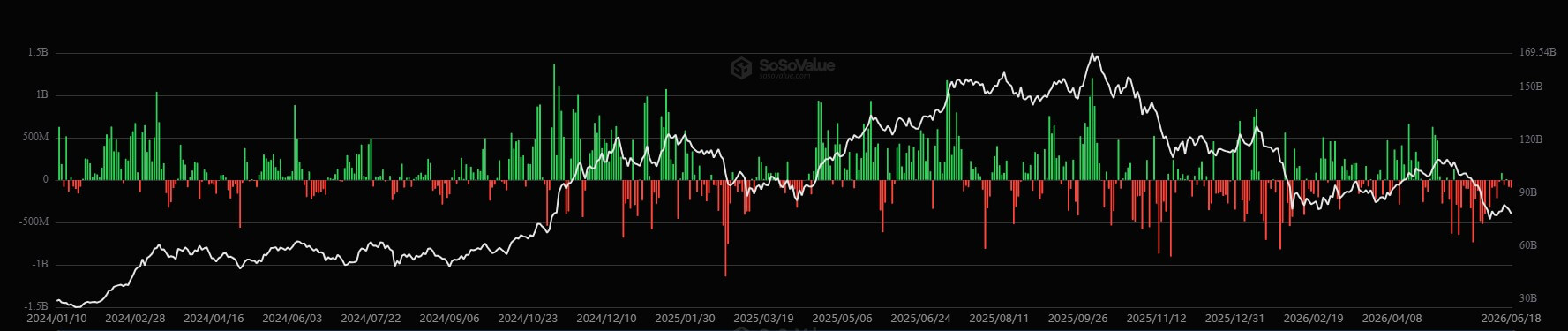

Since its inception in 2024, the U.S. Spot Bitcoin ETF has attracted $53.4 billion in net inflows since its inception and holds $78.32 billion in assets, according to SoSoValue data.

These numbers reflect how quickly the product has pulled Bitcoin into brokerage accounts, model portfolios, and institutional allocation strategies.

However, recent flow conditions have weakened. Roughly $6 billion has flown out of the fund over the past six weeks as outflows continue.

This combination of scale and new pressures is pushing issuers beyond simple spot exposure. The first wave of Bitcoin ETFs gave investors regulated access to the asset. The next wave will focus on shaping how Bitcoin fits into broader portfolios.

BlackRock is already moving in that direction with its iShares Bitcoin Premium Income ETF, which trades under the ticker BITA. This actively managed fund aims to provide Bitcoin exposure while generating monthly option premiums by writing call options on IBIT, BlackRock’s Spot Bitcoin ETF, across approximately 25% to 35% of its portfolio.

This strategy is aimed at investors who seek cash flow from Bitcoin’s volatility, rather than having only directional exposure to Bitcoin’s price. Franklin’s proposed DRIP fund would take a different route, using stock dividends to build a capped Bitcoin allocation over time.

Together, these products represent a new phase in the Bitcoin ETF market, with issuers now competing to define whether their assets belong in income strategies, equity portfolios, savings products, or other parts of traditional wealth management.

(Tag translation) Bitcoin