Bitcoin’s biggest buyers are no longer acting like a reliable backstop for the biggest cryptocurrency.

Exchange-traded funds (ETFs) that helped define the institutional era of markets, publicly traded Treasurys, and Bitcoin-related stocks are showing signs of strain, just as the world’s largest digital asset struggles to maintain one of its most-watched price levels at $60,000.

This sustained drawdown has prompted a broader reassessment of the role of cryptocurrencies in institutional investor portfolios, raising questions about whether the current environment reflects temporary profit-taking or a structural retreat from digital assets.

Bitcoin ETF demand is facing headwinds

The clearest reversal comes from the US Spot Bitcoin ETF, which has become one of the market’s most important demand drivers going into 2026.

For most of the period following its January 2024 debut, the fund was treated as evidence of Bitcoin’s steady adoption by traditional financial investors.

Their influx helped create a simple bull market theory that states that access to Wall Street will bring more money into fixed supply assets, providing a permanent source of upward pressure on Bitcoin.

However, this theory has been thoroughly tested in recent weeks.

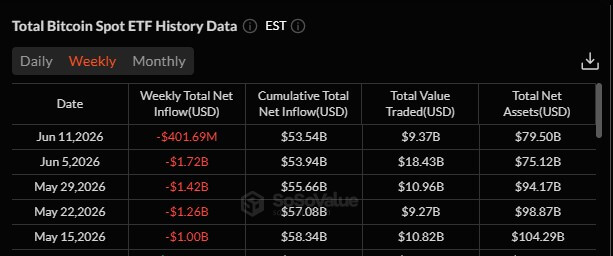

U.S. Spot Bitcoin ETFs have recorded total outflows of more than $5 billion for five consecutive weeks, according to data from SoSoValue.

This is further supported by data from Glassnode, which shows that the 30-day moving average of net ETF flows has fallen to -2,450 BTC per day, the fastest sustained pace of outflows since the product launch.

The size of that flow is significant because it exceeds the network’s daily supply of newly created Bitcoin.

After the halving in 2024, miners will produce approximately 450 BTC per day. The ETF’s continued outflows of 2,450 BTC per day are more than five times the new supply, turning what was once a sink into a source of pressure.

In volatile markets, it’s not uncommon for ETFs to be sold short-term. A negative 30-day moving average carries more weight because it filters out day-to-day noise and captures broader changes in location. Until this trend improves, institutional capital flows are unlikely to support Bitcoin prices.

Additionally, ETF trading has cooled down. The 30-day moving average of daily volume for the US Spot Bitcoin ETF fell from $4.4 billion in October to about $960 million, a 78% decrease, Glassnode reported.

This decline suggests more than simple profit-taking. This indicates that speculative demand from traditional market participants is waning even as redemptions accelerate.

Low volume can make it harder to absorb price fluctuations because there are fewer buyers available when selling intensifies.

BTC DAT loses momentum

The ETF reversal coincided with a slowdown in digital asset treasury companies, another major source of bitcoin demand.

These companies are often publicly traded, raising capital or leveraging the resources of their balance sheets to accumulate Bitcoin as a treasury asset. These gains have expanded institutional adoption beyond ETFs and given investors another way to express their demand for Bitcoin through the stock market.

Similar to ETFs, the buying disappeared in June.

Analysts at Glassnode noted that while these companies remain net buyers overall, daily cumulative amounts have slowed to a fraction of the pace seen at the beginning of the quarter.

According to them:

“Business savings have slowed sharply, with net inflows falling from a peak of more than $500 million a day to near zero levels since June.”

With ETF flows also negative, this slowdown in buying removes one of the market’s clearest sources of demand growth.

Some of the concerns center on Strategy Inc., Bitcoin’s largest public company holder. The company revealed that it sold 32 BTC in the last week of May, a small amount compared to its overall holdings, but a symbolically important move given its role in popularizing Bitcoin financial models for businesses.

The strategy then returned to the market during the decline and purchased approximately $100 million worth of Bitcoin. However, this purchase did not stop the price from dropping below $60,000.

Other BTC-focused companies are also attracting attention. Fold and Nakamoto have sold some of their Bitcoin holdings, raising concerns that Treasury-corporate transactions are no longer as unidirectional as they were during the upswing.

While these sales do not represent a broad pullback by corporate buyers, they do signal that some treasury companies are becoming more selective, liquidity-focused and willing to adjust positions as market conditions worsen.

This change is important because corporate financial models depend in part on trust. When stock prices are strong and investor demand is high, companies can raise capital to buy Bitcoin and benefit from the perception that they are leveraged agents of the asset.

However, as Bitcoin falls and demand for stocks weakens, this model becomes difficult to sustain.

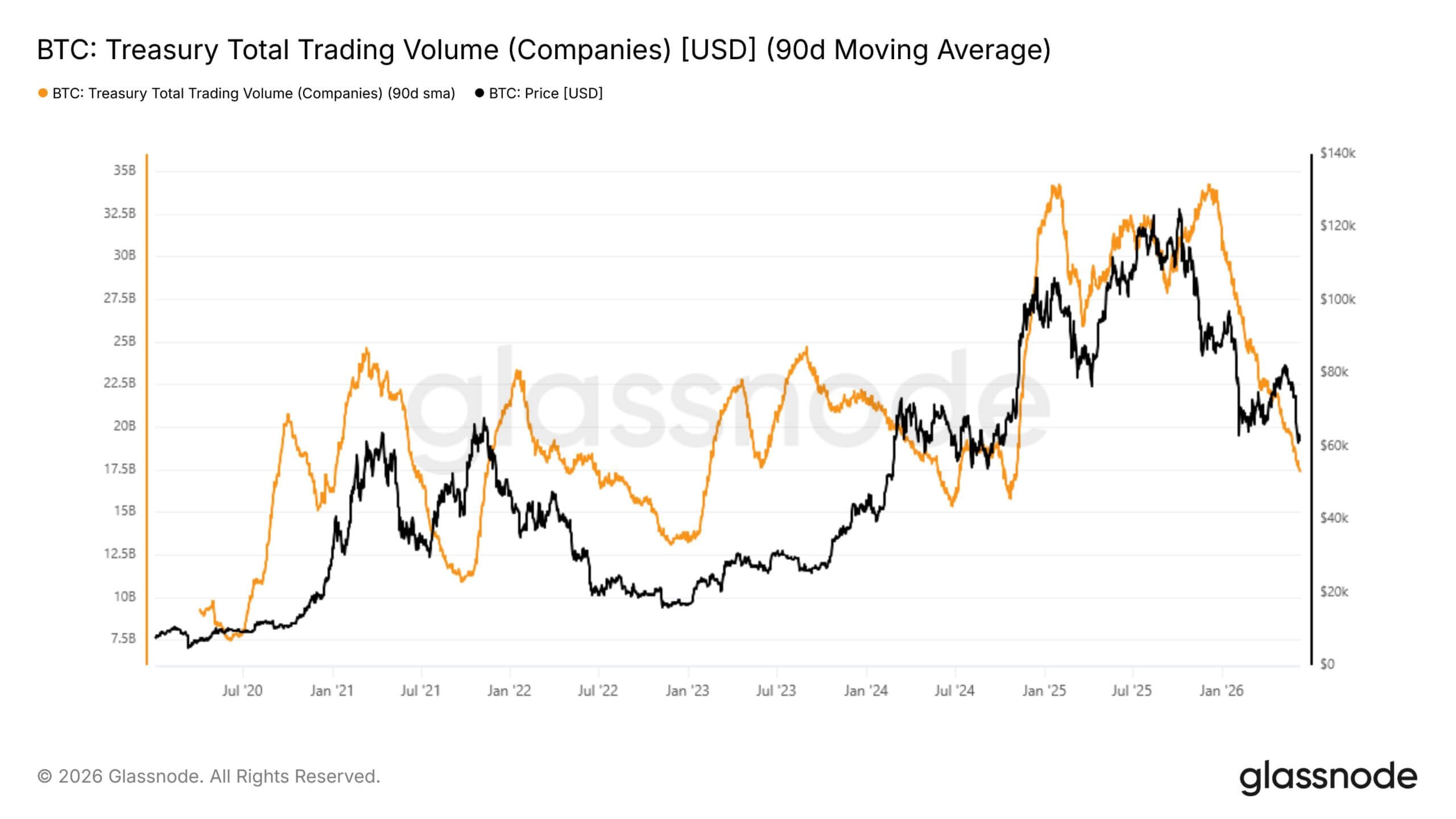

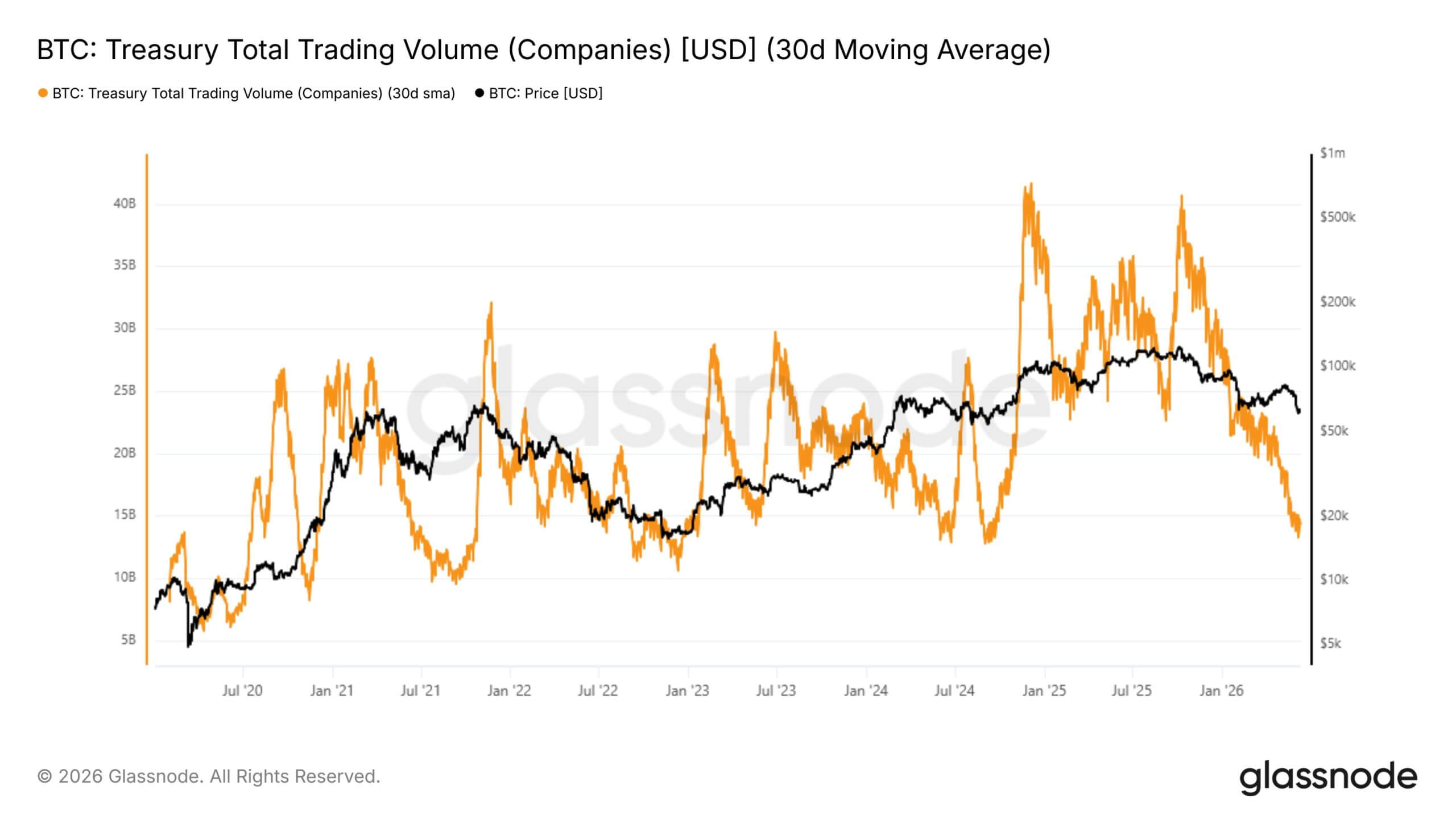

Meanwhile, the slowdown is also evident in the trading activity of the stocks of these companies.

Glassnode data display The total daily trading volume of major publicly traded Bitcoin-holding companies decreased by 49% year-over-year, as measured by a 30-day simple moving average. About 6 months. Its deal value has fallen from $34.2 billion in December to $17.4 billion at the time of writing.

This decline suggests investors are exiting Bitcoin proxy trading more broadly, not just the asset itself.

During strong market times, public Bitcoin holders often attract investors looking for leveraged exposure. Because of their combination of government bond holdings, business operations, and capital market selectivity, their stock prices could rise faster than Bitcoin if conditions improve.

As such, it has become a popular method for traders who want to use cryptocurrencies in the stock market without directly owning the tokens. However, as Bitcoin corrected, its demand weakened significantly.

Currency inflows indicate anxiety across the market

Institutional distribution creates an environment of widespread market anxiety, affecting participants across the wealth spectrum.

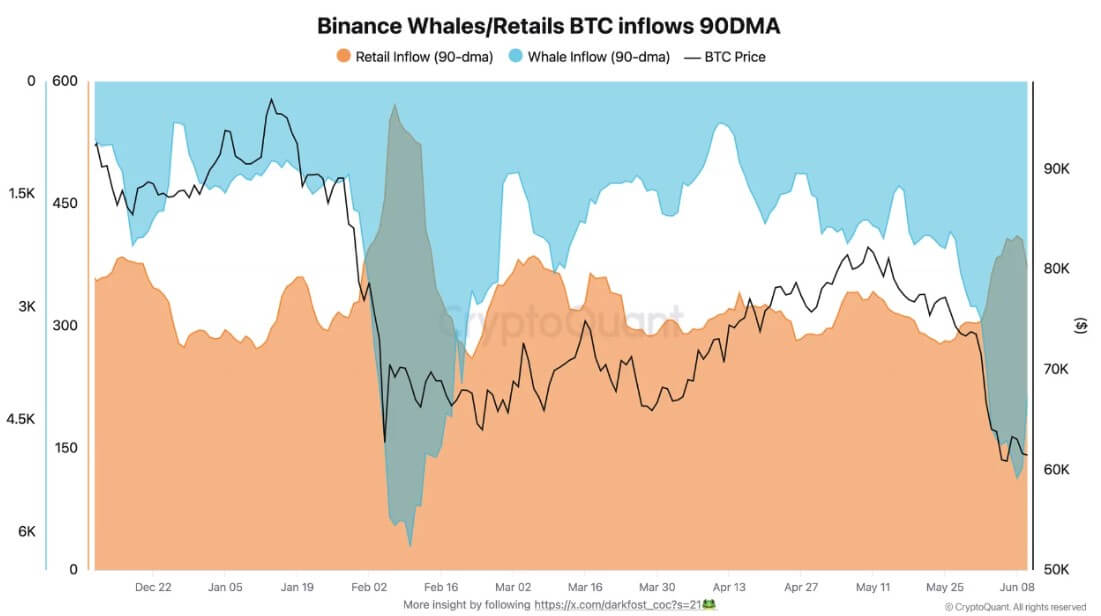

CryptoQuant data shows a significant increase in exchange deposits from both large holders and retail investors. Such deposits are usually associated with an intention to sell.

Once Bitcoin briefly breached the $60,000 floor, large holders, or “whales,” accelerated the movement of assets to trading platforms.

Over the past three months, whale inflows to the Binance exchange have averaged 5,280 BTC per day, a sharp increase from the daily average of 1,900 BTC observed in March. Retail investors are also reflecting this change in behavior, with average daily forex inflows rising to 410 BTC.

This parallel movement highlights how macroeconomic uncertainty levels the playing field regarding investor sentiment.

The current environment is a major event, marking the second time this year that foreign exchange deposits have soared. A similar pattern appeared in early February when Bitcoin tested the $60,000 threshold, with whale inflows surging to 6,200 BTC and retail inflows reaching 570 BTC.

Periods of heightened market stress such as this historically encourage the transfer of assets from short-term speculators to long-term holders, but the immediate effect is significant downward pressure on prices.

Thin market awaits catalyst

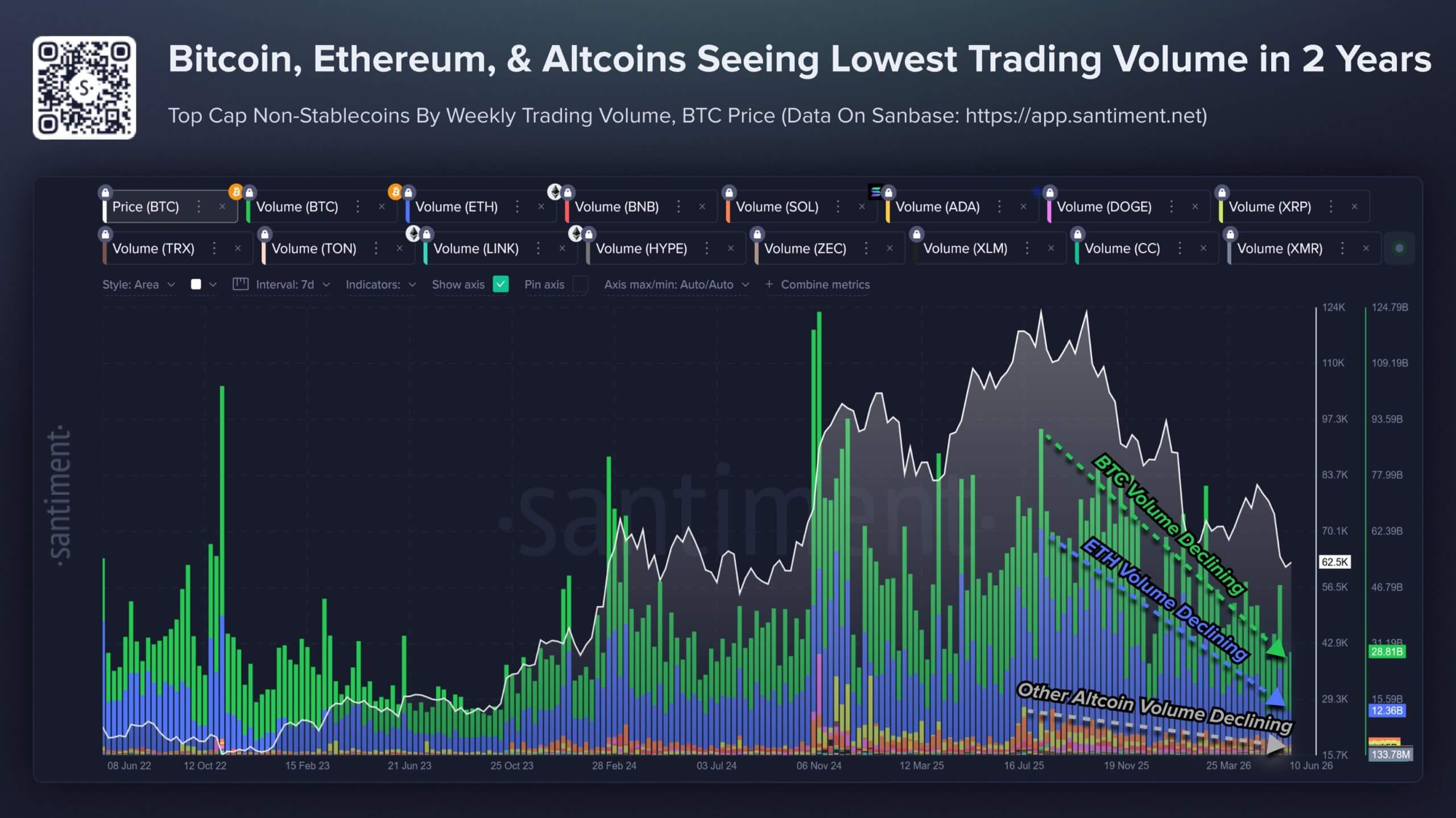

This entire market has arrived as widespread crypto trading activity has also cooled down.

Trading volumes across the largest non-stablecoin crypto assets have fallen to levels last seen in mid-2024, according to Santiment Data. The decline reflects a market in which many traders appear reluctant to pursue price gains or sell aggressively due to recent liquidations, macro uncertainty, and geopolitical risks.

For Bitcoin, this creates a two-sided setup.

On the other hand, low trading volumes can make the market vulnerable. If there are few participants and large buyers are slow, even modest selling can have a large impact on prices. Therefore, negative trends in ETF flows, slowing government bond accumulation, and weak proxy equity demand may weigh more heavily than in a more liquid environment.

Conversely, low volume may also indicate fatigue. Part of the strong rally in cryptocurrencies came after a period of weak trading activity, attention, and conviction. Markets often recover once positioning has already been reduced and the money that was on the sidelines begins to return.

That possibility prevents the current setup from becoming a simple bear market call. Bitcoin continues to have institutional investors, listed company buyers, and long-term investors. The broader digital asset industry as a whole continues to evolve, and the ETF market remains an established bridge between Bitcoin and traditional finance.

But the question at hand is narrower. Bitcoin does not require institutions to abandon Bitcoin to face pressure. The largest buyers simply need to slow down, sell selectively, or stop absorbing supply at the same pace.

That’s what the market is facing now.

Until ETF flows stabilize, Treasury demand recovers, or trading activity returns to Bitcoin-related stocks, the market may continue to be exposed to more difficult realities. So, while the institutional bid is still there, it’s no longer strong enough to trade on its own.

(Tag translation) Bitcoin