From a peak around $1,900 in 2011, gold built up a deep foundation over the years, retesting resistance near $2,100 in 2020, solidifying again into 2022, and then decisively rising to $3,300 by early 2025 and hitting a record above $5,400 in January 2026.

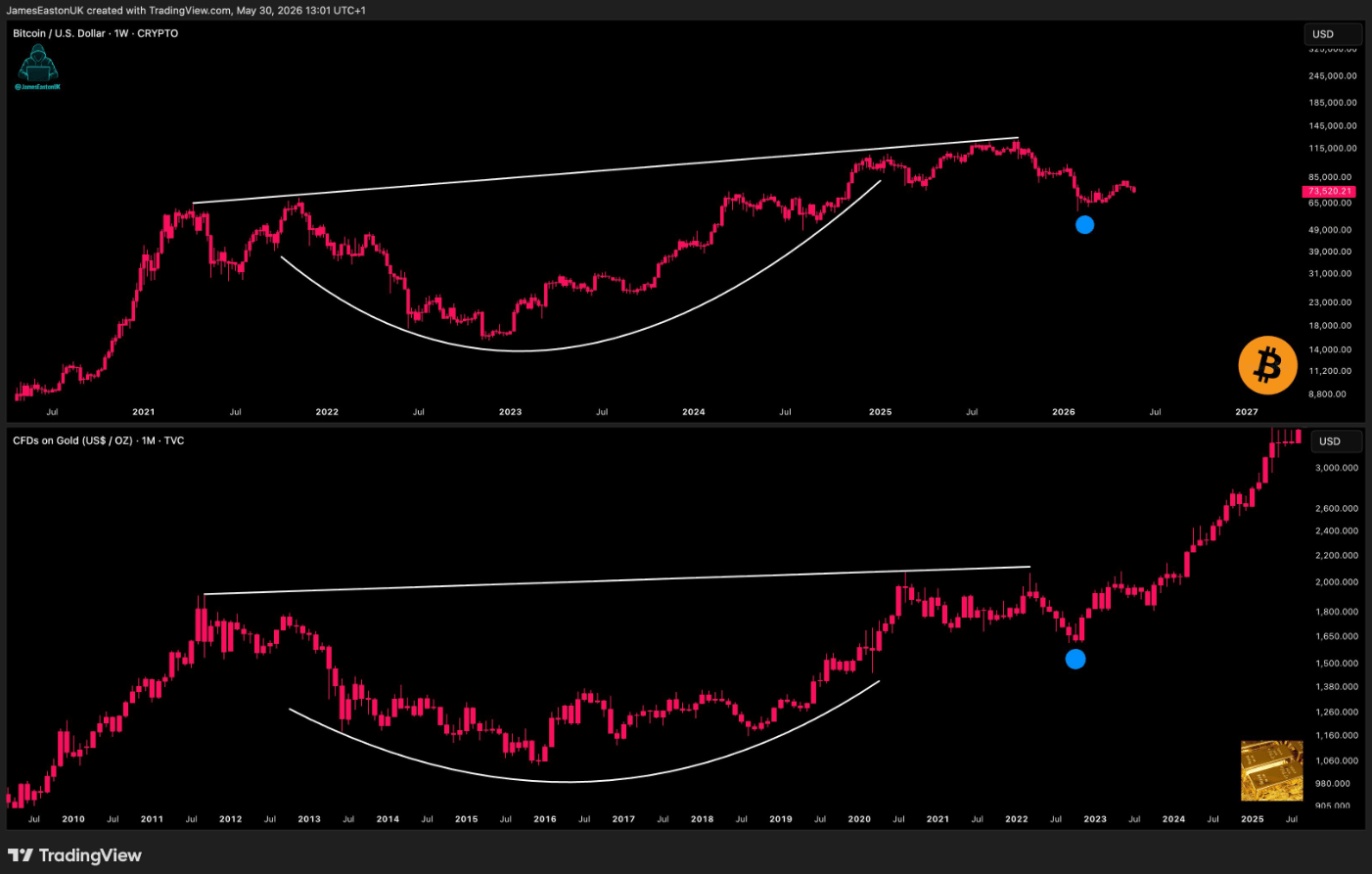

According to analyst and RealVision affiliate James Easton, Bitcoin’s weekly chart currently depicts the same formation on a compressed timeline: a peak in 2021, deep troughs in 2022 and 2023, a recovery and retest of previous highs in 2024 and early 2025, and a decline that left BTC in the blue.

Traders who overlay the two structures predict that if this pattern holds, Bitcoin will reach $300,000 by the end of 2026, arguing that Bitcoin is lagging behind the re-pricing of gold as a macro-hedging asset.

The macro argument for ending the delay seemed convincing until June 1, when Brent crude oil soared by more than $6 a barrel to $97.14, after Iran’s Tasnim news agency reported that Tehran had stopped exchanging messages with the United States and that its allies were considering closing the Strait of Hormuz.

The gold buyer group established the pattern.

Gold’s woes resolved as a weaker dollar, lower real yields, central banks accelerated diversification of foreign exchange reserves away from US Treasuries, and geopolitical fragmentation made non-sovereign hard assets structurally more attractive.

The central bank made 244 tonnes of net purchases in the first quarter alone, maintaining its 17th consecutive quarter of net purchases even as prices rose 81% year-on-year, according to World Gold Council data.

Demand for bars and coins increased 42% year-on-year to 474 tonnes, while gold-backed ETFs added 62 tonnes, bringing total demand to a record $193 billion, an increase of just 2% in volume.

Yield sensitivity is structurally unrelated to central bank reserve additions, so this breakout had a buyer base that did not change prices based on interest rate hike concerns.

Bitcoin’s pattern requires the same macro solution for a buyer base with opposite rate sensitivities. The U.S. Spot Bitcoin ETF recorded net outflows for 10 consecutive trading days through May 29, with nearly $3 billion outflowing during the period, according to data from Pharcyde Investors.

BlackRock’s IBIT shed approximately $2 billion during consecutive trading sessions, including a $527.8 million exit in a single session on May 27th.

ETF holders reprice their positions the moment oil prices push up inflation expectations and the odds of a rate hike rise. Yield-sensitive institutional investors are quick to exit when oil prices raise the possibility of a rate hike, and that’s exactly what is happening now.

| breakout ingredients | gold | Bitcoin | why is it important |

|---|---|---|---|

| structural demand | The central bank made a net purchase of 244 tonnes in the first quarter. | There is no equivalent to a central bank | Gold has sovereign reserve demand |

| ETF movements | Gold ETFs increased by 62 tons | Nearly $3 billion has been drained from BTC ETFs | BTC demand is more macro sensitive |

| retail demand | Demand for bullion and coins +42% YoY | Article frames are mainly led by ETFs/institutions | When the situation gets tough, the price of BTC will quickly revalue |

| rate sensitivity | Low for buyers of central bank reserves | Higher for ETFs/institutional investors | Oil-led Fed concerns deal further blow to Bitcoin |

| pattern status | Breakout completed | conditional breakout | BTC still needs macro confirmation |

oil problem

According to EIA data, 20.9 million barrels per day are transported through the Strait of Hormuz, equivalent to about 20% of global liquid oil consumption.

The Dallas Fed estimates that a two-quarter closure of the Strait of Hormuz would increase fourth-quarter headline PCE by 0.79 percentage points and core PCE by 0.31 percentage points.

Traders are pricing in a roughly 56% chance of at least one U.S. interest rate hike by the end of the year, according to June 1 CME Fedwatch data. As rates rise more likely, the dollar strengthens, real yields rise, and prices of liquidity-sensitive assets fall.

Gold fell nearly 2% on June 1 as that transmission raced through yields, confirming that even completed breakouts struggle when shocks arrive through interest rates. Bitcoin has been more directly affected by the war shock, with a record correlation of 0.96 to US stocks.

The chart pattern requires BTC to behave similarly to gold with an equivalent blue dot. That is, it absorbs selling pressure, maintains its base, and accelerates as macro conditions ease.

This pattern persists even if oil prices find a ceiling.

EIA’s short-term energy outlook for May predicts that Brent will average around $106 in May and June, but decline to $89 in the fourth quarter of 2026 and $79 in 2027 as production recovers in the Middle East.

The IEA predicts demand will fall by 420,000 barrels per day in 2026, adding fundamental weight to the supply cap.

If the Fed can maintain its path before actually raising rates, financial conditions will ease, the chances of a rate hike will fade, and the same forces that led to gold’s collapse – a weaker dollar, lower real yields, and institutional reallocation to hard assets – will be available to Bitcoin.

Bitcoin’s 30-day annualized perpetual basis has fallen to -0.45% as of mid-May, compared to 3.16% a year earlier, resulting in a spot-led structure with minimal leverage overlay. The same accumulation profile occurred prior to gold’s sustained breakout.

VanEck points to the $80,000 to $85,000 zone as the key resistance to regain to change momentum, with Citi’s bull run at $165,000 within 12 months. Achieving $300,000 would require a melt-up well beyond institutional consensus, and sustained inflows into ETFs to counter the increased demand and compress the available float.

formation fails

If the Hormuz disruption lasts for more than two quarters, the Dallas Fed’s inflation model predicts a 0.79 percentage point increase in headline PCE by the fourth quarter, enough to make a Fed rate hike more likely and to make ETF outflows self-reinforcing.

Citi’s recession scenario lies at $58,000, at which level the cup-and-handle formation on Bitcoin’s weekly chart transitions from the base to a failed breakout, completely resetting the pattern clock.

Peter Brandt, who set a price target for Bitcoin in April 2026 of $300,000 to $500,000, conditional on a four-year holding cycle, this caveat applies across the board if the Fed threatens to reset the price.

| scenario | oil/macro condition | supply path | Impact of Bitcoin | key level |

|---|---|---|---|---|

| the pattern survives | Oil has a ceiling. Brent follows EIA mitigation path | Chances of interest rate hikes diminish | ETF pressure eases, charts remain valid | Recovery between $80,000 and $85,000 |

| consensus bull | Weaker dollar, lower real yields, resumption of capital inflows | Improving liquidity | BTC moves towards institutional bull case | $165,000 |

| pattern fails | Holmes turmoil lasts for 2 quarters | Inflation pressures rise | ETF outflows become self-reinforcing | $58,000 |

| melt-up incident | Gold lag trading has completely ended | Easing/Liquidity Return | BTC overshoots consensus | $300,000 stretch target |

Gold benefits from war risk as central banks ramp up purchases, Asian retail demand accelerates and ETF holders change hands. Bitcoin will reach the same destination only through a secondary route, where geopolitical stress should translate into a weak dollar and monetary easing, a sequence that an oil-driven inflation shock would actively postpone.

Whether Bitcoin can complete its version of gold formation depends entirely on whether the oil rally stops before locking into a rate environment that makes this pattern impossible.

(Tag translation) Bitcoin